GST is a consumption-based destination tax. A taxpayer has to be registered in all the states in which he is supplying/selling. Now, most banks have a pan-India presence, which means they are required to register in ALL states. In addition to this, banks provide services to their own branches and also to other banks. Transactions between subsidiaries are taxable under GST.

Owing to the nature and volume of other financial services (apart from regular banking services) provided by banks and NBFCs such as lease transactions, hire purchase, actionable claims, fund, and non-fund-based services, etc., GST compliance will be complex. This article deals with the place of supply of banking and financial services from the point of the customers and what they will be charged.

Government clarifies GST applicability on financial services

Goods and services tax apply to exit loads charged by mutual funds, the additional interest charged for default in payment of loan installments, and late payment charges levied by credit card companies, the government has said.

Securitization, future contracts, derivatives, and forward contracts in commodities, unless entailing actual delivery of products, will not be liable to the tax, which was introduced in July 2017. The comprehensive explanations for the financial service sector allotted in the procedure of Frequently Asked Questions (FAQs) pursues to address some relevant issues relating to the industry like levy of tax on free services.

For banks or ATMs will not be considered as place of business and will not generate GST registration, said by the government. In case the services are provided by multiple branches to any customer, the branch where the account of the customer belongs will pay the GST and other branches will be considered to deliver amenities to the main branch. Integrated GST will apply once in case of import of gold, on import, and not again when banks appropriate it.

Financial Services that are provided by banks to the Reserve Bank of India will be taxable as they are not protected by any of the exemptions or excluded from any provision provided by GST. But, the repo rate or reverse repo rate is exempted from the GST rates, as per the clarifications issued.

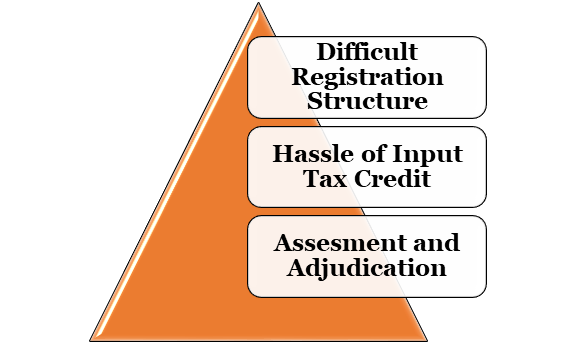

GST and Its Impact on Financial Sector

Difficult Registration Structure

Before implementing GST, all the banks and NBFCs have to maintain their service tax compliance via a centralized process of registration. When the banks have different branches in several states and union territories, the compliance registration was not required to be done distinctly.

Through GST, banks and NBFCs need to carry out tax registration distinctly for every branch they own. Meanwhile, GST is a destination-based administration; it has a multi-stage system. The tax that is received at every stage, and the tax already paid in the last step is reduced to the next level. No uncertainty that GST has rationalized the tax structure and helped the industry with improved cash flow, but GST compliance is still a test.

Read our article:GST Rates for Hand Wash and Sanitizers

Hassle of Input Tax Credit

Before coming of GST, banks and NBFCs were able to opt for a 50% reverse of CENVAT (Central Value Added Tax) acclaim that is developed from input services as well as inputs. The credit for CENVAT on capital possessions was reversed without any conditions. Nowadays, the relations for the reverse has been transformed, and for input service, input, and capital goods, only 50% of availed CENVAT is overturned.

The impact of GST on banks is excellent as they are 50% reduced credit on capital goods, and the cost of capital is raised overall. But, this can still be considered as a benefit because of a unified tax regime, the production costs are reduced, which increases profit.

Assessment and Adjudication

GST has its impact on the fiscal subdivision is seen in the form of assessment and adjudication changes. Before, banks and NBFCs have an alternative to a specific state controller, in which that branch was registered for assessment for service tax. Having GST every branch of banks and NBFCs has to justify its chargeable position in the particular state and provide a motive for input credit tax usage in different states.

Furthermore, under GST, numerous settlement establishments are involved that has led to delay in settlement as there are different opinions on one fundamental issue. Before GST, only one decision-taking authority was to be contacted for any fundamental issue, which was obviously viable, fast, and convenient for every bank.

Impact of GST on Banking Service

Banking service charges 15% service tax, which increased to 18% under GST. Similar indemnification, banking facilities will also become more exclusive to the customers due to increase in tax rates. Most banks have now applied transaction charges on cash withdrawals from different bank ATMs, cash withdrawals from branch.

Impact of GST on Banking Company

The impact of GST on Banking Company will pass on the tax obligation to its customers. However, their organizational and compliance effort will surge tremendously. Branch gives service to each other, which will be taxable under GST. This will increase the form-filling and, therefore, the operating costs. Good news for business customers. They can now entitlement input tax credit on the banking services paid on their business accounts.

Benefits of GST for Banks and NBFCs

Before GST, the banks were only able to obtain a partial credit of CENVAT and no VAT credit on obtained goods. Meanwhile, all the indirect taxes are included to GST, credit for GST applicable on procured goods can also be availed.

GST Impact on Financial Services Industry in India

The tax bracket has been augmented to 18%, which previously was 15% with service tax after introduction of GST. After beyond the ATM cash withdrawal limit, a certain charge plus tax is appropriate. However, it is supposed that this additional tax will be appreciated in the long run as the banks will be able to accept input tax credit benefits in an improved way.

Transactions Affected By GST

- Loans that are presented by banks and NBFCs are not exaggerated as they are money-to-money transactions. Henceforth, no GST is applicable on loan as well on the interest charged.

- In banks or NBFC, the rent can be supply of goods or supply of financservices, or it can be both of that attracts GST charges similar to the services and goods that are on lease.

- Leasing purchase is a procedure in which the purchaser of asset pays regular payments and takes ownership of the asset from the starting of the contract. Though, the possession is only relocated once all the portions are paid. In this type of transaction, both the cost price and the leasing charges are applicable to GST.

Conclusion

The impact of GST on banks and financial services is excellent as they are 50% reduced credit on capital goods, and the cost of capital is raised overall. But, this can still be considered as a benefit because of a unified tax regime, the production costs are reduced, which increases profit. CorpBiz shall be happy to serve you with any legal issues, be it establishing your financial institutions or compliances for GST or its registration.

Read our article:A Guide on GST Benefits for Small Businesses & Start-ups