Due to the possibility of taxable supplies being broadened under GST, Exemptions under GST have clearly been defined by the law. They understand that the tax also involves knowing whether the item is exempted or not under the rules of GST. Not just expressing the Exemption list, but also understanding the suggestion of item being exempted is essential as specific circumstances are attached to it like reversing the Input Tax Credit. What can be Nil rated today may also become charge to a higher tax rate in the future circumstances. Henceforth, demarking the various terms such as Nil Rated, Exempt, Zero-rated, and Non-GST supplies under Goods and services tax is essential.

What are the Exemptions under GST?

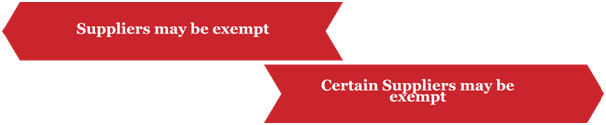

Organizing Exemptions under GST are as follows:-

Suppliers may be exempt

Exemption to any person making supplies which means suppliers of goods, regardless of the nature of external supply of goods.

Example of such supply are Services offered by Securities and Exchange Board of India, Services by Charitable entities.

Certain Suppliers may be exempt

Certain goods are exempted under GST due to the nature and the type of the supplier. All supplies that are informed will be eligible for the exemptions under GST. Here, irrespective of who the supplier is, the exception is allowed. It is not very much relevant. Example of certain supplies may be exempted under GST are Services by offering sponsorship of sporting events, Services by way of public conveniences.

Read our article:How to apply for GST registration certificate online?

Types of Exemptions under GST

The different types of Exemptions under GST are-

Absolute Exemption

Under this type of exemptions of GST, the supply of specific types of goods would be exempted from GST without seeing the details of the supplier or receiver or whether the good is supplied within or outside the State.

Example- Transmission or distribution of electricity by an electricity transmission or distribution utility, Services by Reserve Bank of India.

Conditional Exemption

Under this type of exemptions of GST, the supply of specific variety of goods will be exempted under GST subject to specific terms and conditions which have been laid under the GST Act.

Example- Services offered by a hotel, for residential or lodging purposes, having declared tariff less than INR 1000 per day.

Conditional or partial exemption

Intra-State supplies of goods and services received from an unregistered person by a registered person are exempt from payment of tax under reverse charge provided the aggregate value of such amounts established by a listed person or any of the providers does not exceed INR 5000 in a day.

What do you mean by Exempt supply under GST?

Exempt supply under GST means that suppliers which not fascinate goods and service tax. In these supplies, no GST is charged in this case. Input tax credit paid on the supplies that will not be used for utilization.

These are the following types of supply which are considered as an exempt supply: –

- Supplies that are chargeable to nil rate tax.

- Supplies that are partially and wholly exempt from the charge of GST by the notifications which amended section 11 of CGST and section 6 IGST.

- Supplies that come under the sec 2(78) of the act. Which covers the amounts which are not taxable under the law like alcoholic liquor for human consumption.

Exemptions under GST Law and its effect on another GST Law

Note that the exemption allowed under the CGST Act cannot be deemed to be applicable under the IGST Act. In other words, GST permitted exclusion in case of inter-State business transactions is not the same as the Exemptions under GST available in case of Intra-State transactions.

| Exemption under CGST Act | It was deemed to be exempt under the SGST / UTGST Act.No auto-application of exemption under the IGST Act |

| Exemption under IGST Act | No auto-application of exemption under the CGST Act |

What is a non-taxable supply under GST?

Non-taxable supply under GST means a procurement of goods or services or both, which is not levied upon to tax under the CGST Act or the IGST Act[1].

This definition covers only those supplies that are excluded from the scope of taxation under GST – that is, alcoholic liquor for human consumption, articles listed in section 9(2), or in schedule III.

It should also be noted that the next items are not out of the possibility of GST, which means that the GST Rate has not yet been announced or notified for them.

- Petroleum crude

- High-speed diesel

- Motor spirit (commonly known as petrol)

- Natural gas and

- Aviation turbine fuel

Exemptions under GST on Services

Like precise goods, specific services can also be exempted under GST. There are basically 3types of supply of services that would qualify for exemption under GST. These include the following –

- Amounts that have a 0% tax rate on supplies;

- Supplies does not attract CGST or IGST due to the provisions stated in any notification or statement which Compensated either Section 6 of IGST Act or Section 11 of CGST Act;

- Supplies that are not taxable and are defined under Section 2(78) of the GST Act;

- Since these types of supplies are exempted under GST, any Input Tax Credit, which applies to these supplies would not be available to utilize or set off any GST liability.

Exemptions under GST for businesses

Small and medium scale businesses can enjoy the benefit of GST exemptions if their aggregate turnover is up to a specified limit prescribed under the GST law. When the GST Act came into existence, the limit set was 20 lakhs for the individual as well as businesses and 10 lakhs for hilly and the North-eastern States of India. Though, in the 32nd GST Council Meeting, which was held in January 2019, the limits have been changed.

The limits are as follows –

- Businesses and individuals who are providing goods can claim GST exemption if their collective turnover is less than 40 lakhs in a financial year;

- In case of hilly and north-eastern states of India, the limit has been set to 20 lakh;

- For business and individual involved in the supply of services, the limit for claiming GST exemption is 20 lakh;

- In the case of hilly and north-east State, if the cumulative turnover is up to 10 lakhs, business and individual supplying the services can claim GST exemption.

Hilly and north-east States includes Jammu, and Kashmir, Himachal Pradesh, Uttarakhand, Tripura, Nagaland, Arunachal Pradesh, Meghalaya, Mizoram, Assam, Manipur and Sikkim. Total turnover, as per the GST Act, would include the total value of all taxable supplies, inter-state supplies, exempt supplies, and the goods and services which have been exported.

Conclusion

Exempt supply under GST means that suppliers which not fascinate goods and service tax. In these supplies, no GST is charged in this case. Input tax credit paid on the supplies that will not be used for utilization. Our Corpbiz group shall be at your disposal if you seek expert advice on any aspect related with GST along with complete compliance. We will help you ensure full compliance concerning all the requirements based on your anticipated activities, ensuring the productive and well-timed completion of your expectation.

Read our article:Financial and its related services Under GST