Alternative Investment funds (AIF) in India are witnessing exponential growth since their inception in 2012. The number of investors in this sector is increasing every passing day. In this article, we would unfold some facts regarding the growth of Alternative Investment funds from India’s perspective.

An Overview of the Growth of Alternative Investment Funds in Recent Years

In the view of the Global Limited Partner Survey held in 2017, our country secured top in ranking and became the most preferred platform for alternative investment. This has triggered the growth of new capital and broadened the scope of consumer protection.

Where the stock market has witnessed a significant decrease in investment with the fall of benchmark Sensex, Alternative investment Funds are making a great buzz in our country. Additionaly, unlike mutual funds, AIF offers inculcation of hedging strategies.

Owing to these reasons, Alternative Investment funds are likely to strengthen their position in the upcoming years. As per SEBI, the registered funds are consistently thriving for AIF every passing year and have reached 366 in 2018. Till Sep 2018, about 470+ AIF have obtained funds that have resulted in enhancing the efficacy of this volatile secondary market. This marks a considerable rise in the Indian economy at a faster pace.

Outlook on Alternate Investments Funds and its Various Categories

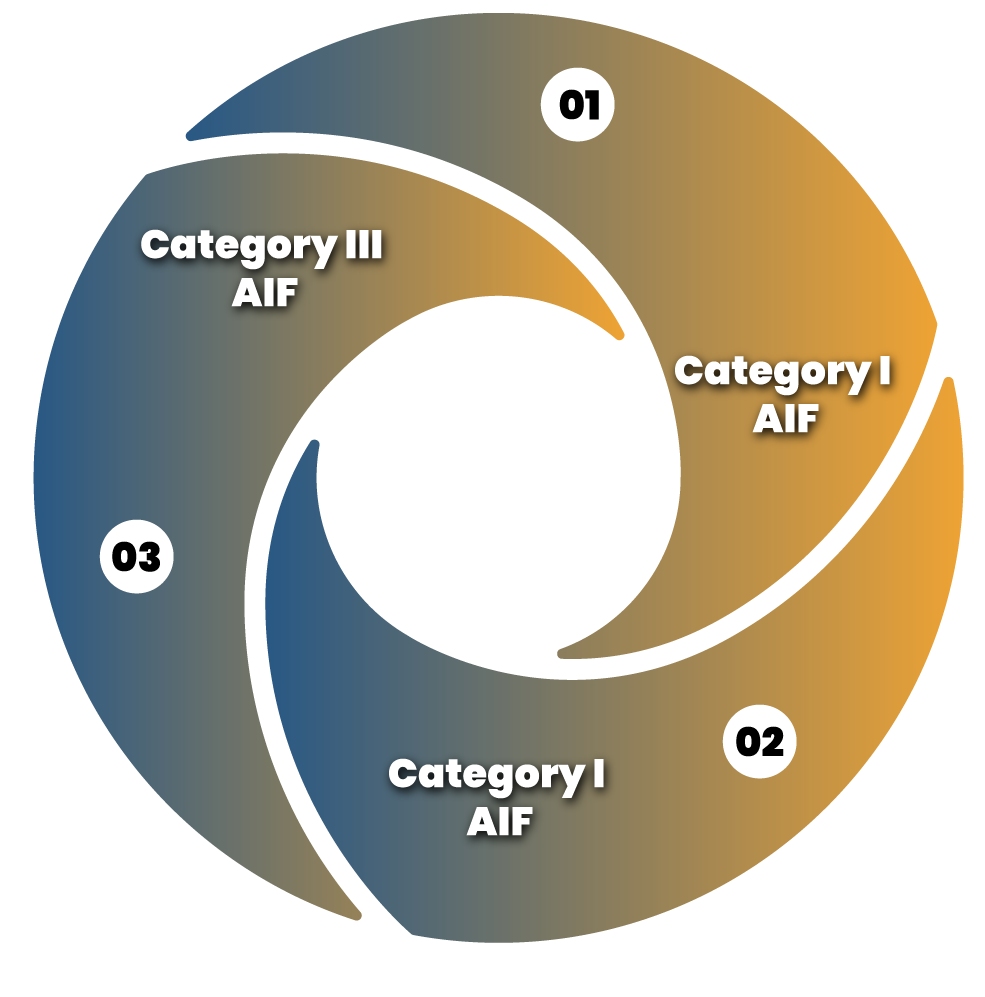

Unlike traditional investment methods, the Alternative Investment funds (AIF) resides outside the framework of SEBI’s regulation meant for investment institutions. They bear distinctive identities when compared with stocks, bonds, etc. Also, they are perceived as private investment opportunities in general. These funds are categorized into the following classes, which are as follows:-

Category I AIF

It encloses a class of the funds subjected to the investment in socially or economically ventures such as Social Venture Funds[1], Venture Capital Funds, SME funds, and Infrastructure Funds.

Category II AIF

It comprises funds that are not part of Category I or Category III AIF. This investment is done depending on the investment mandate, such as Debt funds and private equity funds.

Category III AIF

It consolidates all the funds that have intricate and flexible investment strategies to ensure decent return, either by investment in Hedge funds or by the use of leverage.

Read our article:CBDT Amends Rule 12CB related to Investment Funds under Section- 115UB(7)

Reasons Pertaining to the Sustainable Growth of Alternative Investment in India

There are wide arrays of factors that affect the growth of AIFs in our country, some of them are mentioned below:-

- The growing real estate sector has led to a whopping hike in the AIFs in our country. Also, in the year 2017, this sector was deemed to be second most active sector in India. The development of NIIF (National Infrastructure Investment Fund) of Rs 20,000 Crores by the government of India is one of the prominent factors due to the boost of AIFs.

- Investors are more inclined towards Category III as they are allowed to invest in commodity derivatives until 10% of the investible funds. Not only this, but they are also permitted for taking advantage up to two times.

- Since Nov 2015, the Reserve Bank of India has also rolled out a notification for the AIFs foreign investment under the automatic route. There are two things: First, there will be FDI limitation applicable for AFIs if the individual who controls the fund is from the Indian Territory. Second, if most of the AIF contains the overseas capital, it would be deemed local funds.

- Deploying tax pass-through structure for the Category I and II funds. This way, investors will be liable to address tax liabilities under these categories and can easily avoid the trouble related to double taxation.

However, there is still room for improvement to ensure long term growth stability.

Viable Strategies to Ensure Substantial in Alternative Investment Funds in India

Growth in AIFs also acts as a key performance indicator for the Indian Economy. Therefore, it is compulsory to mitigate the loopholes by selecting suitable reforms so that there can be a legitimate change in the AIFs structure of India. The following section exhibits the suitable measures that must be considered to ensure steady cash investment:-

Garnering Local Institutional Investors for the Investment in AIFs

Currently, our country is more dependent on the overseas market for funds. If there was an increase in local institutional investors, you will witness positive outcomes in the growth of AIFs in India.

Essential Amendments to the Goods and Service Tax Framework

The current GST framework must be incorporated with 2 changes, which are as follows:-

- For all investors who put up their funds in PE and VC funds, 5% of tax ought to be levied on services provided to these funds.

- GST should be applied on overseas investments that surpassed 50% in AIFs as all the services that the Alternative Investment funds receive must be deemed as an export of services.

Growth-Oriented Taxation Reforms

Existing tax reforms for AIF sectors isn’t favourable as it should be. Below we have mentioned some essential measures to cater to such an issue.

- For Category III AIFs, there should be a Pass-through structure.

- The transaction-related unlisted securities and profits should not be perceived as business gains. Rather it must be treated as capital gains. Besides, the expenses related to AIF management should be treated as improvement costs.

- If the AIF ends up unprofitable, it must be set-off against the income of the investor rather than the business profits of AIFs.

- Deployment of a Unit-based Taxation Approach must be done prior to the advent of AIFs under the stock exchange platform, such as mutual funds. The tax shall not be imposed on the investors of registered AIFs:

- Distribution tax should be applied on dividends as well as interest.

- Capital gains tax should be brought into existence along with unit transfer for short and long-term capital gain.

- Tax exemption should be accessible to an overseas investor for the generated income via an AIF in as IFSC.

Alternative for Leverage on Category III Funds of Funds (FOF)

The FOF market in India is an initial stage of development when contrasted with the global scenario. Henceforth, it is imperative to render an alternative for taking leverage at the Fund of Fund or individual portfolio level.

Compulsory Disclosure of Fund-based Information

Imperative details regarding the fund performance must be shared with the investor. Besides, there must be an establishment of an Investment Advisory Committee that shall play an important role in managing all the fund’s related conflicts in a better way.

The aforesaid essential reforms will surely ensure the sustainable and long term growth of AIFs in India. Although the Alternative Investment Funds are still in the emerging stage, with such reforms in place, they will surely arrive at a good position in the coming years.

Conclusion

The growth in AIFs will surely have a sustainable future in the coming years. You will witness the increase in the investor’s numbers, which in turn leads to stimulate the growth of the Indian Economy. A great transformation is on its way that will ensure cut development in the AIF sector soon.

Read our article:What are Alternative Investment Funds and why they are becoming increasingly popular across the Globe?