The GST on transportation is applicable on goods along with the passengers pursuing their journey through the roadway, railway, airway, or waterway. It’s an undeniable fact that the transportation industry plays a massive part in the progress of any nation. Moreover, it’s not wrong to say that the growth of the transportation industry and the growth of a country walk hand in hand.

Various GST rates ranging from nil to 18% are applicable in the transport industry. Goods and service tax on transportation services have considerably not affected the ticket prices of traveling by Air, Road, or Rail. In addition to this, if goods and service tax on transport gets charged; Input Tax Credit is not applicable all the time. According to the report of the National Highways Authority of India, about 65% of freight/cargo along with 80% passenger traffic gets carried by the roads.

A few years back, the road transport industry has gained the spotlight with regard to the new GST, whose applicability is on freight charges including goods transport agencies, i.e., GTA. In this blog, we will spread rays of knowledge on the applicability of GST on the transportation of goods as well as passengers.

GST On Transportation of Goods

The GST on transportation of goods starts from nil at an applicable rate. Here, the goods and service tax gets incurred by the transportation of goods moved out by rail, road, air as well as inland waterways. The list of goods that are exempt from goods and service tax on transport are-

- Military or defense equipment that gets transported

- Milk, pulses, flour, rice, salt and different food grains

- Relief material allotted to the victims of natural or man-made calamities, accidents, and mishaps, etc

- Magazines and newspapers registered with the newspaper Registrar

- Organic manure as well as agricultural produce

- If the total amount charged for the transport of goods is below Rs 1500

Applicability of Exemption or Nil GST on Transport is in the cases given below-

Taxation rates for GST on Transportation of Goods by a Goods Transport Agency (GTA)

- If input tax credit not availed, 5% GST will be applicable on transport.

- If input tax credit gets availed, 12% GST will be applicable.

- On rental services of freight aircraft either with or without an operator, the applicability of GST is 18%.

- On rental services vehicles running on the road like trucks without or without an operator, applicability of GST rate is 18%.

- On rental services of water vessels comprising freight vessels either with or without an operator, applicability of GST rate is 18%.

Note– These rates are not fixed, and they keep varying from time to time as per the GST amendments.

GST on Transportation of Passengers by Rail

Applicability of GST on rail tickets for passengers is at the rates given below-

- Nil goods and service tax is applicable on metro tokens/tickets.

- Nil GST is applicable on sleeper tickets as well as tickets for general class.

- 18% goods and service tax is applicable on AC and first-class tickets of train.

*The above list is open to periodic change.

GST on Transportation of Passengers by Air

Applicability of GST on air tickets for passengers is at the rates given below-

- 5% goods and service tax is applicable on air tickets for economy class

- 5% goods and service tax is applicable on tickets of chartered flights for the pilgrimage visiting purpose

- 12% GST is applicable on the air tickets of business class

- 18% goods and service tax is applicable on rental services of aircraft either with or without an operator and is also applicable on rental services of chartered flights

*This list is subject to changes by the governing authorities.

Read our article: A Complete Outlook on Job Work under GST Regime

Rules Concerning ITC Claiming

- In the case of business class, airlines can claim the input tax credit for spare parts, food items, along with different types of inputs except for fuel.

- In the case of economy class passengers, airlines can make claims for the input tax credit on input services.

- Most importantly, you can also claim the goods and service tax on air tickets as ITC for business purposes. The condition is that your purpose of traveling should be related to business.

GST on Transportation of Passengers by Road

- The main GST rates that are applicable to goods and service tax on road transport of passengers-

- Nil GST is applicable to passengers using public transport to travel via road

- Applicability of Nil GST on road transport of passengers by different modes of public vehicles like auto rickshaw/metered taxi and e-rickshaw

- Nil GST is applicable on transport via non-A/C contract carriage or stagecoach

- 5% goods and service tax is applicable to transport by radio taxi and also on similar kind of services

- On transport by A/C contract carriage or stagecoach, 5% GST will be applicable and no applicability of ITC

- Applicability of 18% goods and service tax on rental services offered by road vehicles like buses, cars, coaches either with or without operator

*These key rates are subject to changes from time to time.

Peek at the Concept of GTA (Goods Transportation Agency)

Goods Transportation Agency or GTA means any person or an entity that renders services such as transportation of goods via road and issues consignment note as well. Going through the GST Act[1], we learned that it’s not necessary that GTA always refers to an individual or business that is performing the task of hiring out vehicles for goods transportation. Therefore, it is businesses or individuals that are responsible for issuing consignment note and get qualified as Goods Transportation Agency.

Services Provided by a Goods Transportation Agency

The various services that GTA provides are-

- Actual transportation of goods

- Packing/unpacking

- Trans-shipment

- Loading as well as unloading

- Temporary warehousing facility

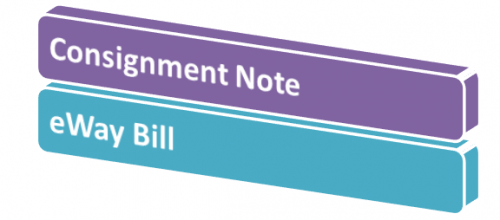

Essential Documents involved in the Transportation of Goods

- Consignment Note

Goods transportation agency issues a document in place of a receipt of goods for the purpose of transporting the goods via roads into a carriage. This document is known as a consignment note. After a consignment note gets issued, the responsibility of goods lies in the hands of transporter till the time consignment gets delivered to the consignee. There is no need to pay additional charges for generating a consignment note which the transporter has created.

- eWay Bill

Before the transportation of goods, eWay bill gets generated. eWay bill is a mandatory document for all businesses and individuals registered under GST involved in the transportation of goods from one site to another.

eWay bill includes-

- Name of Consignee

- Name of Consignor

- Details about vehicles used in transporting the goods

- GST paid on transported goods

Take Away

The GST law is carrying forward the provisions that were a part of the previous tax regime. However, the new law came with something different and identifies that most of the time, people in the unorganized sector renders the services of transportation of goods. Goods and service tax is applicable to transportation services provided by a goods transportation agency. Furthermore, businesses or individuals must issue consignment note in order to get qualified as GTA.

Read our article:GST on Food Services and Food Items: All that you need to Know