Ministry of Finance has issued a clarification which was regarding the numerous queries on the issue regarding the GST payable on an amount charged by the Resident Welfare Association. It was for providing services and goods for the common use of an area by its members in a housing society or a residential complex.

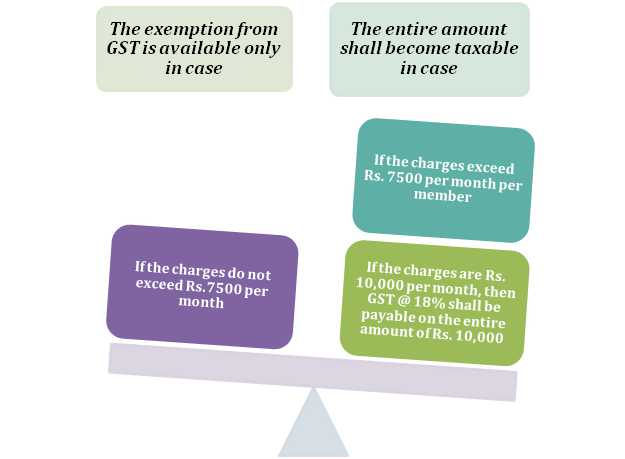

The Finance Ministry[1] has recently clarified in the circular that exemption from GST is available if the charges do not exceed Rs 7500 per month. Resident Welfare Association collects GST on fees charged from the members who own flats in their society. If the monthly payment of maintenance fees is more than Rs. 7500 per apartment per month and also the annual turnover of the Resident Welfare Association exceeds the defined limit of Rs. 20 lakhs by way of supply of services and goods. GST must be collected @ 18% on the monthly maintenance fees charged.

Registration Requirement for Resident Welfare Association

|

Aggregate Turnover of Society |

Monthly maintenance per member |

Exemption from Registration |

Remarks |

|

Less than Rs 20 Lakhs

|

Rs 7500 or less |

Exempt |

– |

|

Less than Rs 20 Lakhs

|

Rs 7500 (for some members less than Rs 7500 PM)

|

Exempt |

– |

|

More than Rs 20 Lakhs

|

Rs 7500 or less |

Exempt |

|

|

More than Rs 20 Lakhs

|

Rs 7500 or more (for some members less than Rs 7500 PM) |

Not Exempt |

The registration condition only arises when the aggregate turnover exceeds Rs 20 lakhs and monthly maintenance per member exceeds Rs 7500/- |

How shall the GST amount be calculated on RWA Charges?

For example, if maintenance charges are Rs. 10,000 per month per member, GST @ 18% must be payable on the entire amount of Rs per month. 10,000 and not on the left out amount after exemption (10,000-7500=2500). Therefore, GST will come out to be 10,000 multiply by 18%= 1800.

Read our article:Coupons and Vouchers under GST

Following are GST Clarification on Resident Welfare Association Charges

“Issue- What is an exemption limit under the GST on maintenance charges paid by residents to the Resident Welfare Association in a housing society?”

Clarification- Supply of service by RWA (unincorporated body or a non- profit entity registered under any law) to its members by way of the reimbursement of charges or share of contribution up to the amount of the Rs. 7500 per month per member for providing goods and services for the common use of an area for its members in the housing society or the residential complex are exempt from GST. Till Jan 25, 2018, the limit was Rs 5,000 per month per member.

“Issue- Can RWA Claim ITC on GST paid on Input and Services paid for making supplies to members?”

Clarification- RWAs are entitled to take ITC of GST paid by them on the capital goods such as water pumps, generators, lawn furniture, etc.), and other goods such as pipes, taps, other sanitary and hardware fillings, etc.) and also on input services such as repair and maintenance services.

“Issue-How must the Resident Welfare Association calculate GST payable where the maintenance charges exceed Rs 7500 per month per member? Is the GST payable only on an amount exceeding Rs 7500 or the entire maintenance charges?”

Clarification-The exemption from the GST on maintenance charges charged by an RWA from residents is available only if the charges do not exceed Rs 7500 per month per member. In case the charges exceed Rs 7500 per month, the entire amount will be taxable. For example, if the RWA maintenance charges are Rs. 9000 per month per member is levied, then GST @18% must be payable on the entire amount of Rs. 9000 and not on [Rs. 9000 – Rs. 7500] = Rs. 1500.

“Issue- Where the person has two or more flats in the housing society or residential complex, whether the ceiling of Rs. 7500 per month per member on the maintenance for the exemption to be available must be applied per residential apartment or per person?”

Clarification-A person who has two or more residential apartments in the housing society or the residential complex must normally be a member of the RWA for each residential apartment owned by him separately. The charges of Rs. 7500/- per month per member must be applied separately for each residential apartment owned by him.

Conclusion

As per the rules, Resident Welfare Association is required to collect GST on monthly subscription and contribution charged from its members if the payment is more than Rs 7500 per month per apartment and an annual turnover of RWA by way of supply of services and goods exceeds Rs 20 lakhs.

Resident Welfare Association is eligible to take Input Tax Credit (ITC) of GST paid by RWA’s on the capital goods and input services. The Finance Ministry in the circular clarified an exemption from the GST is available if the charges do not exceed Rs 7500 per month per member.

Read our article:Latest: Selective Applicability of GST Regulation by AAR

Recent Blogs

Get Free Expert Consultation

Impact Of GST On Educational Institutions And Exemptions

02 Sep, 2020

02 Sep, 2020 Reading Time: 4 Minutes

Reading Time: 4 MinutesThe Good and Service Tax (GST) is an indirect tax which has replaced the various indirect taxes which were being le...

Skill Mapping: Government deployed new portals to combat Unemployment

13 Jul, 2020Reading Time: 4 MinutesCentre for Monitoring Indian Economy has claimed the unemployment rate in India is escalating rapidly. With 27% of...

An Outlook on the Code on Social Security, 2020: Latest

07 Oct, 2020Reading Time: 3 MinutesCode on Social Security, 2020 was initiated in the Lok Sabha on 19th September 2020 vide Bill No. 121 of 2020...