In order to take the exemption related to Section 11 under NGO, the institution should be registered as trust. Moreover section 12A lay down exemption under section 11 as well as Section 12 of Income Tax Act, will not be accessible except the following conditions are satisfied

- The NGO is required to acquire 12AA registration with the Income tax Commissioner.

- Audit by qualified CA is necessary when income earned by the NGO is more than INR 2, 50,000 & the report is required to be provided while filing Form 10B.

Section 11(1) – Income Applicable to Charitable or Religious Purposes

Section 11(1) of the Income Tax Act[1] states that any income or profit derived from organization should be registered under religious or charitable trust. It should not include the total income of the trust to such extent where the income is applied or gathered for application. The exemption is allowed under specific conditions or on completion of those conditions. The conditions are as follows-

- In order to be eligible to claim any exemption, it is necessary that the income of the trust is applicable on such objects;

- A charitable NGO will have to apply for at least 85 % of the income for charitable motive only;

- If the income is spent on charitable purposes and it falls short of 85 % of the income derived during the previous year, then tax will be liable on such shortfall;

- Voluntary contribution or donations will be deemed to be the part of income derived from property held under trust.

Read our article:An Insight into New Era for Religious NGOs under Taxation

Section 11(2) – Accumulation of Income in Excess of Specified Limit

When 85% of income derived from property of trust is not applicable or the income earned is not used for charitable purpose. But the income is accumulated for application of charitable purposes in India then the exemption can be claimed for the accumulated income in excess of 15% limit after complying with few conditions-

Following are the conditions that are required to be complied, they are as follows:-

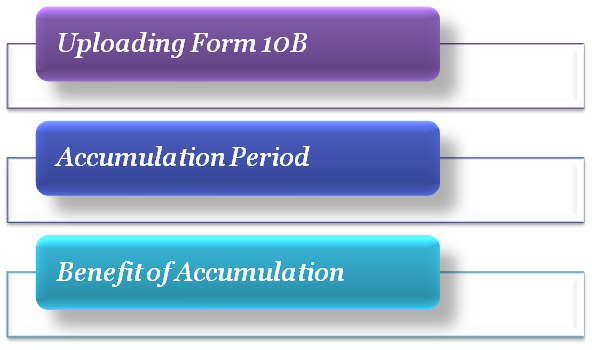

- A proclamation in Form 10B is required to be uploaded electronically within the allowed time period for providing the return within Section 139(1), informing about the amount being collected and the period of accumulation of income. In case Form 10B is not uploaded before the date provided then the benefits of accumulation can’t be availed and such income will be taxable.

- The period for accumulation of income should not exceed 5 years and the accumulated money should be invested or deposited in modes or forms specified by Section 11(5).

- From assessment year 2016-17, the benefit of accumulation cannot be availed if income return is not provided before due date for filing ITR as per Section 139(1).

Section 11(1) (d) – Corpus Donations are fully exempted

Corpus Funds or donations are fully exempted under Section 11 under NGO and there is no obligation to fulfill the specific criteria for application of at least 85% income for such donations.

What is Corpus Donations?

A corpus donation is the kind of donation that is made by a donor to any trust with a detailed direction that they are required to form part of the corpus of the registered trust. Only the donor has the right to give specific direction related to the donation.

Withdrawal of Exemption granted to Income accumulated under Section 11(2)

The income which is accumulated in accordance with the provision of Section 11(2) can be taxable in the following circumstances-

(a) It is applicable for purpose other than charitable as well religious trust;

(b)Income remains invested in a specified form or certain mode of deposit;

(c) It is not used for charitable or religious motive within the specified period;

(d) It is paid or credited to any trust or institution registered under Section 12AA or to any trust referred in clauses (iv), (v), (vi), and (via) of Section 10(23C).

Under any of the above-mentioned situation, the amount that is included is required to be deemed to the previous year income in which it is misapplied to be accumulated, following the expiry of the specified period.

Section 11(4) and Section 11(4A) – Charitable Trust Carrying on a Business

There is no bar on a charitable trust carrying on business activity. Any NGO can be established in relation to any property involving a business undertaking as well. The income from such business will also qualify for exception provided that the other conditions of section 11 under NGO and Section 12 are accomplished.

The income of such business will be determined in accordance with the provisions of the Act, which is Section 28 to Section 44 DB. If income from such business are fixed by the Assessing Officer is found to be in excess of the income shown in the accounts, then such excess should be considered to have been applied to non-charitable as well as non-religious purpose and that excess income will not qualify for exception. According to section 11(4) income of any business, which is held in trust for charitable purpose will be eligible for exemption under Section 11 under NGO.

Any income of a trust being profits of business, will not qualify for exemption under Section 11 under NGO, unless the business is incidental to the accomplishment of the objects of the trust and a separate books of account are maintained in respect of such business as per Section 11(4A).

Exemption related to Capital Gains Section 11(1A)]

The amount of exemptions under Section 11 under NGO in relation to capital gains arises on transfer of asset of charitable trusts will is provided when the capital gain asset is held under trust only for charitable or religious purpose if the following conditions-

- If the whole of the total consideration is utilized for attainment of a new capital gain asset, the entire capital gain will be exempted;

- If only a part of the total consideration is utilized, then the amount of capital gain will be exempted.

Conclusion

It is relevant to mention that the charitable trusts under Section 11 under NGO have an option to claim specific exemption under Section 11(1A) with relation to the capital gains. The other option includes general exemption under Section 11(1) (a) by applying at least 85% of the accumulated income for the charitable objectives.

Read our article:An Overview on Formation of a Trust under Indian Trusts Act