The central government imposes the tax in India, and it is the task of the concerned government to levied tax on individual taxpayers. The income tax system depends on the slab system, and the tax varies on various tax rates, which have set apart differently for financial year slabs. These tax rates keep further escalate and increase income slabs accordingly.

According to the well defined and regulated of various classified slabs in the income tax manual each year for every tax payer’s, where we argued on the latest income tax slab for the annual year 2019-20, the Annual year 2020-21, and the year 2021-22 are rooted in this Article. With that, it must be concluded and kept in mind that the above-said tax slabs tend to alter and change during every budget stated by the Finance Minister of India[1].

About the Existing Tax Regime of India

Within the prevailed Tax Regime of India, three classifications of individual tax payers are described and noted-

- Individuals comprise of residents as well as non-residents who are below the age of 60 years;

- Resident senior citizens who are below the age of 80 years but above than 60 years;

- Resident who are above 80 years of age, known as super senior citizens.

New Tax Regime

The Budget 2020 announced a new tax scheme provided to taxpayers as a boon or privilege based new tax slabs from the FY 2020-21 onwards.

The calculated tax will be the subject concern to health and education on a cess of 4%.

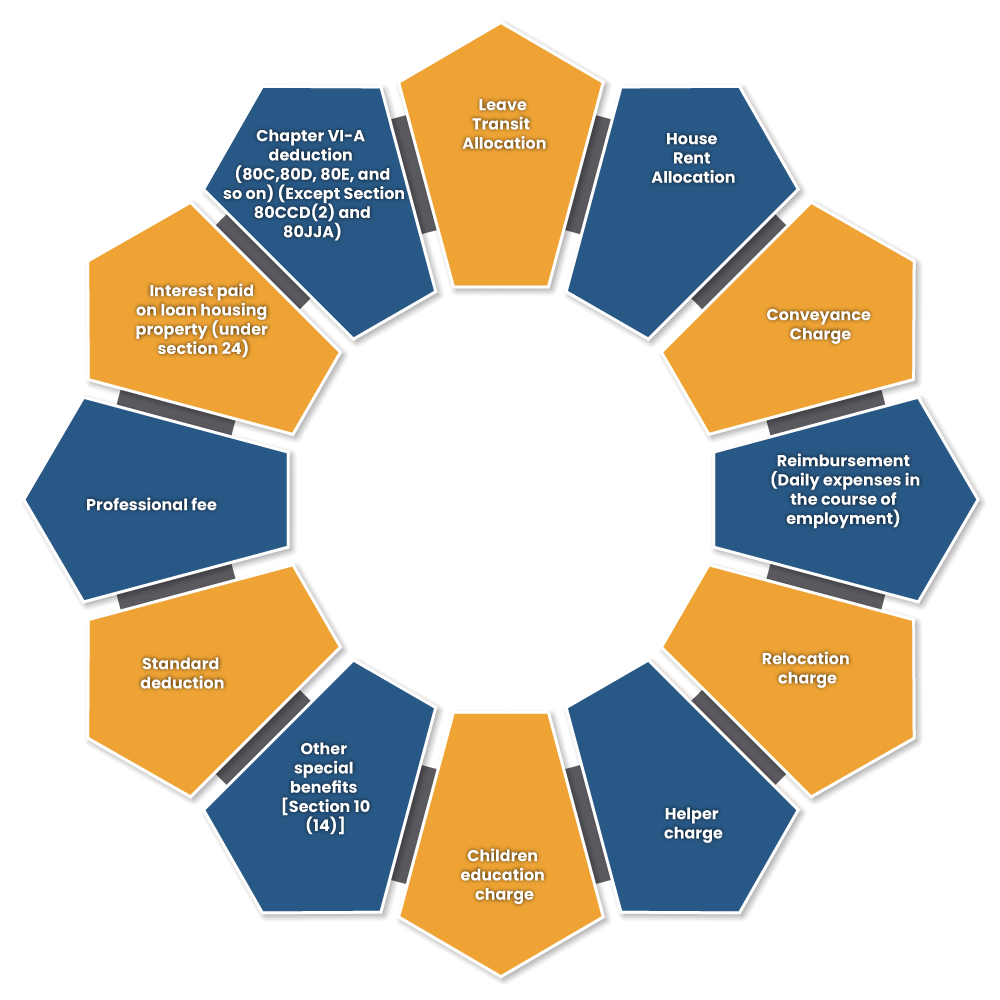

Under the zone of definite and concrete exemptions and deductions from FY 2020-21, a person can choose accordingly to be charged taxes based on their income.

The below mentioned are the exemptions and deductions that tax paid person has to be given while choosing the new tax slab.

Points to talk about at the Time of Choosing for the New Tax Slab

There are few option to be applied on or before the due date of filing return of income for AY 2021-22, those are as follows:-

In case the earning by a taxpayer was through any of the economic activities and applied for the option, he/she can retreat the option at once. An enterprise taxpayer withdrawing from the optional tax slab has to act below the regular income tax slabs.

According to India’s current tax laws, resident individuals’ income tax rate is based on their age ratio. Various tax slabs applicable to the person for the financial year 2018-19 and 2019-20. For instance, a resident below 60 years and an income of less than Rs. 2.5 lacs and is exempt from paying income tax.

Read our article:10 Reasons Why Filing Income Tax Return Is Vital For You

Income Regime and Tax Rates for F.Y. 2020-21/A.Y 2021-22

Income Tax Rate & regime for citizens & HUF

The Citizen who is (Resident or Resident but not Ordinarily Resident or non-resident), aged below 60 years on the last day of the significant previous year & for the Hindu Undivided Family

| Taxable income |

Tax

Rate (Existing Scheme) |

Tax

Rate (New Scheme) |

| Up to ₹. 2,50,000 | – | – |

| ₹ 2,50,001 to ₹. 5,00,000 | 5% | 5% |

| ₹. 5,00,001 to ₹. 7,50,000 | 20% | 10% |

| ₹.. 7,50,001 to ₹.. 10,00,000 | 20% | 15% |

| ₹10,00,001 to 12,50,000 | 30% | 20% |

| ₹ 12,50,001 to ₹ 15,00,000 | 30% | 25% |

| Above ₹ 15,00,000 | 30% | 30% |

An individual who is Resident of India or Resident but not Ordinarily Resident senior citizen, that is, every individual, being a resident or Resident but not Ordinarily Resident in India, who below the age of 60 years or more however less than 80 years during previous year:-

| Taxable income |

Tax

Rate (Present Scheme) |

Tax

Rate (Modified Scheme) |

| Up to Rs. 2,50,000 | – | – |

| ₹. 2,50,001 to ₹. 3,00,000 | – | 5% |

| ₹. 3,00,001 to ₹. 5,00,000 | 5% | 5% |

| ₹. 5,00,001 to ₹. 7,50,000 | 20% | 10% |

| ₹. 7,50,001 to ₹. 10,00,000 | 20% | 15% |

| ₹. 10,00,001 to ₹. 12,50,000 | 30% | 20% |

| ₹. 12,50,001 to ₹. 15,00,000 | 30% | 25% |

| Above ₹. 15,00,000 | 30% | 30% |

The Citizen who is inhabitant or inhabitant but not Ordinarily inhabitant super senior citizen, that is every individual, being a resident of India or Resident but not “Ordinarily Resident” within India, whose age is 80 yrs or more at any time during the previous year:-

| Taxable income |

Tax Rate (New Scheme) |

Tax Rate (Existing Scheme) |

| Up to ₹. 2,50,000 | – | – |

| ₹. 2, 50,001 to ₹. 5,00,000 | 5% | – |

| Rs. 5,00,001 to Rs. 7,50,000 | 10% | 20% |

| Rs. 7,50,001 to Rs. 10,00,000 | 15% | 20% |

| Rs. 10,00,001 to Rs. 12,50,000 | 20% | 30% |

| Rs. 12,50,001 to Rs. 15,00,000 | 25% | 30% |

| Above Rs. 15,00,000 | 30% | 30% |

Surcharge

a) 10 percent of Income-tax where the total income of individual more than Rs.50 lakh

b) 15% of Income-tax where the total income of individual more than Rs.1 crore

c) 25% of Income-tax where the total income of individual more than Rs.2 crore

d) 37% of Income-tax where the total income of individual more than Rs.5 crore

Education Cess

4 percent rate of income tax plus surcharge is applicable.

Point to Remember

A person who is the resident or Resident but not Ordinarily Resident is allowed to rebate under section 87A if his total earnings are not more than Rs. 500,000. The amount of taxable rebate shall be 100% of income-tax which calculate – Rs. 12,500, whichever is less. Rebate under section 87A is accessible in both proposals, i.e., existing proposal as well as a new proposal

Income Tax Rates for AOP /Any other Artificial Juridical Person/ BOI:-

| Tax Rate | Taxable income |

| Nil | Up to Rs. 2,50,000 |

| 5% | Rs. 2,50,001 to Rs. 5,00,000 |

| 20% | Rs. 5,00,001 to Rs. 10,00,000 |

| 30% | Above Rs. 10,00,000 |

Income Tax Rate for Partnership Firm

A partnership firm (including LLP) is allowed to pay tax at rate of 30%.

Surcharge

12% rate of Income tax where total income exceeds Rs. 1 crore

Education Cess

4% of Income-tax plus surcharge

Income Tax Slab Rate Prescribed for Local Authority

A local authority will be liable to be taxed at the rate of 30%.

Surcharge Slab

12% of Income-tax where total income exceeds Rs. 1 crore

Education Cess

4% of tax plus surcharge

Tax Slab Rate for Domestic Company

A domestic company is taxable at 30%. However, the tax rate is 25% of its turnover or gross receipt does not exceed Rs. 400 crore in the previous year.

| Related Particulars | Rate Slab – Taxable |

| If the gross receipt or turnover of the company does not exceed Rs. 400 Cr. in the last year 2018-19 | 25% |

| Company u/s115BA (Note 1) – Opted | 25% |

| Company u/s 115BAA (Note 2)- Opted | 22% |

| Company u/s 115BAB (Note 3)- Opted | 15% |

| Any other domestic company | 30% |

Note 1: Section 115BA

Any domestic company which is incorporated on or after March 1, 2016, and involved in the business activities of production or manufacture of any article or thing and research concerning to (or distribution of) such article or thing manufactured or produced by it and also It is not claiming any deduction under section 10AA, 32AC, 32AD, 33AB, 33ABA, 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB), 35AC, 35AD, 35CCC, 35CCD, section 80H to 80TT (Other than 80JJAA) or additional depreciation, can opt section 115BA on or before the due date of return by filing Form 10-IB online. The company cannot claim any brought forwarded losses (if such loss is related to the deductions specified above).

Note 2: Section 115BAA

Total earnings of an entity are taxable at the rate of 22% (from A.Y 2020-21), if the below listed conditions are satisfied:-

- Entity is not demanding for any deduction u/s 10AA or 32(1)(iia) or 32AD or 33AB or 33ABA or 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB) or 35AD or 35CCC or 35CCD or section 80H to 80TT (Other than 80JJAA).

- The company does not claim any forwarded losses (if such loss is related to the deductions specified in the above point).

- Conditions of MAT do not aply to such companies after exercising of option. The company cannot claim the MAT credit (if any available at the time of exercising section 115BAA).

Note 3: Section 115BAB

Total earnings of an entity are taxable at the rate of 15% (from A.Y 2020-21) if the below-listed conditions are satisfied:

- Entity (not covered in section 115BA and 115BAA) is incorporated on or after October 1, 2019 and initiated manufacturing on or before 31st March2023.

- Entity is not made by splitting up or reconstructing a business already in existence.

- Company does not avail any machine or plant which previously used for any cause.

- Company does not avail any building previously used as a hotel or a convention center, as the case may be.

- Company is not involved in any business activities other than the business activities related to manufacturing or production of any article or thing and research about (or distribution of) such article or thing manufactured or produced by it. The business of manufacture or production shall not contained the business activities of –

- Growth of computer software;

- Mining ;

- Conversion of marble blocks or similar items into slabs;

- Filling of gas into the cylinder;

- Printing of books or production of the cinematographic film; or

- Any other activity notified by Central Govt.

- Company is not demanding for any deduction u/s 10AA or 32(1)(iia) or 32AD or 33AB or 33ABA or 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB) or 35AD or 35CCC or 35CCD or section 80H to 80TT (Other than 80JJAA and 80M).

- Company does not claim any brought forwarded losses (if such loss is related to the deductions specified in the above point).

- Provisions of MAT not applicable to such companies after availing of option. The company cannot claim the MAT credit (if any available at the time of exercising section 115BAA).

Surcharge

a) 7% of Income-tax where total income exceeds Rs.1 crore

b) 12% of Income-tax where total income exceeds Rs.10 crore

c) 10% of income-tax where domestic company opted for section 115BAA and 115BAB

Education Cess

4% of Income-tax plus surcharge

Tax Rates for Foreign Company

A foreign company is taxable at rate of 40% its total income.

Surcharge

a) 2% of Income-tax where total earnings exceed Rs. 1 crore

b) 5% rate of Income tax where total earning exceed Rs. 10 crore

Education Cess

4% rate of Income-tax plus surcharge

Income Tax Slab for Co-operative Society

| Taxable income |

Tax Rate (New Scheme) |

Tax Rate (Existing Scheme) |

| Up to Rs. 10,000 | 10% | |

| Rs. 10,001 to Rs. 20,000 | 22% | 20% |

| Above Rs. 20,000 | 30% |

Surcharge

a) 12% of Income-tax where total income exceeds Rs. 1 crore

b) In the case of the Concessional scheme, the surcharge rate is 10%

Education Cess

4% rate of Income-tax plus surcharge. Total earnings of a company is taxable at the rate of 22% (from A.Y 2020-21), if the below said conditions are fulfilled:

- Company is not demanding any deduction u/s 10AA or 32(1)(iia) or 32AD or 33AB or 33ABA or 35(1)(ii)/(iia)/(iii)/35(2AA)/(2AB) or 35AD or 35CCC or 35CCD or section 80H to 80TT (Other than 80JJAA).

- The company is not claiming any brought forwarded losses (if such loss is related to the deductions specified in the above point).

- Provisions of MAT are not applicable to such entities after exercising of option. The company cannot claim the MAT credit (if any available at the time of exercising section 115BAA).

Conclusion

The estimated amount of income-tax depends upon imposing distinct tax rates to separate yearly income groups, which can be considered slabs for estimating income tax rates under provisions of different sections under the Income Tax Act, 1961, giving for separate income inclusion & exclusion for the same.

Read our article:An Overview on Filing of Form 10BA of Income Tax