There are different categories of taxpayers in India, and each requires various forms to file ITR (Income Tax Returns). Form ITR 3 is the most difficult ITR form for taxpayers, especially non-professionals. In this write-up, we will discuss Form ITR 3.

What is Form ITR 3?

Form ITR 3 applies to the individuals and HUF (Hindu Undivided Families) who earn profit from business/profession. If the individual or HUF has an income as a partner in a partnership firm, which is carrying out business, then the person will not be required to file ITR 3; in this scenario, he must file ITR 2 Form.

Eligibility for Filing Form ITR 3

An ITR 3 Form applies to individuals and HUF whose total income for a provided assessment year includes the following:

- Income from the business or profession is carried under a proprietorship firm, wherein the taxpayer is the proprietor.

- Rewards are earned from winning a lottery, horseracing, or income from other sources of activities.

- Generate income from short or long-term capital gains.

- Earn income from one or several house properties.

- Income assets from the way of assets in a country outside India.

Structure of a Form ITR 3

ITR 3 is briefly divided into the following sections:

- Part A

- Schedules

- Part B

- Verification

Let’s elaborate the each of these sections one by one:

- Part A includes-

| Part A- GEN | Nature of Business and General information |

| Part A- BS | Balance Sheet of the Proprietary Profession or Business as of 31st March 2021. |

| Part A- Manufacturing Account | Manufacturing Account for the financial year 2021-2021. |

| Part A- Trading Account | Trading Account for the financial year 2020-2021. |

| Part A- Profit & Loss | Profit and Loss for the Financial Year 2020-2021. |

| Part A- Other Details | It is optional in a case not liable for audit under Section 44AB. |

| Part A- QD | Quantitative information (it is optional in a case not liable for audit under Section 44AB). |

- Schedules include-

| Schedule- S | Computation of income under head Salaries. |

| Schedule- HP | Computation of income in the head Income from the Property of House. |

| Schedule- BP | Computation of income from profession or business. |

| Schedule- DOA | Computation of depreciation in another asset under the Income-tax Act. |

| Schedule- DPM | Computation of depreciation in plant and machinery under the Income-tax Act. |

| Schedule- DEP | Summary of depreciation on all the assets in the Income-tax Act. |

| Schedule- DCG | Computation of deemed capital gain on the sale of depreciable. |

| Schedule- CG | Computation of income under the head of Capital gains. |

| Schedule- ESR | expenditure on scientific research Deduction under section 35. |

| Schedule- 112A | Information on Capital gains where section 112A is applicable. |

| Schedule- OS | Computation of income in the head Income from other sources. |

| Schedule 115AD(1)(B)(iii)Proviso | For Non-Resident’s information on Capital gains where section 112A is applicable. |

| Schedule- CYLA-BFLA | Statement of income after set off current year’s losses and statement of income after set off unabsorbed loss brought forward from earlier years. |

| Schedule- CYLA | Statement of income after set-off of current year’s losses. |

| Schedule- BFLA | Statement of income after set-off of unabsorbed loss brought forward from earlier years. |

| Schedule- UD | Statement of unabsorbed depreciation. |

| Schedule- CFL | Statement of loss to be carried forward to future years. |

| Schedule- ICDS | Effect of income computation disclosure standard on profit. |

| Schedule- 80G | Statement of donations entitled for Deduction in section 80G. |

| Schedule- 10AA | Computation of Deduction under Section 10AA. |

| Schedule- RA | Includes information on donations to institutions entitled to deduction under Section 35(2AA), 35(1) (iia), or 35(1)(iii). |

| Schedule- 80IA | Computation of deduction under section 80IA. |

| Schedule- 80IB | Computation of deduction under section 80IB. |

| Schedule VI-A | Statement of deductions (from total income) in Chapter VIA. |

| Schedule- 80C/ 80-IE | Computation of Deduction under section 80IC/ 80-IE. |

| Schedule AMT | Computation of Alternate Minimum Tax Payable in Section 115JC. |

| Schedule AMTC | Analysis of tax credit under section 115JD |

| Schedule SI | Statement of income that is chargeable to tax at special rates. |

| Schedule SIP | Statement of income arising to spouse/ son’s wife/ minor child or any other person or association of person to be included in the assessee’s income in Schedules-HP, BP, CG, and OS. |

| Schedule IF | Details regarding partnership firms in which the assessee is a partner. |

| Schedule- PTI | Pass-through income information from business trust or investment fund as per sections 115UA and 115UB. |

| Schedule- EI | Statement of income not included with total income (exempt income). |

| Schedule- TPSA | Secondary adjustment to transfer price according to section 92CE(2A) |

| Schedule- TR | Statement of tax relief claimed in section 90 or section 90A or section 91. |

| Schedule- 5A | The Portuguese Civil Code governs details regarding the apportionment of income between spouses. |

| Schedule- FA | Statement of Foreign Assets & income from any source outside India. |

| Schedule- FSI | Information on income from outside India and tax relief. |

| Schedule- AL | Asset & Liability at the end of the year (applicable where the total income exceeds Rs.50 Lakhs) |

| Schedule- GST | Details regarding turnover/ gross receipt reported for GST. |

| Schedule- DI | Schedule of tax-saving investments, deposits, or payments to claim Deduction or exemption in the extended period from 1st April 2021 until 30th June 2021. |

- Part B

- Part B- TI: It includes the computation of a taxpayer’s total income.

- Part B- TTI: This Section computes the tax liabilities on one’s total income.

- Verification: Lastly, the Form ITR 3 structure guarantees to authenticate the details furnished above.

How to file Form ITR 3?

Form ITR 3 can be filed either online or offline:

- Online: The income tax return can be done electronically using the Digital Signature Certificate. This data can be transmitted after the submitting verification of the return.

- The Form ITR 3 online filing process starts with visiting the official e-filing web portal of the Income Tax Authority.

- You need to register an account with the portal if you are new.

- This portal auto-generates your PAN information. Then choose ‘Assessment Year’ for which you are filing the ITR 3 Form.

- Then go to the Revised Return section, if you wish to file a revised return against a previously filed original return’.

- Submit the online form and click on ‘Continue’.

- At this point, you are required to provide income details, exemptions, deductions, and investments.

- Then, add the details of tax payments through TDS, TCS, and/or advance tax.

- Remember to fill all data accurately and carefully. Additionally, periodically click on ‘save the Draft’ to avoid losing data.

- Select the preferred verification option from the following:

- Instant e-verification

- E-verification later but within 120 days from filing Form ITR 3.

- Verification through a duly signed ITR V sent to Centralised Processing Centre (CPC)[1] via post and within 120 days of filing return.

- Select Preview and Submit the Form.

Electronic returns can be filed when:

- The assessee is an Indian resident, or in case the signing department is located out of India.

- Assess those claiming relief under sections 90, 90A, and 91 for whom the schedule FSI & Schedule TR must file the returns electronically.

- The assesses with more than Rs.5 Lakh total income must be outside India.

New Update in Form ITR 3

- THE ITR 3 e-filing offline utility for taxpayers is now available on the income tax portal.

- ITR 3 JSON Schema for the annual year 2022-23.

- The Form ITR 2 validation rules V1 for the annual year 2022-23 are available on the income tax e-filing portal.

- The income-tax authority has issued notification No. 134/2021/F.No. 1 78/4/2021-ITA related to the LIC of India for the annual year 2021-22.

- The due date for completion of the penalty proceeding under the Act has been extended from 30th September 2021 to 31st March 2022.

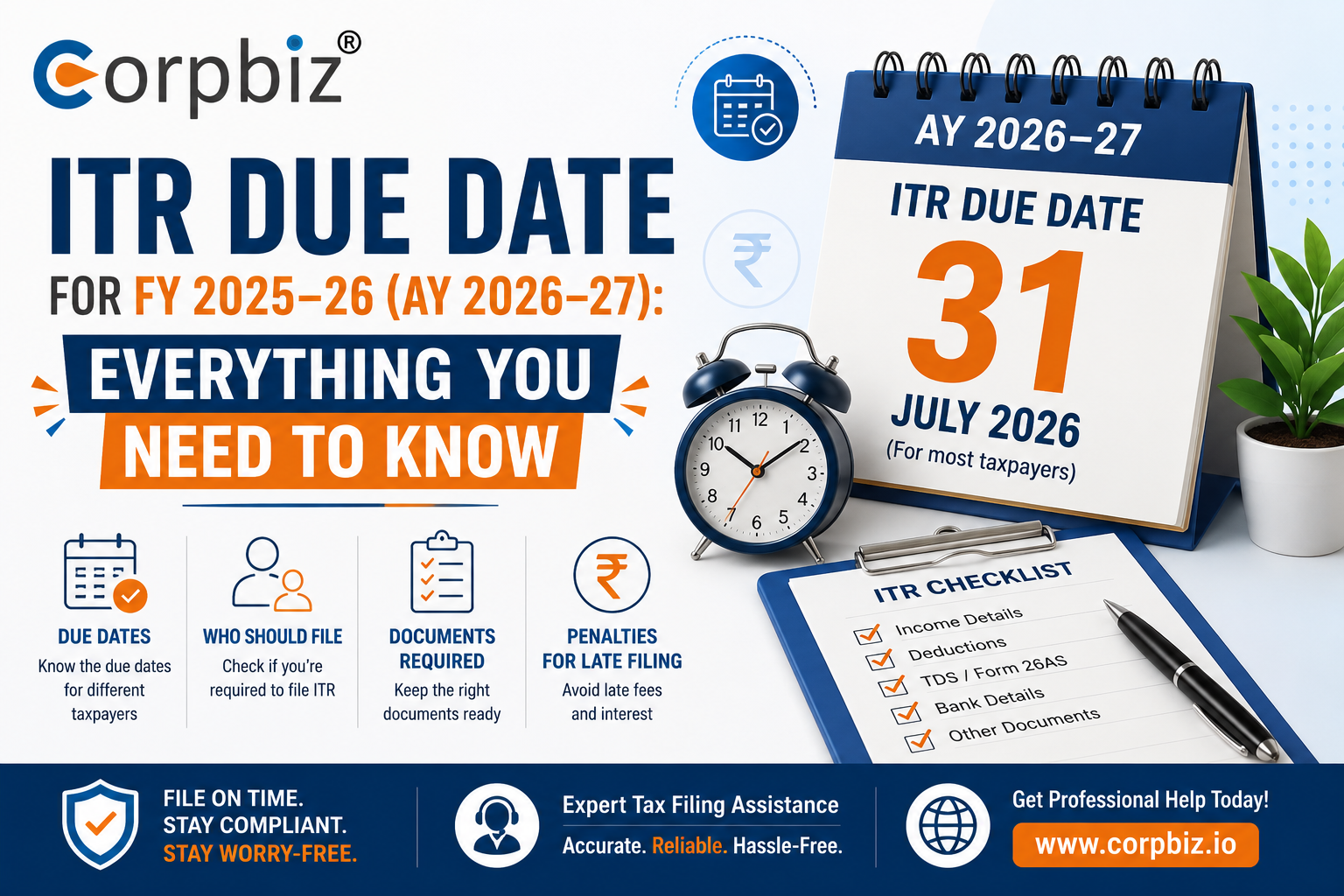

What is the Due-Date for Filing the Form ITR 3?

The date due for filling an ITR is as for individuals & businesses:

- The Annual Year 2022-2023: 31st July 2021 for Non-audit Cases and 31st October 2022 for audit Cases.

- The Financial Year 2020- 21 (the Annual Year 2021 -22): 31st December 2021 (Revised) for Non-audit Cases and 15th March 2022 (Revised) for Audit Cases.

Conclusion

Individuals and Hindu Undivided Families who earn money from their profession or a business can use the ITR 3 Form. ITR-3 cannot be filed if an individual or a Hindu Undivided Family receives income from a business partnership.

Read our Article:Types of ITR (Income Tax Returns)