Job work under GST means any treatment or process initiated by an individual on goods belonging to a registered entity. Thus, we can say that job worker is the registered or unregistered person whose job responsibility is managing or processing the goods of a registered entity whereas the principal is that registered person on whose behalf undertaking of job work takes place. As mentioned in Section 19 of the CGST Act, 2017, any person that supplies goods to the job-worker is the principal.

Concept of Job Work under GST Act

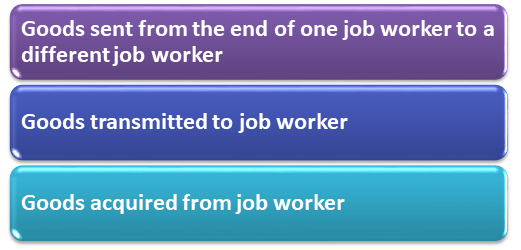

Job workers have a significant role to play in the economy of India due to their engagement in the input or unfinished goods processing. In four points, we are explaining the concept of job work under GST-

- The principal manufacturer would perform its duty by sending input or capital goods.

- Input or capital goods get sent without tax payment to a job worker and beneath intimation.

- In case of any requirement, goods would reach into the hands of another job worker from one job worker.

- Finally, after the job work gets over, the principal manufacturer would receive back the goods without tax payment.

The GST law has boosted this sector in growing vigorously and claiming tax credit on job work supplies has become convenient with the GST law. Let’s understand the things by an example-

Example: – Job workers are the small manufacturers involved in manufacturing bottle bodies along with their caps in the plastic bottle industry. Job worker obtains the raw material from the principal manufacturer, and job worker transfers the finished goods to the principal manufacturer after completion of the processing process.

Job Work under GST- Procedure

The principal manufacturer needs to construct a ‘Delivery Challan’ by following the prescribed format. The motive behind this is to send semi-finished goods or inputs without payment of duty and also without ITC reversal to a job worker. The Delivery Challan must hold the following information.

The information’s are as follows-

- GSTIN of the consignor along with the consignees’ GSTIN

- Form GSTR-1 represents the details concerning the challans.

- With the help of Form GST ITC-04, details of challans should get filed.

- On a quarterly basis, Form GST ITC-04 requires submission until the 25th day of the month.

The Form GST Input Tax Credit- 04 carries the following details-

Responsibilities of the Principal

- Account maintenance of input as well as credit goods

- As per the invoice rules (Rule 10) under the Goods and Services Tax Act, the principal is the flag bearer of issuing the challan to the job-worker for the capital goods and inputs

- Making a declaration that the additional place of Job workers’ conducting his business is his premise in case of direct export of goods to the third party person and the job worker has not gone through the process of GST registration

- The jurisdictional officer must get intimated for maintaining the details of proposed input goods. Besides this, the job worker delivers the processing nature.

E-way Bill for Job Work under GST Provisions

- GST provisions on the e-way bill give an implication that all the registered persons who are responsible for the movement of goods having consignment value surpassing the amount of Rs 50,000 even in those cases where movement takes place for reasons other than supply must generate e-way bill. Thus, the e-way bill gets generated even in the case of goods movement for job work.

- Irrespective of the consignment value, e-way bill would get generated either by the job worker who is registered or by the principal manufacturer in the matter of inter-territorial movement of goods.

Read our article:GST on Food Services and Food Items: All that you need to Know

GST Rate on Job Work

- The GST council has brought a reduction in the goods and service tax rate on the engineering job work. Earlier, the GST rate was 18%, and now the GST rate stands at 12%.

- In the case of diamond supply job work, the GST rate was 5%, and now the GST rate is below 1.5%.

- Clarifications in the latest GST circular 126/45/2019 confirms that every registered taxpayer under job work would get imposed with 12% goods and service tax and consequently the taxpayers under GST job work who are yet not registered would have to give 18% GST rate as well.

- In the case of job work on Agriculture, animal husbandry, fishing, and forestry, the GST rate is 0%.

- In the case of job work on animal rearing and cultivation related services, the GST rate is 0%.

- In the case of job work on the processing of leather, skins, and hides, the GST rate is 5%.

- In the case of job work on the Textile along with the textile products and job work on newspaper printing, the GST rate is 5%.

Return of Goods to Principal

The goods send out must get received back by the principal manufacturer within the time frame-

- Input Goods- 1 Year

- Capital Goods- 3 Years

Under job work, the return of goods to the principal is one of the most crucial aspects.

Exemptions of GST on Job Work

- Under the Ministry of Agriculture, Cooperation and Family Welfare, services rendered by the National Centre for Cold Chain Development

- Services by means of retail packing, pre-cooling, waxing, ripening, labeling of fruits, and pre-conditioning

- Slaughtering of animals

- Cultivation of plants as well as the rearing of many life forms of animals, an exception is the horse rearing for fuel, food, raw material, or other same kinds of products

Waste Generated at the Premises

- As stated under Section 143(5) of the CGST Act, 2017[1], the registered job worker might have to supply the waste generated at the job worker premises from his business site on payment of tax, in this case, job worker will pay the tax.

- On the other hand, if a job worker is unregistered, then the principal manufacturer would go on clearing waste of such kind, and the goods and service tax would be payable from the principal manufacturer end.

Cases in Which Principal Manufacturer can Avail Credit

The principal manufacturer can avail credit on-

- Goods directly supplied to job worker

- Input tax paid on inputs given to job worker

Bottom Line

Through this blog, you might have understood the concept of job work under GST Act. We have covered procedures related to job work under GST to make you know about those essential details that Challan must hold. Our Experts at Corpbiz would make you GST ready and simplify the process for you as well.

Read our article:Elucidation on GST Refund Issues – Recent Updates