The Income Tax Appellate Tribunal, New Delhi held that the generated revenue distribution of products cannot be taxed as ‘royalty’ by business income as it is already mentioned under (MAP) Mutual Agreement Procedure. The earning of an assessee generated from revenue distribution cannot tax as royalty as it will amount to double taxation which assessee already states under the Mutual Agreement Procedure.

Key Highlights from the order as Revenue Distribution Cannot Taxed as Royalty

- The appellant never granted any licenses to use any copyright but only granted commercial rights in the nature of ‘broadcast reproduction right’, which is defined under section 37 of the Copyright Act[1].

- The respondent is carrying out a distribution and selling of the advertisement and it does not have any kind of right for edit, interpret, and add the products distributed by this.

Read our article:8 Incredible Benefits of Copyright Registration in India

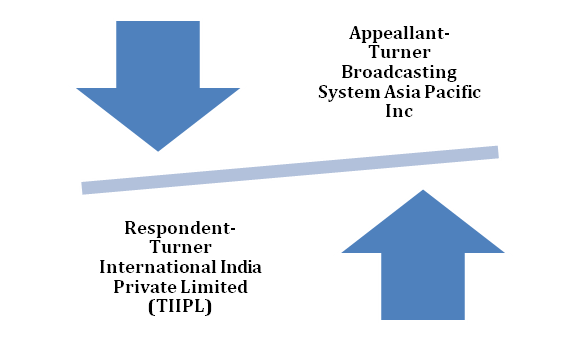

In matter of Turner Broadcasting System Asia Pacific Inc vs. Turner International India Private Limited

Facts of the Case

An Appellant- Turner Broadcasting System Asia Pacific Inc. was a company incorporated under the USA laws. During the captioned assessment years, an appellant was a tax resident of the USA. During the relevant assessment years, an Appellant derived advertisement and distribution revenue from a grant of exclusive rights to (TIIPL) Turner International India Private Limited, an Indian Company, to sell advertising on the products and also to distribute the products.

However, the Indian Company, TIIPL acted as the exclusive distributor of the products to cable operators and other permitted systems on a ‘principal to principal basis’. A ‘distribution agreement’ allowed TIIPL to distribute the products to various cable operators and ultimately to the consumers in India.

Legal Illustration: Brief

The distribution revenue collected by TIIPL was shared between TBSAP (Third party) and TIIPL. However, in relation to TIIPL (Indian Company), the copyright in content always remained with an Appellant. At any point of time, it was NOT transferred either to TIIPL or the sub-distributor, which is evident from Clause 5 of the Agreement concluded between an Appellant Company and TIIPL. This clarifies that all copyrights and other proprietary rights in the products (channels) has to vest solely in the appellant company.

The AO in the current year must be treated as the distribution revenue to be ‘Royalty’ in accordance with section 9(1)(vi) of Act, and Article 12 of DTAA (Double Taxation avoidance Agreement) between India and the USA. After perusal of distribution in sales agreement it came to conclusion that as per terms of an agreement, in consideration rights for license is between TIIPL and TENA (Sub-distributor). The TIIPL have to pay TENA the sum of 50% of net revenue generated from a distribution and advertising sales on channels subject to minimum guarantee set out under the “distribution fee” and “advertising sales fee” which is a royalty both under the Income Tax Act and DTAA.

What was decided by the ITAT?

The bench of two-member has observed that an appellant has never granted any licenses to use any copyright, either to a distributor or to the cable operator. It has only granted right for purpose of selling advertisement on the product that are channels and distribution of such products in India. The tribunal has also observed that an Indian company is carrying out a distribution and selling of the advertisement and it does not have any kind of right for edit, interpret, and add the products distributed by this.

The tribunal held that an assessee company only granted commercial rights in the nature of ‘broadcast reproduction right’ to the TIIPL, which is defined under section 37 of the Copyright Act. Therefore, it is held that revenue derived by an assessee for distribution of products is NOT taxable as ‘royalty’ as it is a business income of the assessee.

Conclusion

The revenue distribution earned by the appellant-assessee cannot be taxed as royalty as a business income. Since an assessee has already mention its income as business income in terms of the MAP. Therefore, an income declared by the assessee in accordance with the MAP and accepted by the Department in the earlier years has to be accepted.

Read our article:Extension on Tax Audit Report due Dates and Income Tax Returns Applicable for AY 2020-21