Every taxable person is responsible to pay tax on ad-valorem basis meaning “according to the value” the person is taxed based on the value of transaction or a property. Every individual liable to pay tax has to pay GST on both for supply of goods or services and the value for the same has to be decided in accordance with section 15 of the CGST Act, 2017.

Therefore, Valuation Rule for Supply under Goods and Services Tax is under GST Law to determine the Transaction Value on which the taxable person shall pay the tax. Thus, at present the GST will be charged on the valuation of supply. The price actually paid for the supply of goods and services involving un-related parties i.e., price is the only consideration in the Transaction value.

What is the Valuation Rule for Supply under GST?

The section 15 of the Central Goods and Services Tax Act and CGST Rules, 2017 on Determination of Value of Supply provides which is related to the valuation for supply of goods or services made in different circumstances and to different persons.

In cases where the consideration is not completely in money then the value of supply of goods or services shall, be the open market value of such supply:-

- The total sum of consideration in money if the open market value is not available – if such amount is known at the time of supply then any such additional amount in money as is equal to the consideration which is not in money,

- The value of supply of goods or services or for both of similar quality and kind – in case where the value of supply is not determinable under clause (a) or clause (b),

- The consideration of total sum of in money – where the value is not determinable under any of the clauses (a), (b) or (c).

For example:- Where a new laptop is supplied for Rs. 20000 but together with the exchange of an old laptop and if the price of the new laptop without exchange is Rs. 24000 then the value of the new laptop in the open market is Rs. 24000.

Read our article:GST Returns Reflecting in your Income Tax Passbook (Form 26AS)

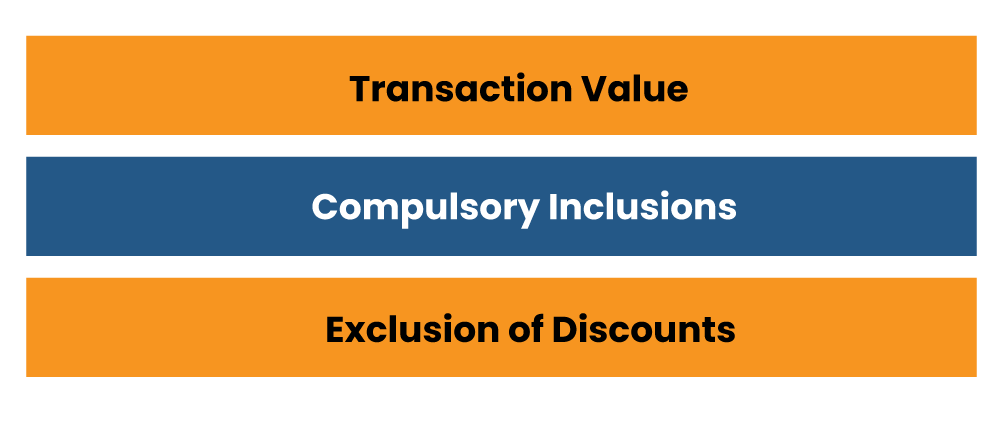

Things to be Considered while Applying Valuation Rules

There are three things that shall be taken into consideration while valuation of tax under GST:-

i) Transaction Value

According to GST, the taxable value is regarded as the transaction value. In simple words, transaction value under GST shall be the value paid by the buyer to the supplier.

But it is equally imperative to note here that the price is the sole consideration and the supplier and buyer shall not be related persons. Though, for some special cases the transaction value has to be determined in accordance with the CGST Rules, 2017.

ii) Compulsory Inclusions

This will provide some key things that shall form a part at the time of valuation compulsorily:-

- Any taxes, charged or fees imposed under any different law besides the GST law.

- Any expenses that the buyer incurs on behalf of the supplier.

- Interest, penalty or late-fees.

- Any subsidies given by the government or any direct subsidies.

- Any other supplementary expenses which includes handling and packaging costs and commission sustained by the supplier.

iii) Exclusion of Discounts

The taxpayer shall while determining the taxable value exclude all the discounts from the value of supply whether it is a pre-supply discount or a trade supply. Nonetheless, the post supply discount during the valuation time can also be excluded if the mentioned below two conditions are satisfactorily met:-

- If the discount is agreed in accordance with the pre-supply agreement condition as made between the buyer and the supplier.

- The buyer shall reverse the Input Tax Credit (ITC) which shall apply to such a discount.

Analysis of Valuation Rule for Supply

The GST law has provided various valuation rules which can be considered while determining the value of supply of goods and services. Given below is the list of all probable circumstances wherein there is requirement to implement valuation rule and has been categorized under seven heads. These are:-

Valuation Rule 1

It provides for the value of supply of Goods or Services where the consideration is not wholly in money. Like for example: where a buyer gives another good which is in exchange of barter and partial consideration.

Valuation Rule 2

It provides for the value of supply of Goods or Services or both but such valuation is between related or distinct persons, but not through an agent. Example shall include the cases where related persons or entities are supplied with goods or services and they have separate registration but the control is common.

Valuation Rule 3

The value of supply of goods received or made through an agent. For example there can be particularcases between Principal and agent where goods or services are supplied between them. There might be no value addition but cases like these will fall under the description of supply.

Valuation Rule 4

This contains valuation on the cost of acquisition basis and the manufacture cost basis.

Valuation Rule 5

This includes any residual or different method for determining the value for supply of goods and services which can be justified fairly.

Valuation Rule 6

This includes determination of the value with respect to certain supplies. It shall cover particular cases such as Life Insurance Business[1] and Foreign Currency Convertor under it.

Valuation Rule 7

This will completely be applicable where value for supply of service covers the case of pure agent. Exclusive application of this valuation rule is for Principal-Agent related cases.

These valuation rules are case specific, the GST council has also mentioned definite businesses such as the life insurance business and the foreign currency sale, etc and their particular valuation rules .

Conclusion

The Transaction Value concept was adopted under the GST Law by taking into consideration the Hon’ble Supreme Court judgements that the tax authorities cannot force the businessman’s to sell their goods at a specified price to maximise his profit.

Therefore, the taxpayers need to know the valuation rule and correctly decide the value of supplies in accordance with section 15 of CGST ACT, 2017 and the rules as prescribed. The taxpayers have to be cautious while paying the due tax for the purpose of saving additional tax liability with interest and penalty for increase in value by the Tax Authorities.

Read our article:What are the Things you Should Know about GST Business Loan?