The Goods and Service Tax (GST) brings and felicitate the concept of “One Nation One Tax” under the economical regime of India. Under this particular, presently GST is charged on the ‘Transaction Value’. The transaction value refers to the price actually paid or payable for the supply of goods or services between un-related prices which is the sole consideration for the supply. In this blog, we will discuss about Valuation of Supply under the Goods and services tax regime in India.

What is Valuation of Supply of Goods?

Valuation of Supply includes such amount, which the supplier is liable to pay but has been sustained by the recipient, and is not included in the price.

The Value of Supply under GST shall include any taxes, duties, cess, fees, and charges levied under any act, except GST, where the Compensation Cess will be ruled. The Valuation of Supply of goods and services is ordinarily known to be ‘the transaction value’.

- Section 15 of the CGST Act, 2017 contains provisions related to valuation of supply of goods or services made in different circumstances and to different persons.

- Section 15 (1) of the Central Goods and Services Act, 2017 (CGST Act) defines “Valuation of Supply of goods or services or both should be the transaction value, which is the price actually paid or payable for the said supply of goods or services or both where the supplier as well as the recipient of the supply are not related and the price is the sole consideration for the supply.” It further states in sub-section (2) about the details of various inclusions and exclusions from the ambit of transaction value.

Read our article:Step by step guide on how to check GST Registration Status

Who is a Principal?

As per the Section 1 (88) of the Central Goods and Services Tax Act, 2017, it defines the term “principal” as a person on whose behalf an agent carries on the business of supply or receipt of goods or services or both.”

Common examples of the principal-agent relationship can be hiring of a contractor to complete construction of any building by the Project owner. In such instance, the principal is the individual reaching for the service, while the agent is performing the work.

Who is an Agent?

As per the Section 1 (5) of the Central Goods and Services Tax Act, 2017, it defines agent as a person, including a factor, broker, commission agent, del credere agent, an auctioneer or any other merchant agent, who carries on the business of supply or receipt of goods or services or both on behalf of any other.

A DelCredere agency is a category of principal-agent relationship where the agent acts not only as a salesperson or broker for the principal but also acts as a guarantor of credit extended to the buyer.

What do we understand by Principal and Agent Relationship?

Explanation of principal – agent relationship has been detailed in Schedule I of CGST Act, 2017 vide Circular No. 57/31/2018-GST dated 04/08/2017. In terms of said Schedule I of the Central Goods and Services Tax Act, 2017 (CGST Act), the supply of goods by an agent on behalf of the principal without consideration has been deemed to be a supply.

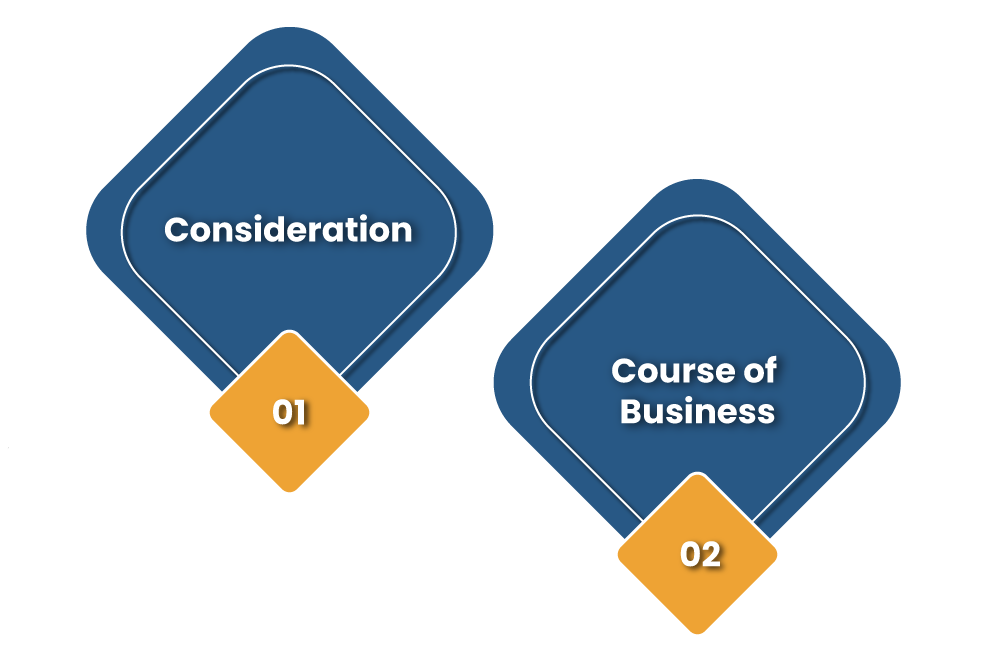

Branches of any Supply under GST

The two branches of any supply under GST are-

Consideration

The consideration is not abiding in any such transaction, in which a transaction does not drop down within the scope of any supply. There are certain scenarios, as provided in Schedule I of the CGST Act. Supply of goods is stated as follows:-

“Supply of Goods”—

- By a principal to his agent where the agent undertakes to supply such goods on behalf of the principal; or

- By an agent to his principal where the agent undertakes to receive such goods on behalf of the principal.

It is well observed that not all the activities and transaction between the principal and the agent and vice versa allocate within the scope of the specified entry.

- Firstly, the supply of services between the principal and the agent and vice versa is apart from the ambit of the said entry, and would consequently require “consideration” to consider it as supply. This would be liable to final calculation of GST.

- Secondly, the element recognized in the definition of “agent”, i.e., “supply or receipt of goods on behalf of the principal” has been contracted in this entry.

In the Course or Furtherance of Business

Section 7 of CGST Act 2017 defines scope of Valuation of Supply under GST. As per clause (a) of sub-section (1), supply includes all forms of supply of goods or services or both made for a consideration in the course or furtherance of business.

In Goods and Services Taxes law, the supply of goods, services and supplies made by principal to his agent or agent to his principal shall be liable to tax even any such transactions does not contain any consideration for such supplies.

Conclusion

For determining relationship would addresses few questions such as; whether invoice for further Valuation of supply of goods on Principal’s behalf is issued by agent or not. Any provision of services from principal – agent and vice versa would fall within the Entry 3 as herein invoice for the supply is issued by agent. In scenario, when the invoice is issued by the agent to his customer in the name of the principal, such agent do not fall within the ambit and scope of Schedule I of the CGST Act[1].

When the goods are being secured by the agent on behalf of the principal, those will get invoiced in the name of the agent. The forthcoming provision of the said supplies and services by the agent to the principal would be covered by the provided entry in the Schedule I of the Central Goods and Services Tax Act, 2017. To get such more clearance in the topics of valuation of Supply under the regime of GST, you may please connect to our CorpBiz professional as soon as possible.

Read our article:How to apply for GST registration certificate online?