TDS under GST is different from TDS under the Income Tax. In additional words, separate TDS Payments, separate returns, and separate TDS Certificates are required in the case of Goods and services tax. Section 51 of the CGST Act, 2017, arranges down requirements in respect of TDS Payments under GST.

Who Deducts TDS Under GST?

Section 51 of the CGST Act, 2017, states that following are accountable to withhold TDS under GST:

- Department of Central Government or State Government;

- Local Authority;

- Government Agencies;

- Category of the person notified by the government on the recommendation of the GST Council.

The tax will be deducted at the rate 1% of the payment made to the supplier of taxable goods and services or both, where the total value of supply, under a contract, exceeds INR 2,50,000 not including the sum of central tax, State tax, Union territory tax, integrated tax and cess specified in the account.

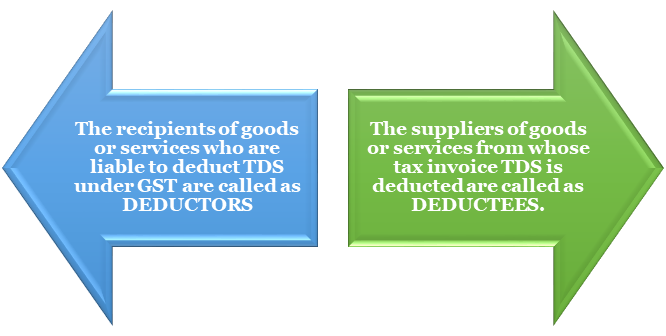

Who are Deductor and Deductee?

Applicability of TDS Under GST

Recipients of goods or services are also known as deductors who enter into a contract with a supplier for taxable products or services of a value exceeding INR 2,50,000 are mandatory to remove TDS from the tax invoice of suppliers. The TDS is charged on the taxable amount of goods or services which exclude the GST component on such taxable products or services. In other words, where the individual supplies may be less than INR 2,50,000 Lakhs, but where the chargeable value of goods and services exceeds INR 2,50,000, TDS would be deducted. Thus, certain conditions need to be fulfilled to deduct TDS from the tax invoice of the supplier of taxable goods and services.

Conditions for deduction of TDS

- The aggregate value of the taxable supply must exceed INR 2,50,000 under a single contract. CGST, SGST, IGST, UTGST, and CESS is not applicable under GST.

- In case the recipient entered into a bond with the supplier for both taxable supply as well as exempted supply, TDS would be deducted only if the value of the payable amount in the agreement exceeds INR 2.50 Lakhs. The taxable value doesn’t include Taxes or CESS appropriate under GST.

- When the site of the supplier and the place of supply is within the same state or same Union Territory, in case of intra-state supply, TDS @1% each under CGST and SGST or UTGST would be deducted, that is, a total of 2% (1%CGST and one %SGST or UTGST) where the inheritor or the deductor is registered in the same state or Union Territory without government.

- In cases where the site of the supplier is in State A, and the place of supply is in State or Union Territory B without legislation, it is an inter-state supply. TDS is deducted @ 2% will be deducted under IGST. Providing the recipient or the deductor is registered in the state or Union Territory B without legislation.

- When the location of the supplier is in State A, and the place of supply is in State or Union Territory B without legislation, it is inter-state supply. TDS will be deducted @ 2% and will be deducted under IGST. Providing the recipient or the deductor is registered in the state or Union Territory A without legislation.

- In case when the advance is paid to the supplier before or after 1st October 2018, for the supply of taxable goods or services, TDS will be deducted at the rate of 2%.

Read our article: How Form 15G and 15H Helps To Save TDS on Interest Income

When is TDS not being Deducted?

Following are the cases when there is no deduction in TDS:-

- Where the total value of the taxable supply is less than or equal to INR 2,50,000 under the contract.

- The Total agreement value exceeds INR 2,50,000 both for taxable as well as exempted supply. However, the cost of the payable amount under such a contract is less than or equal to INR 2,50,000.

- When the recipient receives exemption in services as defined by the GST Law.

- The recipient receives exemption in goods stated under the GST.

- The case when the supplier/deductee had issued an invoice for the sale of goods in which TDS has to be deducted under the VAT Law before 1st July 2017. However, payment for such a purchase is made on or after 1st July 2017 after coming of GST.

- When the site of the supplier and the place where the Supply has to be made is in a State or Union Territory that is different from the State or Union Territory, where the recipient/deductor has been registered.

- In case when the agreement includes transactions that are included in Schedule III of CGST/SGST Acts[1] irrespective of their price.

- When the payment has to be made to the supplier that is related to the tax invoice that has been issued before 1st October 2018.

- In cases where the advance amount was paid before 1st October 2018, and the tax invoice was issued before or after 1st October 2018. TDS will not be deducted to the extent of the advance payment made before 1st October 2018.

- When the tax required has to be paid on reverse charge based by the recipient.

- In case when the payment is made to the supplier.

- Where the payment is related to the CESS component.

TDS Rate Under GST

TDS under GST is deducted at the rate of 2% on the payment made to the supplier of taxable goods and services.

How deductee can claim the benefit of TDS under GST?

Any sum deducted as TDS and stated in GSTR 7 will routinely reflect in the electronic cash register of the deductee. The provider can take this amount as credit in his electronic cash record and use the same for imbursement of tax or any other liability.

Conclusion

If excess amount is removed and paid to the government, a refund can be demanded in the tax quantity if the government has a right. Though, if the deducted sum is already added to the electronic cash record of the seller, the sum so added cannot be refunded by the deductor. Deductee can claim a refund of tax subject to refund provisions of the act. The CorpBiz team shall be at your disposal if you need any assistance on TDS as well as GST. We shall be happy to serve you.

Read our article:TDS on Cash withdrawal and Refund of TDS excessively deposited: Latest Orders