Forensic Audit

If you need forensic audit to prosecute a party for embezzlement, fraud, or additional financial crimes, you can take instant action with the help of CorpBiz Professionals.

Get Free Expert Consultation

1 Lakh+ Global Brands That Trust Us!

Talk to an Expert

Online

Expertise in Audit

(4.8)

Enquiry Form

Among Asia Top 100

Consulting Firm

Get Consultation

Lowest Fees

100,000 + Clients.

Overview of Forensic Audit

A forensic audit is an evaluation and examination of an individual's or a firm's financial records to stem up evidence that can be used in a legal proceeding or court of law. Forensic auditing is a specialization within the accounting field, and most large accounting firms have a forensic auditing department. Forensic audits necessitate auditing and accounting procedures as well as expert knowledge about the legal outline of such an audit.

Generally, Forensic audits cover a wide range of investigative activities. A forensic audit may be directed to prosecute a party for embezzlement, fraud, or additional financial crimes. Moreover, the auditor may also be called to help as an expert witness during trial proceedings of a forensic audit. Forensic audits could also involve situations such as disputes related to business closures, bankruptcy filings, and divorces that do not involve financial fraud.

What are the “Whys” for Conducting a Forensic Audit?

Forensic audit investigations may interpret, or confirm, numerous kinds of illegal activities. In general, a forensic audit is used if there is a possibility that the evidence collected would be used in court in its place of a normal audit.

The forensic audit process is similar to a traditional financial audit — accepting investigation, planning, assembling evidence, and writing a report — with the added steps of a potential appearance in court. The lawyers offer evidence that the crime is one or the other discovered or disproved, which agrees the harm sustained. In this procedure, they will explain their conclusions to the respondent should the case go to trial in front of the judge. The reasons are as follows:-

1. Corruption

Corruption is a significant obstacle to socio-economic development and also at different corporate levels. It can have come along with ill-effects on the image of the business/company and jeopardize it severely. It consists of any illegitimate use of the office or dishonest behaviour and its resources. In such occurrences, a forensic auditor attempts to look for accounts of extortion and bribery, or anything that will amount to or relate to any conflict of interest.

2. Extortion

Taking a step ahead from any corruption, extortion involves the use of force, threat, or violence to extract money from another person/party. For the interest of the company, this may be done on the pretence of ‘protection money’ for sophisticated cyber extortion schemes, small businesses, etc. Moreover, the identification of extortion in company finances reduces its reliability in the eyes of its suppliers, clients, etc. which is the most important reason for having a compacted financial statement.

3. Bribery

Bribery refers to the conduct of dishonestly influencing one’s position or role to receive something as well as promising something favourable to the party demonstrating such benefit. There are few problems where bribery arises, not always in such a role/position to offer anything. When one acts beyond his authority, it obstructs the company's profits and interest, which is illegal to do so.

4. Conflict of interest

Anything on a related note, including bribery, that is done to gain personal profit, and which is unfavourable to the company. By this conducts forms the objective of a forensic audit.

5. Fraud

There are a few reasons related to the fraud associated with the financial circle of any company. Those are as follows:-

6. Asset Misappropriation

This included raising fake invoices, misappropriation of cash, payments made to non-existing employees or suppliers, theft of Inventory, or misuse of assets. It comes about in undesirable conditions when people who are entrusted to manage the assets of a company/organization give away from it. Moreover, it can be the greatest detrimental to the company when it may lead to infiltration by other organizations to take control over the control of the victim company. It directly hit on the cash flow of the organization.

7. Financial Statement Fraud (FSF)

Financial statement fraud is the will full and deliberate misstatement or misrepresentation, creating a false impression and omission of financial statement data to mislead the reader of a Company’s financial strength. Generally, it defers revenues or expenses in a different time period to show consistent earnings or growth. Towards the other extreme, it consists of overstating revenues. It diminishes the confidence of market participants and capital markets in the dependability of financial information.

What are the benefits of a Forensic Audit?

Few chief benefits of Forensic Audit are listed below. Those are as follows:-

Book a Free Consultation

Get response within 1 hour

What is the procedure for conducting a Forensic Audit?

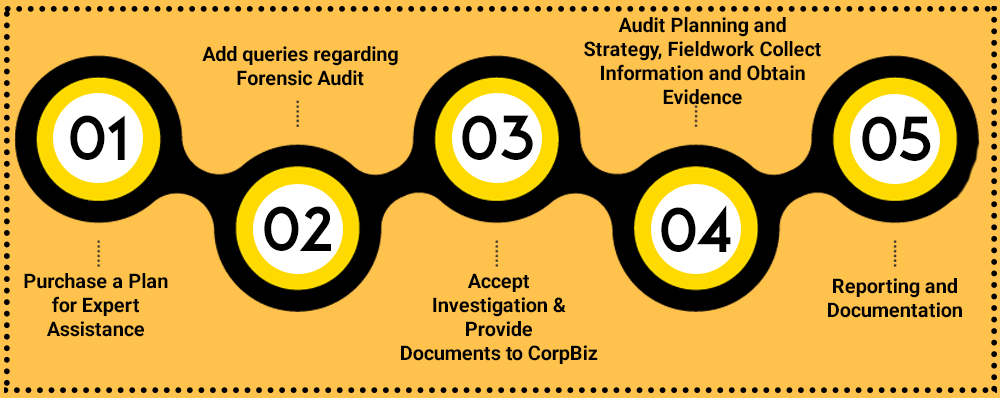

Step 1 – Accepting the Investigation and Know your Client

To conduct a truthful, unbiased audit, and investigation, a forensic audit is always assigned to an independent firm/group of investigators. As a result, their first step is to determine whether they have the necessary skills tools and expertise (auditor) to go forward with such an investigation whenever such a firm accepts an invitation to conduct a forensic audit. Only when they are contended with such considerations are they required to assess their own 'training and knowledge' of fraud detection/investigation and legal framework. They also can go ahead and accept the investigation that has been offered.

Step 2 – Planning the Audit Investigation and Strategy

Planning the investigation is the first most steps in a forensic audit before executing. The Auditor (s) must judiciously ascertain the Audit goal so being conducted and prudently determine the procedure to achieve it, over and done with the usage of effective techniques and tools. They should be clear on the ultimate categories of the report before planning the investigation. Those are as follows:-

1. Identification of the kind of fraud that has been operating,

2. Fieldwork Collect Information and Obtain Evidence

3. dentifying the fraud of how long it has been operating for, and how the fraud has been afforded to conceal the same

4. Identifying the fraudster(s) / Masterminds involved

5. Measuring the financial loss suffered by the client and the Company

6. Collecting Evidence to be admissible and used in court proceedings

7. Measurement of Frauds, Analysis Evaluate and Assess the Impact of Evidence

8. Providing advice to prevent and measure the recurrence of the fraud.

Step 3 – Gathering Evidence for Investigation

There are specific procedures that are carried out in forensic auditing to harvest Evidence. All kinds of Audit techniques and procedures are used to gather Evidence to prove and to identify. Such as how it was conducted and concealed by the perpetrators and how long they have fraudulent activities existed and continued in the organization. In the direction of gathering Evidence, the investigators can use the following techniques. Those are as follows:-

1. Testing controls which identify the weaknesses to gather Evidence, which certifies the fraud to be perpetrated

2. By means of analytical procedures to provide comparatives between different segments of the business or compare trends over time

3. To locate the "timing and location" of relevant details being tampered or altered in the computer system, investigators can apply computer-assisted audit techniques

4. Interviews and Discussions with employees

5. Substantive techniques such as cash counts, reconciliations, and reviews of financial and Non-financial paper works.

Step 4 – Reporting and Documentation

The reporting stage is the furthermost clear and apparent element in a forensic audit. The investigating team is expected to report the findings of the investigation after investigating and gathering Evidence. They must provide a summary of the Evidence and conclusion that came out of the loss suffered due to the fraud happened. It should also include the executed plan of the fraud itself and how it stretched out and had profit out of the whole trail of events. They should provide suggestions to prevent such fraud in the future events.

Step 5 – Court Proceedings - Fraud Prevention measures and Exercise Judgement

The last stage enlarges over those audits that principally lead to legal/ court proceedings. The auditors will give litigation assistance as mentioned above, where they will be called to Court and included in the advocacy process/ trials. The understanding here is that they are requested in because of their expertise and skill in commercial issues and legal proceedings. Most importantly, they must lay down the facts and findings reasonably and objectively to understand so that the anticipated action can be taken up judiciously.

CorpBiz Procedure for Forensic Audit

We believe that most of the times, corruption and fraud in a company can be controlled and eradicated, having to go for a forensic audit, and taking radical legal steps subsequently. It is pertinent that there exist expressed accountability and reliability mechanisms to help foster such work environment, along with a situation/atmosphere of control. Such techniques reduce the probability of corruption in a company and its ill-effects. Prevention can be measured even at the time of recruitment by way of thorough contextual background checks and screening processes.

Forensic Audit is a compulsory step in the terms of fundamentals in the existence of evaluation and examination of an individual's or a firm's financial records to stem up evidence that can be used in a legal proceeding or court of law. It shall be prepared with careful consideration, and plenty of time should be allowed for all stages of the drafting and investigation and reporting. It is advisable that an attorney with “Forensic Auditing experience” must be appointed to overwhelm many of the potential pitfalls that creep around within Forensic Audit.

CorpBiz recommends you that you should be in contact with an Experienced Auditor to understand the requirement in detail. The elementary information would be mandatory from your end to start the process. The Auditor will begin working on your request once all the information is provided, and the payment is received.

Why CorpBiz?

CorpBiz is one of the platforms which coordinate to fulfil all your legal and financial requirements and connect you to consistent professionals. Yes, our clients are pleased with our legal service! Because of our focus on simplifying legal requirements, they have consistently regarded us highly and providing regular updates.

Our clients can also track at all times the progress on our platform. If you have any questions about the Forensic Audit process, our experienced Auditors are just a phone call away. CorpBiz will ensure that your communication with professionals is charming and seamless.

What are the legal provisions attract if he/she is caught in a forensic audit?

It is required to know about the various statutes that talk about forensic audits' implementation to understand the legal provisions, and consequences that a person attracts on being caught in a forensic audit in India.

1. Sections - 235 & 237 of the Companies Act, 2013

It Empowers the Central Government to order an investigation into the affairs of a company, inspect the books of accounts of a company, special audit, and launch prosecution for destruction and violation of the provisions of the said Act.

2. Provisions of Sick Industrial Companies, Act Companies Act, 2013

3. Prevention of Money-Laundering Act, 2002

Section 3 of the said Act- defines the offense of "money laundering" as the involvement of a person in any activity or process connected with the proceeds of crime and sticking out it as untainted property, where the limits and scope of integrating forensic audits can be undoubtedly seen.

4. SEBI Act, 1992- (Regulation 11 C)

It empowers the SEBI to investigate the affairs of intermediaries, to direct any person or brokers associated with the securities market whose financial transactions in securities are being allocated in a manner detrimental to the securities market or the investors. Moreover, under the Insurance Act, 1938- Section 33 of the Act empowers the IRDA; it also emphasizes directing any person (Investigating Authority) and investigating the affairs of any insurer.

5. The Companies (Auditor's Report) Order, 2003

The Act needs auditor to report the effect of whether it has affected the going concern status if a substantial part of fixed assets has been disposed of off during the year.

If he or she is caught in a forensic audit, the following penalties may be faced by a person in light of these statutory authorities by way of administrative penalties.

Frequently Asked Questions

Forensic auditing is a specialization within the accounting field, and most large accounting firms have a forensic auditing department

Yes. The auditor may be called to help as an expert witness during trial proceedings of a forensic audit.

Corruption is a significant obstacle to socio-economic development and also at different corporate levels. It includes Extortion, Bribery, and Conflict of interest.

There are a few reasons related to the fraud associated with the financial circle of any company. It includes False and Wilful representation or Assertion, Perpetrator of Representation, Intention to deceive, the representation must relate to a fact, the the active concealment of circumstances, and many more.

Asset Misappropriation includes raising fake invoices, misappropriation of cash, payments made to non-existing employees or suppliers, theft of Inventory, or misuse of assets.

Financial statement fraud is the will full and deliberate misstatement or misrepresentation, creating a false impression and omission of financial statement data to mislead the reader of a Company's financial strength. Generally, it defers revenues or expenses in a different time period to show consistent earnings or growth. It includes -Forensic Data Analysis (FDA) and Fraud Triangle and Fraud Risk.

There are numerous benefits associated with Forensic Audit. To know in detail, please refer to the above text for better understanding.

- Forensic Audit Planning and Strategy

- Obtain Evidence & Analysis Evaluate

- Assess the Impact of Evidence

- Exercise Professional Judgement

- Reporting and Documentation

- Handling any Litigation Involved. To know in detail, please refer the above text for better understanding

They must lay down the facts and findings reasonably and objectively to understand so that the anticipated action can be taken up judiciously.

Prevention of Money-Laundering Act, 2002:- Section 3 of the said Act- defines the offense of "money laundering" as the involvement of a person in any activity or process connected with the proceeds of crime and sticking out it as untainted property, where the limits and scope of integrating forensic audits can be undoubtedly seen.

It includes:- Unlawful copying of citations and quotations from any data, Illegal access and downloading files, Introduction of malicious or viruses programs, Impairment to a computer network or computer system, Rejection of access to a lawful person to a computer system, Supporting to any person to facilitate unlawful access to a computer system.

About the Author

Neha Dawra

Legal Researcher

Written by Neha Dawra. Last updated on Jul 2 2026, 03:50 AM

Neha Dawra has 4+ years of experience in legal research and intellectual property advisory. Her expertise lies in analyzing IP laws, drafting structured legal content, and simplifying complex registration procedures into clear, simple insights.

Updated testimonials from our customers

Trusted by thousands of businesses across India for seamless compliance, registrations, and advisory services.

Really thankful to Corpbiz. Our experience with its expert was tremendous. Strong professional approach towards clients. My Company Registration was filed in a very less time, thanks to Corpbiz experts.

We would recommend Corpbiz incorporation services to any founder without a second doubt. The process was beyond efficient and shows Corpbiz founder's commitment and vision to truly help entrepreneurs and early stage startups to get them incorporated with ease.

I was searching for a company for assistance in the incorporation services. Then one of my friend tell me about Corpbiz and definitely the Corpbiz team is really efficient and has an experienced staff to guide us through the entire process of Company Incorporation.

Setting up our Bio Medical Waste Recycling Plant was a huge project. Mukul managed the entire compliance framework seamlessly from start to finish.

Corpbiz is very reliable and efficient. They managed all paperwork, resolved my queries, and completed my GST registration much quicker than I expected.