After getting over with the complete company registration procedure, it has been observed that employers are the main asset of any company. Whenever a firm decided to wrap up one of their main offices or units for any reason, they need to offer compensation to the top management. Section 202 explains the same concept in the Company Act 2013[1]. In this blog, we will go through a detail of Compensation to “Director for Loss of Office.” This particular term mention under section 202 of the Company Act 2013.

The notion of Compensation to Director for Loss of Office

A company might give payment to MD or Director (full-time) or manager by way of compensation for office-related loss, or for fulfilling the purpose of retirement or in connection to both. No payment will be made as per sub-section (1) in the following circumstances, viz:—

- In case of resignation of director due to reconstruction of the company, or its collaboration with other corporate or bodies corporate, is appointed for the post of managing or Director, manager of the reconstructed company or the corporate setup via amalgamation;

- where the Director opted for the resignation from his office otherwise than on its amalgamation or the reconstruction of the company as aforesaid;

- where the office is already in search of Director due to vacant position under sub-section (1) of section 167;

- where the Tribunal has wound up the company’s operation, provided due to negligence of the Director;

- where the Director defrauded the company or hampered the operation due to negligence or gross mismanagement.

- where the Director has involved in the action that triggers the chance of the termination of his office.

Any payment made to an MD or Director as per sub-section

- shall not surpass the remuneration’s limit, which he could have earned if he were in the office for its remaining tenure or three years, whichever is applicable, estimated by considering the average remuneration he/she earned during three years, leading to the date when office’s operation was put on hold or where he involved with the office for less than three years, during such period:

- Provided that the payment of such nature is made w.r.t commencement of the company’s winding up within the time span of one year of the date on which he halts the office operation if the asset after deducting the expenses is not enough to deal with repayment of shareholders.

- Nothing in this section is projected to hinder the payment provision of managing or whole-time Director, or manager

Read our article:Circulation of member resolution: Everything you need to know

Specifications for Compensation to Director for Loss of Office

Compensation may be paid for the following reasons:-

- For the loss of office; or

- As consideration for retirement from office

- In connection with such loss or retirement

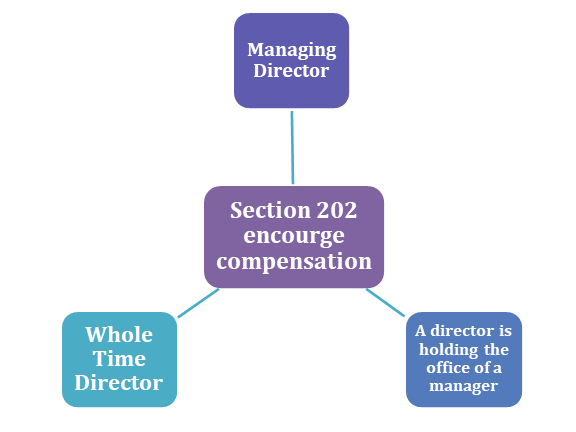

Compensation to whom

- Managing Director

- Whole Time Director

- A director is holding the office of a manager.

Permissible period

- Unexpired period of Directorship.

- Three years.

Basis: Average remuneration Earned

- Period for which Director held the office.

- Three years immediately preceding the date of the cessation of office.

In relation to subsections discussed previously, Rule 17 of the Companies (Meetings of Boards and its Powers) supplements this provision. No director of a company can reap monetary benefit via compensation w.r.t event included in sub-section (1) of section 191 unless the company’s member comes across following particulars, and then they authenticate the payment amount in the general meeting.

- Director name

- The exact figure of the payable amount

- illustration of the circumstances in which compensation becomes payable

- Board meeting Date w.r.t such payment

- illustration on how the amount is determined

- Fact or reasons that justify the payment

- Payment mode

- Payment source

- Relevant particulars.

Any expenses bear by the company in the form of compensation to counter office-related loss or as a consideration for retirement to an MD, or whole-time Director of the company shall not surpass the limit mentioned under section 202. No payment shall be made to Directors or MD of the company as a compensation for the office loss or retirement consideration from the office or in connection with such loss or retirement if the following reasons gets satisfied.

Those are as follows:-

- The company involved in paying issues regarding public deposits or payment of interest thereon;

- The company is still in the defaulter list of entities engaged in mismanagement w.r.t payment of interest or redemption of debentures.

- The company is acting as a defaulter w.r.t liability, towards public financial institutions, banks, and financial institutions.

- The company has income tax liabilities that still need to be addressed. Plus, expenses like VAT, excise duty, service tax are still waiting in a queue that the company failed to address on time.

- The company failed to make a payment regarding the statutory dues of employees.

- The company failed to pay dividends on preference shares or unable to redeemed preference shares on the due date.

- The company is accountable to pay expenses w.r.t compensation to the MD of the company or Directors for the loss of office.

- These payments seek approval of general meetings, or else it will bear no value.

- Any amount reaped by the Director before approval or received in the violation of this section shall not be deemed a company’s transaction.

If a company’s Director violates the provision through any means, the predetermined fine will be imposed on such activities. The bandwidth of this fine ranges from Rs 25,000 to Rs 10,00,00.

Conclusion

Section 202 is an employee-oriented provision that protects the right of top management w.r.t claim for compensation. The unexpected shutdown of the office could lead to loss of remuneration, and that where section 202 comes into the picture. It led the Directors or MD of the company to demand compensation for their remaining tenure. If you need some additional help regarding the concept of Compensation to the Director for Loss of Office, feel to connect with us.

Read our article: Guide: Freezing of the company’s assets on investigation and inquiry