Non-Convertible Debentures (also known as NCDs) are one of the most efficient ways of fundraising for the NBFCs. The major chunk of borrowers in the NCD market comes from the NBFC segment. The RBI has tightened the regulations for Non-Convertible Debentures i.e. NCDs offered by NBFC. Many experienced investors favor Non-Convertible Debentures (NCDs) as the primary source of investments. NCDs allow the investor to lock their fund for an extended time at a higher interest rate.

Non-Convertible Debentures as Financial Instrument

- Non-Convertible Debenture is referred to as a financial instrument used by the organization for efficient fund raising. The companies conduct such activities via the public issue of shares. In laymen term, Non-Convertible Debentures can also be called a debt instrument.

- Non-Convertible Debentures has a fixed tenure and individual who invest the fund in these avail regular interest at a specific rate.

- Some debentures could be transformed into shares after a certain period. This is typically done with the approval of the owner. However, this is not true with Non-Convertible Debentures; this is the only reason why they are recognized as Non-Convertible Debentures.

- Non-Convertible Debenture i.e. NCD is also issued by the Non-Banking Financial Company with an initial maturity of one year and issued via private placement.

How is a Non-banking financial Company dependent on NCDs?

The majority of NBFCs procure funds via the issuance of debt securities or capital. Apart from that, they also raise funds by issuing debenture through private placement or public notice. Therefore, a significant increment in the borrowing of Non-Banking Financial Company has been witnessed via issuance of debenture, particularly in the form of the private placement.

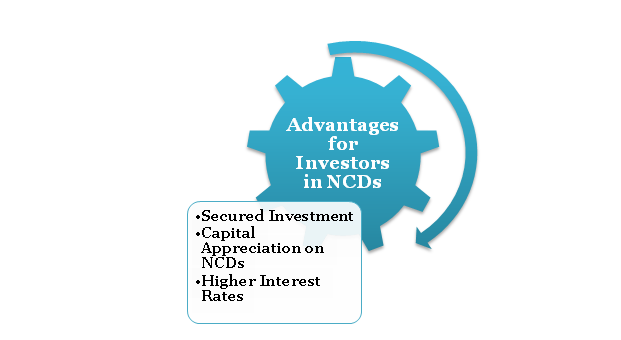

Investor’s Benefits in the NCDs Issued by NBFC

The significant advantages for investors in NCDs issued by Non-Banking Financial Company are as follow:

Higher Interest Rates

Non Convertible Debentures i.e. NCDs issued by NBFCs typically pays interest rate ranges from 150-177 basic point, which is greater than what mainstream banks pay on their FDs i.e. fixed deposit. NCDs issued by NBFCs possess a healthy reputation and are well-capitalized. And since the issuance of these NCDs is closely regulated by RBI, it can act as a sign of positivity for the investors seeking secured funding options.

The rate of interest is not stable on other modes of investment, therefore, in such a scenario, the NCDs seems to be a secured and efficient fundraising option for the investors.

Capital Appreciation on NCDs

Apart from reaping a higher interest rate, there is another benefit in investing funds in NCDs offered by NBFC. In the event, if the rate falls from 25-30 basis points from the existing levels, then the investor rejoices capital appreciation on the NCDs which is inevitable in their market price.

Secured Investment

The debentures typically have got either first or second charges on the issuer’s assets. Henceforth, they are secured when contrasted with other forms of investment. This renders an added benefits as well as higher return with capital appreciation.

Risk Aspects of Non –Convertible Debentures Issued by NBFC

An investor should adopt a holistic approach while investing their fund debt instrument like NCDs. In general, NCDs may offer the following risk to the investor:-

- NBFCs encompass a diverse class of assets. NBFCs are categorized into two levels i.e. low-quality NBFC and high-quality NBFC. Before investing, make sure to check the credit rating of the NCDs. The credit rating reflects the repayment ability of the issuer. It is advisable to consider the credit rating as the parameter for determining the repayment capacity of the issuer.

- About two decades back, Reserve Bank had imposed several regulations on NBFCs on account of capital adequacy and asset clarification. Such regulations caused severe financial turbulence for the NBFCs operating at that point in time.

NCDs Features Issued by NBFC

The Features of non-convertible debentures issued by NBFC are given below:

Taxation

The tax implications of the investor on NCDs depend on the tax bracket related to the investor. In case if the investor decides to sell the NCDs within a year then STCG shall be applied in the view of the income tax slab rate of the investor. In case if investors opt to sell the NCDs before the maturity date, then LTCG shall be applied at twenty percent with price indexation.

Credit Rating

The credit rating agencies hold the responsibility for judging the creditability of the existing NBFCs across the country. The companies with low credit ratings typically lack to potential to counter debt obligation. Likewise, the company with a higher credit rating is good at handling debt obligations. Henceforth, credit rating acts as the key performance indicator of any lending company.

Interest

The NCDs offer a comparatively better interest rate in contrast to convertible debentures. The bandwidth of interest rate that NCDs offer falls between 8 to 12%. The interest payouts are estimated on a monthly, quarterly, half-yearly, or annual basis. The NCDs also offer the cumulative payout option.

Read our article:How does a Company Issue Debentures to the Public?

Who Can Issue Non-Convertible Debenture?

Any entity or NBFCs can issue Non-Convertible Debentures provided they meet the following criteria:-

- The corporate or NBFCs must have a minimum of net owned fund of Rs 4 crore. The latest balance sheet should reflect this figure clearly.

- The company has been sanctioned a term loan by the financial institution or banks.

- The bank must tag the borrower account as the standard asset. The classification of the borrower account of the company is done as Standard Asset by the financing banks or institutions.

Underlying Conditions for the NCDs Issuance in NBFC

- The financial standing of an organization must be shared with the prospective investors on account of standard market practice.

- The investor must avail of the investor’s certified copy showing that the company has complied with RBI’s stipulates regarding eligibility criteria.

- The company should be a law-abiding entity and must adhere to the regulations drafted under the Companies Act, 2013[1]

- The issuance of the debenture certificate must be done as per the timeline mentioned in the Companies Act, 2013.

- The NCDs comprises a face value that carries a coupon rate to face value in the form of zero-coupon instruments is evaluated by the entity.

Bylaws Associated with Placement of Debentures or NCDs

In according to the Companies Act, 2013 and Rules (Company’s Act),

- Section 42 – provide directions concerning the invitation or offer for subscription of securities on private placement and

- Companies (Prospectus and Allotment of Securities) Rules, 2014 provide legal direction regarding Private Placement

Section 42 in tandem with Rule 14 applicable for the following:-

- Private placement of securities via issuance of the offer letter.

- The number of individuals about the avail of the securities.

- The method w.r.t accumulation is of money payable toward security’s subscription.

- The minimum threshold for investment size for a subscription.

- The maximum timeline for allotment of security.

- The maintenance of records and offer letter with the SEBI and with Registrar, in case of a listed organization.

- Filing related to return of allotment with the registrar.

However, the Revised Guidelines have bifurcated the issues related to a private placement into two categories:

- Category A: A limit of two hundred subscribers during a financial year.

- Category B: No restriction of subscriber’s numbers.

Rule 18 of Companies (Share Capital and Debentures) Rules, 2014 and Section 71 of the Companies Act, 2013 deals with Debentures

Section 71 of Companies Act, 2013 in tandem with Rule 18 provides provision in relation to the tenure of secured debentures,

- Its nature of security must be defined

- The amount of debenture redemption reserve i.e. DRR that must be taken care of.

- Procedures w.r.t to the appointment, roles, and eligibility of debenture trustee and meeting of debenture holders, etc.

As per section 71(4), every organization rendering debentures must underpin a DRR account with the profit which is available for dividend’s payment. The amount transferred to such account will be used for the redemption of such debentures.

Keep in mind that as per Rule 18(7) (b) (ii) of Companies (Share Capital and Debentures) Rules, 2014, no DRR required to be maintained for debentures which are privately placed by NBFCs.

Section 77 of the Company Act, 2013 Seeks Registration of Charges

As per Section 77 of the Act, 2013 every organization who created a charge on its asset/property, be it tangible or intangible, requires to register the particulars of the charge with the Register within 30 days timeline of the creation of property.

For Category A

It is mandatory for NCDs to be fully protected in favor of subscribers.

For Category B

The issuer can also create security in favor of its subscribers.

In the view of NBFCs (Acceptance of Public Deposit) Directions, 1998 – the debenture should be protected by mortgage of immovable property or other forms of the asset of the issuer company. The creation of security via mortgage seeks registration under this section.

SEBI Regulations

SEBI (Issue and Listing of Debt Securities) Regulations, 2008 applies to:-

- Public issue of debt securities.

- The listing of debt securities introduced via private placement or public issue on a well-known stock exchange.

Henceforth, these regulations would not apply to privately placed debentures in the absence of listing.

SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2009

These regulations govern the issuance of convertible debentures on a partisan basis by listed Non-Banking Financial Companies.

Guidelines Issued by RBI on Non-Convertible Debentures

- The issued guideline shall apply on Non-Convertible Debenture (NCD) with a maturity period of one year and issued via private placement.

- Reserve Bank vide notification released on February 20, 2015, unveiled directions related to Private Placement of NCDs possessing a maturity period of more than one year by the NBFCs.

- It doesn’t apply to tax-exempt bonds offered by NBFC.

- The NBFCs derives a Board approved policy regarding resource planning and periodicity of the private placement

- Reserve Bank has outlined the direction majorly for issuing of a private placement of NCDs of two categories:

- Category A- With a maximum subscription of less than one crore rupees.

- Category B- With a minimum subscription of one crore rupees and above.

Conclusion

NCDs are undoubtedly the best debt instrument for companies seeking prompt and substantial funding for growth or meeting other business goals. Also, it is less riskier than other modes of investment on account of profitability or rate of return. But to avail of such benefits, the companies have to lock down funds till the completion of the maturity period. It should be kept in mind that unlike FDs i.e. fixed deposit NCDs cannot be prematurely withdrawn.

Read our article:An Inclusive Guide on Contribution of Emerging Technologies toward NBFCs