The applicant has engaged in the manufacturing and rendering of ‘Poultry Meal’ and ‘Poultry Fat.’ Both the products are used as one of the protein raw material for the manufacturing of aquafeed industries, animal feed industries.

The major raw material for the manufacturing of poultry meal and poultry fat is chicken wastages such as chicken legs, chicken head, intestine, feathers, skin, etc. One can buy from the chicken stall owners in twin cities and other parts of the State. The applicant sought the ruling with regard to the HSN codes[1] and the Goods and Services Tax rate in respect of “poultry meal” and “poultry fat” supplied by their unit.

Read our article:Latest: Government unable to pay state’s GST compensation share

Held by AAR

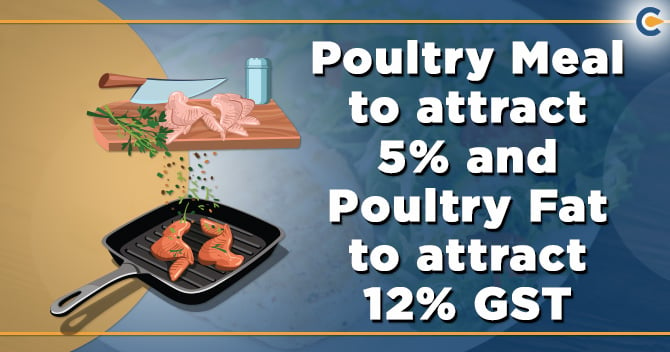

The Authority consists of the Additional Commissioner of State Tax, J. Laxminarayana, and the Joint Commissioner of Central Tax, B. Raghukiran ruled that the product “poultry meal” is classifiable under Chapter Sub-Heading 2301 10 90 of the 1st schedule to the Customs Tariff Act, 1975. The supply for the same attracts GST rate of 5% (2.5 % CGST and 2.5% SGST) under “Sl. No. 103 of the Schedule-I of the Notification No. 01/2017-CT (R), dated June 28, 2017”.

The Authority further ruled that the product “poultry fat” is classifiable under Chapter Sub-Heading No. 1501 90 00 of the first schedule to the Customs Tariff Act, 1975 and the supply of the same attracts GST rate of 12% (6% CGST and 6% SGST/UTGST) vide entry “No. 19 of the Schedule-II of Notification No. 01/2017-CT(R) dated July 28, 2017”.

Ruling

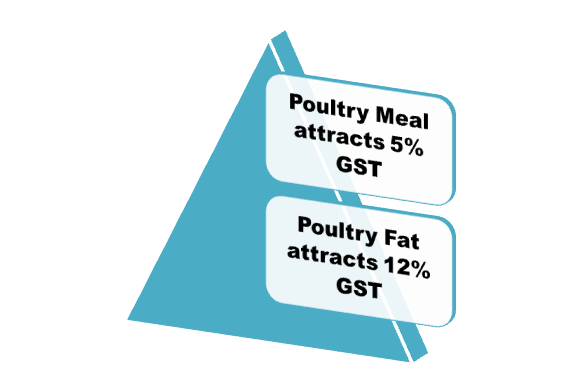

HSN Code and rate of tax regarding the supply of ‘poultry meal’

The product “poultry meal” is classifiable under a Chapter Sub-Heading No. 2301 10 90 of the schedule first to the Customs Tariff Act, 1975, and the supply of the same attracts GST rate of 5% (2.5 % CGST + 2.5% SGST) under Sl. No. 103 of the Schedule- first of the Not. No. 01/2017-CT (R), (as amended) on dated 28.06.2017

HSN Code and rate of tax regarding the supply of ‘poultry fat’

The product “poultry fat” is classifiable under Chapter Sub-Heading No. 1501 90 00 of the first schedule to the Customs Tariff Act, 1975 and the supply of the same attracts 12% GST (6% CGST + 6% SGST/UTGST)vide entry No. 19 of the Schedule-II of Not. No. 01/2017-CT(R), (as amended) on dated 28.06.2017

Read our article:CBIC notifies a new format for E-Invoice under GST