NGOs, trusts, & charitable organizations need constant funding to operate seamlessly. Numeral tax exemptions are given both to the NGOs and the donor to promote donations & to encourage activities for good cause. Furthermore, to ensure access to such exemptions, these institutions must register u/s 80G & 12A of the IT Act. This registration was considered to be valid in perpetuity.

Some changes have been inculcated in this system via the Finance Bill 2020. While the exemptions are still accessible, re-registration u/s 80G & new registration u/s 12AB are now required. Furthermore, a new procedure has been introduced to claim CSR funding too.

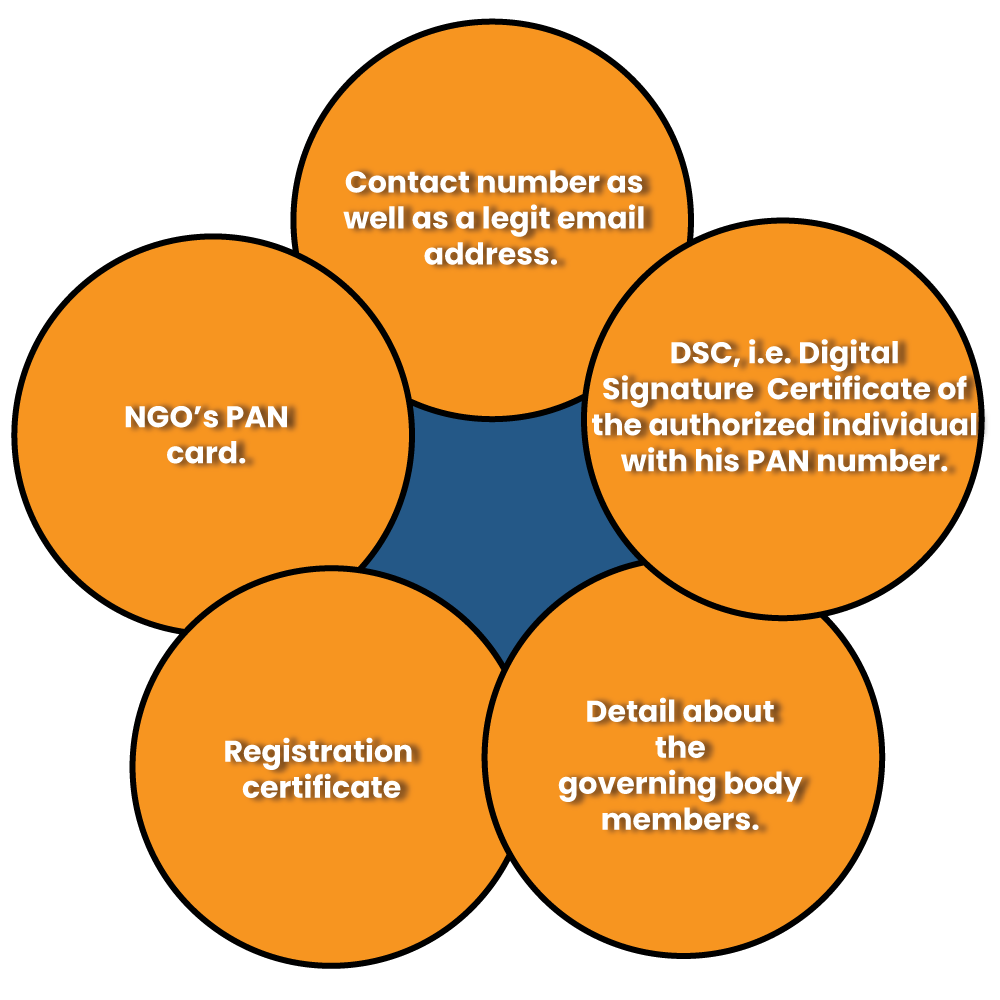

1. Form CSR-1 for CSR Funding

CSR, aka Corporate Social responsibility funding, is when the said entities can avail funding from organizations to execute their operation such as environmental protection or striving to introduce positive changes in society.

Moreover, w.e.f 1 April 2021, NGOs have to register via a Form CSR-1 in the MCA’s portal to be able to obtain such funds.

Eligibility about the filing of form CSR-1

a. Should be one of the following the institutions:

- A company set up u/s 8 of the Act, or a registered public trust or society u/s 12A & 80A of the IT Act, 1961.

- A Section 8 entity or a registered society or a trust established by the State or Central Government.

- Any company founded under a State legislature or an Act of Parliament

b. Should possess a legit registration u/s 80G and 12AA/12AB as of the date of application filing.

If you are establishing a new NGO, you have to register u/s 12AB & 80G of the Income Tax Act[1] before availing of CSR funding.

Mandatory Documentation for CSR filing

2. Re-registering Under Form 10A

Non-Government Organizations u/s 80G & 12A/12AA have the benefit of tax exemption. Moreover, to ensure access to such benefits, the NGOs are needed to re-register themselves with the IT department via a Form 10A.

Amendment to Section 80G

When a donor contributes to certain charitable avenues and relief funds, they can claim income deduction u/s 80G of the Act. This exemption is accessible only when the donation is routed to NGOs registered u/s 80G. Moreover, the Finance Bill 2020 has made some specific changes to the said section that will come to effect from 1 June 2021:

- The Principal Commissioner is to whom an entity must apply to be recognized u/s 80G. Further, they will possess the right to grant the registration.

- An obligation to render a donation’s statement received has been imposed on the entities, failure of which might lead to a penalty. Furthermore, in case of non-availability of the statement, the donor will dissolve the rights to claim the tax deduction.

- Furthermore, the notion of perpetual registration has been put out of the equation, and entities from now are required to seek renewal every five years under this section.

- A provisional registration possessing 3 years validity can be demanded by charitable avenues that haven’t commenced their charitable activities. Meaning- The charitable avenues are awarded registration on the basis of details submitted before the CIT (exemptions). The registration is accorded once the commissioner is satisfied with the legitimacy of such avenues. The Finance Bill proposes the provisional registration for the three years will be accorded to new entities which is yet to start their operation.

To get registered u/s 80G, form 10A as cited above must be submitted with the Principal Commissioner.

Read our article:Finance Act 2020 – Changes in GST

Documentation to be submitted for Form No. 10A

- Where an applicant is created, under an instrument, self-certified of such instrument creating the applicant;

- Where the applicant is created other than an instrument, self-certified copy of the document highlighting the establishment of the applicant;

- self-certified copy of the registration with ROFs or ROCs &Societies or Registrar of Public Trusts;

- self-certified copy of registration under FCRA, 2010, if the applicant holds a registration under such Act;

- Self-certified copy of prevailing order conferring approval under clause 23C of section 10;

- self-certified copy of the application rejection’s order for grant of approval u/c 23C of section 10, if any.

- Proof of business undertaking as per the provisions of subsection (4) of section 11.

- Note on the activities of the applicant.

- Self-certified copies of the annual accounts of preceding business as per the provisions of sub-section (4A) of section 11

3. New Registration u/s 12AB

All charitable organizations are now required to freshly register under Section 12AB. This is to get benefits provided under Sections 11 and 12 with effect from 1 April 2021.

- If you are an NGO earliar registered under the Section 12A/12AA, you required to register under Section 12AB within 3 months.

- Moreover, if you are an NGO not registered under Section 12A/12AA you required to apply for registration under the Section 12AB at least a month before started of the previous year relevant to your assessment year.

- Additionally, for new registrations, provisional registration for 3 years from assessment year from which registration is sought will be given.

All these amendments have provoked concern among NGOs as they theake compliance process more complex than ever. If you have an NGO, you need to understand the said changes inculcated by the Finance Bill to stay compliant.

Conclusion

NGOs, trusts, & charitable avenues have provisions related to tax exemptions in India. These are given because of the non-profit nature of their work. New registrations have been made compulsory for these institutions to claim these exemptions as of 1 April 2021. For any clarification on this topic, feel free to contact CorpBiz’s expert via commenting in the message box.

Read our article:How to approach NGO Registration in India? Forms & Features