GST is a target based tax on the ingestion of goods and services. At all platforms, right from manufacture up to final consumption, it is proposed to be levied with credit of taxes paid at forgoing stages obtainable as setoff. It means that only the value’ addition will be taxed’ and ‘burden of tax’ is to be borne by the final consumer.

Registration is the fundamental requirement for taxpayers’ identification in any tax system, safeguarding tax compliance in the economy. Under the GST Law, Registration of any business entity implies obtaining a unique number to collect tax on behalf of the government from the appropriate authorities and to avail ‘input tax credit’ for the taxes on his private supplies. Therefore, a person can neither collect tax from his customers nor claim any ‘input tax credit’ of tax paid by him without GST registration.

In this blog, you will get to know the overall updates on the latest orders decided by AAR (Authority of Advance Ruling) on the GST applicability on different considered items.

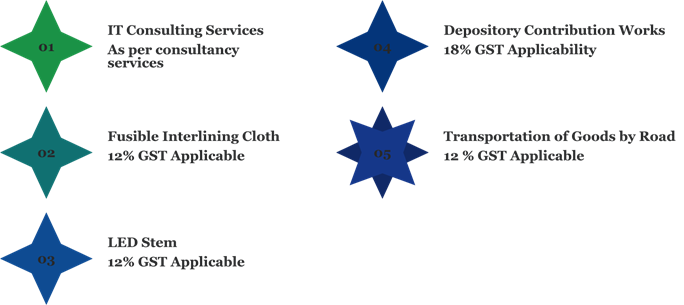

IT Consulting Services: GST is applicable in Oracle ERP

GST applies to IT software related consulting services in Oracle ERP, which has been ruled by the Tamil Nadu Authority of Advance Ruling (AAR).

Facts of the Matter

Mr. Rajesh Rama Varma, the applicant in the case, provides IT software related consulting services to Doyen for a consultancy fee stated in the consultancy agreement in the area of Oracle ERP with relation to Oracle Financials.

His job was that of a Consultant to give support services owned by the US client based out of Boston as part of the Contract to the Oracle ERP. The 1st Contract was among US clients, and Principal, along with a part of the service, was tight up to him. The consultancy fee for his services was based on an hourly basis according to Contract in USD of $33.90 per/hr.

Based on the conversion rate of INR/USD, the fee was decided to be paid in equivalent INR on the average prevailing rate of the previous three months. Moreover, while raising the invoice by him on the Principal, the GST taxes would be charged separately. The Contract is valid until December 2021 and currently in force.

Rational of the Ruling

- Mr. Rajesh Rama Varma (applicant) sought advance ruling on the issue of if the GST applies to IT software in Oracle ERP related consulting services.

- The Authority ruled that GST is applicable to IT software related consulting services in Oracle ERP. The Authority consisted of members Manasa Gangotri Kata and Thiru Kurinji Selvan V.S. It was held, as the said activity gratifies the conditions of “Section 7(1) (a)” which is a supply under GST.

- This supply is a supply of services according to ‘Para 5 of Schedule II read with Section 7(1A)’. Therefore, the applicant is liable for the procurement of consultancy services to Doyen to pay GST appropriately.

Observation

In addition, this Authority cannot answer whether such a supply of services is ‘export of services,’ ‘zero-rated supply,’ and eligibility of refund. It is because they are not covered in Section 97(2) of the CGST/TNGST Act.

AAAR: 12% GST Applicable on Fusible Interlining Cloth

West Bengal Appellate Authority of Advance Ruling (AAAR) ruled that fusible interlining cloth falls under ‘HSN 5903’ as it is not a woven fabric. Therefore, 12% Goods and Service Tax (GST) applies to the fusible interlining cloth.

Facts of the Matter

- M/s. Sadguru Seva Paridhan Pvt. Ltd is the applicant of the case who has manufactured a fusible interlining cloth. The fusible interlining fabric used to be classified under Chapters 52 to 55 before 1989. It was clarified under vide Circular “No. 5/89 dated 15/06/1989”.

- A new ‘chapter note 2(c)’ was introduced in Chapter 59 of the Tariff in the Union Budget of 1989-90. It was led to the inclusion of textile fabrics under heading 5903, discretely or partially coated with plastic by dot printing procedure.

Contentions of the Parties

Consequently, the said chapter note 2(c) was omitted with effect from March 16, 1995, in the Union Budget of 1995. The item cannot be sorted under Heading 5903 after the removal of the said chapter note. The example copies of invoices indicate that it is sorting the product under sub-heading 5208, issued by the appellant.

According to the applicant contention, the WBAAR of Uttarakhand held that such fabrics would fall under ‘Chapter 52 or 55, 58 or 60’ of the Tariff Act and not Heading 5903 in which similar facts and circumstances the West Bengal AAR disregarded the judgment in the case of ‘Good wear Fashion Pvt. Ltd’.

The product merits classification under sub-heading 5903, which was contented by the respondents. Sub-heading 5903 contains products other than heading 5902, namely – impregnated textile fabrics, covered, coated, or laminated with plastics.

Observation

Chapter note 2 of ‘chapter 59’ of the Tariff should come under sub-heading 5903, which provides the description of products. The Appellate Authority of Advance Ruling observed that the claim of the appellant’s supporter does not hold good and the barring clause (4) of chapter note 2(a) of Chapter 59. Chapter 59 does not apply to fusible interlining cloth manufactured by the appellant, which is essential for being excluded from it.

As a result, the subject of the product qualifies classification ‘under sub-heading 5903 of the Tariff’.

The Appellate Authority of Advance Ruling has up-holded the Ruling of AAR’s opinion in this case. It consisted of members Devi Prasad Karanam and A.P.S. Suri observed that fusible interlining cloth falls under HSN 5903 and is not a woven fabric. Therefore, 12% Goods and Service Tax (GST) applies to it.

AAR rules that LED Stem are Applicable for GST: 12%

In a recent order, Tamil Nadu Authority for Advance Ruling (AAR) has ruled that supply of LED stem (long bulb) is taxable at the rate of 6% CGST and with 6% SGST. It is an outdoor lighting fixture with LED combined intimately within them.

Facts of the Matter

- lnventaa LED Lights Private Limited is the applicant in this case. They were engaged in the manufacture, design, and supply of LED Lights of numerous applications in a wide range of sizes.

- They were also engaged in fittings with the fixtures, voltage with accessories, fittings that are made up of Plastic, Aluminium, and Steel or a combination thereof.

- The applicant has indicated that they have developed a LED Stem (Long bulb), which saves power up to 60% compared to the CFL bulb, and has a 360-degree light output at the same time. This conventional LED bulb delivers only a 180-degree light output.

Rational of the Matter

lnventaa LED Lights Private Limited, the applicant, in this case, had applied for an Advance Ruling seeking the Rate and the classification for the products apportioned by them. They were seeking an advance ruling in terms of Category ‘A’ products. Those are as follows: – LED Outdoor Lights, LED Long stem bulb utilizes in LED Garden Lights and, LED Bollard Series.

The considered Issues

- “Does the supply of full product of the LED stem with fixtures or fittings are single, composite, or mixed?

- “Whether the supply of full product – LED stem is applicable GST Tariff code and Rate?”

The Coram (appearance of a person before another individual or a group) applied the explanation (iii) and (iv) to Notification No. 1/2017 – Central Tax (Rate) Dt. 28-06-2017 by the consisting members such as Mr. Kurinji Selvaan V.S (Member, TNGST) and Ms. Manasa Gangotri Kata (Member, CGST).

Moreover, the heading and chapter, tariff heading, sub-heading shall mean respectively as a heading and section, sub-heading, tariff item, as specified in the “First Schedule to the Customs Tariff Act, 1975”.

The rules for interpreting the First Schedule to the Customs Tariff Act 1975[1] will include the classification of goods, the General Explanatory Notes of the First Schedule for interpretation, and Section and Chapter Notes.

Observation

The bench found it evident that Chapter 94 falls under Section XX from further understanding, which also covers `Miscellaneous Manufactured Articles.’ There are few technical parameters propounded by the ruling, which are as follows:-

- It was also opined that light fittings and Lamps could be made of any material and any source.

- Those light fittings and lamps are not covered under this heading by the specific exclusion in the Chapter Notes, which were covered under Chapter 85.

- Lamps are covered under CTI-I 9405 for exterior lighting.

The product is a LED lamp fixture with an LED light that is classifiable under CTH 94054090 as ‘other electric lamps and light fitting,’ which were integrated into it because it can function independently as garden lights.

Read our article: Clarifications made by CBIC regarding GST on Director’s Remuneration

AAR Rules that GST is applicable on Depository Contribution Works: 18 %

The ‘Authority of Advance Ruling’ (AAR) Tamil Nadu ruled that “Depository Contribution Works” is categorized under SAC 99873. The Depository Contribution Works applies to GST in which the Rate of tax is 9% as SGST, and 9% of CGST is applicable.

Facts of the Matter

M/s Tamil Nadu Generation, and Distribution Corporation Limited (TANGEDCO) is the applicant in this case, which is a subsidiary of Tamil Nadu Electricity Board Limited (TNEB).

TANGEDCO Ltd. and TANTRANSCO LTD are registered utilities for distribution and Transmission of Electricity respectively under the Electricity Act, 2003, and both are two subsidiary companies of TNEB Ltd. (Holding company).

TANGEDCO and TANTRANSCO, two subsidiary companies, arrived into transactions between them in the course of a generation of electricity, transmission, and distribution of the same in Tamil Nadu. M/s Tamil Nadu Generation and Distribution Corporation Limited (TANGEDCO) sought advance ruling on the applicability of GST on the transactions between “TANGEDCO Ltd. and TANTRANSCO Ltd.”

Rational of the Matter

Manasa Gangotri Kata and Thiru Kurinji Selvan V.S. are the members of the Authority consist ruled that GST applies to the transfer of capital assets and the supply of operation and maintenance materials used in the regular day to day functioning. They opined that TANGEDCO is a ‘Government Entity”.

GST applies to TANTRANSCO, as the same is the supply of Service to the deployment of employees. Nevertheless, GST does not apply to the transactions of physical fund flow by repayment of the existing loan, availing of fresh loans, etc. between the companies.

Income such as transmission Scheduling, charges, and Systems Reactive Energy Charges, Operating charges, etc. should be considered into the context on an actual basis without any interest component.

Observation

Both are the transaction in money on such fund flow by the applicant received from open access consumers and adapted through payable to “TANTRANSCO’.

Moreover, it was ultimately propounded that “Depository Contribution Works is applicable Rate of tax is CGST @ 9% and classifiable under SAC 99873. It was considered along with as per “SI. No. 25 of Notification No. 11/2017-C.T. (Rate) dated 28.06.2017”.

Moreover, applicable of SGST @ 9% was clarified y as per “SI. No. 25 of Notification no. II (2)/ CTR/ 532(d-14)/2017 vide G.O. (Ms) No. 72 dated 29.06.2017”. AAR has clarified that it got amended, and the same is not exempted in the eyes of the law.

AAR Rules that GST is applicable on Transportation of Goods by Road (Agreement of Supply of Services): 12%

12% of GST applies concerning the transportation of goods by road to the agreement of the supply of services. It was ruled by the Maharashtra Authority of Advance Ruling (AAR).

Facts of the Matter

POSCO India Steel Distribution Centre Pvt Ltd is the applicant in the case which is engaged in providing logistics management services and logistic consultancy services.

The applicant has entered into a rate contract agreement to supply services concerning the transportation of goods by road, i.e., steel coils in bulk by road, with its entity group companies, POSCO Mangaon MIDC, MAH Pvt. Ltd., and Dist. Raigad.

The concerning issue that the applicant sought advance ruling on the Matter is as follows:-

- “What will be the classification of the services under service codes 996511 or 996791or 996799 or any other?”

POSCO India Steel Distribution Centre Pvt Ltd issues the consignment note; nevertheless, the third-party transporter is the actual transportation which releases the consignment note and done through ultimately.

Rational of the Matter

A.A. Chahure and P. Vinitha Sekhar were the members consisting of the Authority who ruled that the Service supplied by them would be enclosed under “Heading 9965,” which covers ‘Goods Transport vice,’ Sub Heading 99651. Simultaneously, it includes under SAC 996511 and ‘Land Transport services of Goods’ also. GST will be applicable under the “Entry of the Notification 11/2017 (CT)” Rate dated 28 June 2017”, and will be covered accordingly.

However, the GST rate of 5% will apply as per subject to conditions provided that credit of input tax credit charged on goods and services used in spring the services had not been occupied. Moreover, the alternative GST Rate of 12% will be applicable, on condition that the applicant and goods transport agency will be choosing to pay central tax 6% under this entry on all the services GTA delivered by it.

Observation

Addressing the above issue of GST rate on the services, AAR ruled that 12% of GST will apply concerning the transportation of goods by road to the agreement of the supply of services.

AAR has also observed that the applicant cannot avail ITC because the third-party transportation is not charging any GST Services supplied by the applicant.

Conclusion

The greater test may essentially be around GST applicability for the institutions. Our CorpBiz group will be at your disposal if you want expert advice on any aspect of GST Registration and any kind of Government Licensing. We will help you to ensure complete compliances concerning all the issues related to GST applicability-based as per your desired activities, ensuring the fruitful and well-timed completion of your work.

Read our article: AAR: Applicability of GST & its Registration for Charitable Medical Stores & Security Service