As per Section 46 of CGST Act, 2017 read with Rule 68 CGST Rules 2017, a notice in FORM GSTR-3A is issued to any registered person who fails to file annual return (defaulter) requiring them to provide such return within 15 days. Further, Section 62 offer assessment for non-filing of GST return of registered persons who fails to provide annual return under Section 39 or Section 45 even after notice under Section 46.

Guidelines Prescribed for Non-Filing of GST Return

Following are the guidelines prescribed to ensure Non-Filing of GST Return-

1.A system generated message will be sent three days before due date for filing of the return for the taxation period.

2. A system generated message and mail will be sent to the defaulter immediately after the due date for filing of the return for the taxation period.

3. A Notice in Form GSTR 3A will be issued electronically Five days after furnishing the return to the registered person asking him to provide return within 15 days.

After 15 days of Notice in GSTR 3A, the proper authority can proceed to assess the tax liability taking into account all the relevant information and will issue order in Form GST ASMT-13. The authority is required to upload the summary in Form GST DSC-07.

Information required by the Authority for purpose of Assessment-

- Details of outward supply available in Form GSTR 1;

- Details of supply available under Form GSTR 2A;

- Details available e-way bills.

4.In case the defaulter provides a valid return within 30 days of assessment order in Form GST ASMT-13, the order shall be withdrawn.

If the return is still unfurnished within statutory period of thirty days, then proceedings under Section 78 of CGST Act[1] will initiated.

Read our article:GST Return Filing Procedure – Types of GST Returns, Due Date and Penalty

Late Filing Penalty for Non-Filing of GST Return

The GST late filing penalties are as follows-

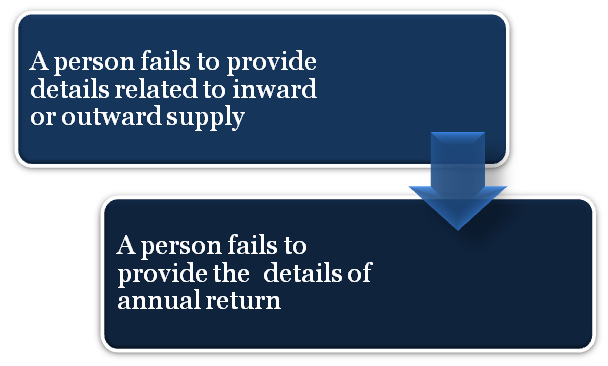

- If a person fails to provide details

The penalty for late filing is INR 100 for each day till the details get furnished in case the person fails to provide details related to inward or outward supply, monthly or annual return by the due date. In case the person is unable to provide the relevant details in the prescribed time then a fine will be applicable with a maximum of Rs. 5000.

- If a person fails to provide the annual return

In circumstances where a person is unable to provide the details associated with annual returns, he would be liable to pay the penalty for late filing for the same. Herewith, the penalty would be adjudged at Rs.100 per day in extension till the required details are furnished by the applicant to the concerned authority. If the applicant does not provide details in the specified time then fine applicable is maximum of 1/4th percent of the person’s income in the state where he is registered.

Interest rate for Non-Filing of GST Return

The interest rate on the applicable offences is yet to be notified, the GST late payment penalty has been specified as follows:

- If a person liable to pay tax fails the interest on the due tax will be calculated from the first day on which the tax was to be paid.

- A person makes an excessive claim of ITC or excess reduction in output tax liability then the interest on excessive ITC claim will be calculated.

Cancellation of Registration

The conditions under which a GST registration can be cancelled are-

- A regular dealer has not provided returns for a continuous 6 months period.

- A composition dealer has not provided returns for 3 quarters.

- A person who has taken voluntary registration has not begun business within 6 months from the date of registration.

- Registration has been obtained by willful misstatement fraud, or suppression of facts.

Confiscation of Goods or Conveyance

The penalty specified for confiscation of goods or conveyance and imposition of INR 10,000 fine or an amount equal to the evaded tax. The penalty is imposed for the following offenses-

- If a person does not account for the goods on which he is liable to pay tax.

- If a person supplies or receives goods in violation of any provision with the intent to evade tax.

- If a person supplies any goods liable to tax without registration.

- If a person uses transportation for taxable goods in breach of any rule or provision.

Imprisonment and Fine for Non-filing of GST Return

The circumstances under which imprisonment or fine applicable are-

- Preventing or obstructing any officer in discharge of his duties, tampering or destroying any evidence or documents – 6 months imprisonment with fine;

- Supplying false information or failure to supply information required by the law – 6 months imprisonment with fine;

- Input Tax Credit wrongly availed on amount exceeding INR 50 Lakhs but less than INR 1 Crore or tax evasion – Imprisonment which can extend to 1 year with fine;

- Input Tax Credit wrongly availed on amount exceeding INR 1 Crore but less than INR 2.5 Crores – Non-bailable imprisonment which can extend up to 3 years with fine;

- Input Tax Credit wrongly availed on amount exceeding INR 2.5 Crores – Non-bailable imprisonment which can extend to 5 years with fine.

Other Penalties imposed for Non-filing of GST Return

Offences on which penalty will be imposed for Non-filing of GST Return are as follows-

1.Penalty imposed if a person commend the following specified offences – INR 10,000 or an amount equal to the tax evaded

- Issues an invoice without supply of the related services and goods;

- Collection of taxes, in failure to pay the same to the authority beyond a period of 3 months from the date on which the payment reflected as dues;

- An e-commerce operator fails to collect tax or fails to pay the tax to the Government;

- Takes ITC without actual receipt of goods and services either fully or partially;

- Attain refund of tax by fraud;

- Misrepresent or substitute financial records or create fake accounts and documents or deliver false return;

- Fails to obtain registration;

- Provides false information with regard to registration;

- Transfer taxable goods without any documents;

- Failure in maintaining books of accounts;

- Restrain turnover leading to tax evasion;

- Issues an invoice or document by using the identity of another person.

2. Penalty imposed if any person assist & support any offences listed above – Fine can be extended up to INR 25,000;

3. Penalty imposed if a person who commits any offence for which penalty is not provided under the law – Fine can be extended up to INR 25,000.

Conclusion

All registered business has to file monthly, quarterly or annual GST Returns based on the type of business. A return is a document which contains the details of income which a taxpayer is required to file with the tax administrative authorities of India. In case of non-filing of GST Return, late fine with interest is imposed on them. To know more about GST Return Filing process contact CorpBiz.

Read our article:CBIC: Extension of deadline for GST Return Filing FY 2019-20