Section 7 Schedule 1 of CGST Act talks about the Activities to be treated as Supply even if made without consideration. The supply made between any related persons for inadequate or no Consideration is covered under Schedule I of the GST Act. Such transactions will be treated as ‘Supply’ only if it happens in furtherance or course of business.

Activities Treated as Supply under Section 7 Schedule 1

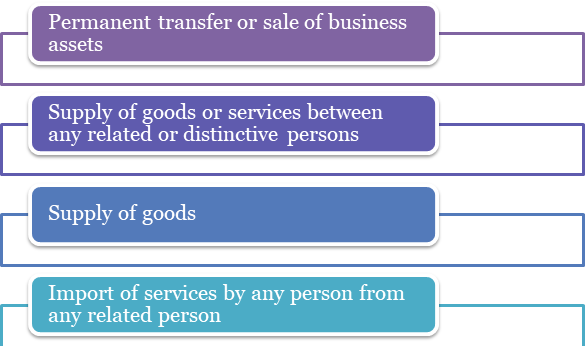

The following are the activities under Section 7 Schedule 1 that are treated as supply even if it is made without any consideration. Those activities are as follows:-

Permanent transfer or sale of business assets where Input Tax Credit has been availed on such assets

Permanent transfer or sale of business assets where ITC has been availed on an asset can be treated as supply without consideration. GST Registration is applicable on sale of business assets only; it does not apply on sale of personal property.

What is Permanent Transfer?

Permanent transfer means transfer of goods without any intention of receiving back the goods.

What is Input Tax Credit?

ITC means that at the time of paying taxes on output, any person who has already paid on the input can reduce the tax.

Situations qualified as “Supply”

When there is no permanent transfer of goods, it will not qualify as “Supply”.

For Example- Goods sent for work or for testing or certification will not qualify as supply as there is no permanent transfer.

When ITC has been claimed?

When ITC has been claimed on any business assets, other than sale of those assets, it will qualify as “Supply”

Donation of business assets or discarding in any other manner other than as a sale will qualify as ‘Supply’, when ITC has been claimed.

Supply of goods or services between any related or distinctive persons

Supply of goods or services between any related or distinctive persons as mentioned in Section 25, when made in the furtherance or course of business are determined as supply without consideration.

Who is a Related Person under GST Law?

Persons shall be considered to be related if they fall under any of the categories mentioned below-

- The business together control any other business;

- Persons under common management;

- Officer or director of one business is the officer or director of another business;

- Members of the same family;

- Businesses are legally recognized as partners;

- Any person who holds at least 25% of shares in another company either directly or indirectly;

- Any person who controls the other person directly or indirectly;

- Any employer and any employee.

It also states that gifts not exceeding INR 50,000 in value in a financial year by any employer to any employee will not be treated as supply of goods or services.

What is the taxability of supply between any related persons?

Supply made in between related persons with consideration will constitute as ‘Supply’ like another transaction.

The supply made between any related persons for inadequate or no Consideration is covered under Schedule I of the GST Act. Such transactions will be treated as ‘Supply’ only if it happens in furtherance or course of business.

Supply of goods

Any supply between agent and principal will be liable to pay GST. Agent and principal both will be liable to pay GST jointly. The person who is paying GST can later claim ITC. These are the following conditions-

By An Agent to the Principal

Supply of Goods by any agent to the principal where the agent receives the goods on behalf of the principal is considered as supply without consideration. In this context, any supply between agent and principal will be liable to pay GST.

By a principal to the agent where the agent undertakes the supply of such goods on behalf of the principal

Following are the methods for appropriate valuation-

- Open market value is considered as the value of the supply between two unrelated parties. When a supply is made in between two related parties, there is a high chance that the prices will be influenced by the relationship.

For example- One company sells goods to any related party at INR 1500 and to any unrelated party at INR 2000. In this particular case we can say that the relationship has manipulated the pricing of the seller. Hence, for the purpose of valuation, INR 2000 will be considered.

- If the open market value can’t be determined, then the value of goods of similar kind and quality will be considered.

For example- If X Company makes entire sales to Y Company, and then the above method of valuation will not be considered. They can consider Z Company who sells similar goods as X Company at INR 1200. Therefore, the valuation for this purpose would be INR 1200.

- If both above mentioned methods does not provide a appropriate valuation, then a valuation based on cost that is total cost of production or residual method will be considered.

Import of services by any taxable person

Import of services by any taxable person from any related person or from any of their other business outside India for business purpose only, shall be treated as supply.

For example, ABC Ltd. is registered in the US by X Ltd. along with Y Ltd. in India. Services imported by Y Ltd from ABC Ltd. without any consideration, then the import will be considered as a supply. GST will be paid by Y Ltd. on Reverse Charge Mechanism.

Conclusion

This blogs deals with transactions between any related persons and other activities that can be treated as ‘Supply’ under GST even if made without any consideration. GST will be applicable on all these transactions. These are listed in Section 7 Schedule 1 of the CGST Act, 2017[1]. The transactions are mostly between entities that are related or between any agent and a principal. The entities, who pay GST, can later claim it as Input Tax Credit.

Our CorpBiz professionals will be at your disposal if you want expert advice on any aspect of GST implications, registration or compliance, and any Government Licensing. We will help you to complete all your compliances concerning all the issues related to GST applicability-based as per your desired activities, ensuring well-timed completion of your work.

Guide-on-Section-7-Schedule-1-of-the-CGST-ActRead our article: Know the Provisions for availing 2 GST Registration on One PAN Card