Consumption of goods and services is intended by GST based taxes. Starting from manufacture up to final consumption with credit of taxes paid at previous stages available as set off, it is projected to be levied at all the right phases. In an outer layer, the burden of tax is to be tolerated by the final consumer, and in which only value addition will be taxed. Deprived of GST registration, a person can neither assert any input tax credit of tax paid by him nor save/collect tax from his customers.

Well, are you aware that 18% GST is applicable on Works Contract for National Centre for Biological Sciences (NCBS[1]) held by Authority of Advance Ruling (AAR)? In addition, do you know that all Supply Facilities of Food and Drinks to Educational Institutions are exempted from GST? Yes. This blog will articulate the recently ruled observation made by Authority of Advance Ruling (AAR), Karnataka upon the GST applicability on the said purposes.

GST Applicability on Works Contract for National Centre for Biological Sciences: 18%

Authority Held

- In consonance with the GST applicability, the works contract service delivered to the (NCBS) National Centre for Biological Science is liable to be taxed 9% under (CGST) Central Goods and Service Tax and 9% under Karnataka Goods and Service Tax (KGST). It has been ruled by The Authority of Advance Ruling (AAR), Karnataka.

Facts and Contentions

- M/s Homebale Construction and Estates Private Ltd, the Applicant in the case, is a Private Limited Company incorporated under the Companies Act, 1956. For the creation of Hostel building at NCBS Campus in Bangalore, they have arrived into a works contract agreement with NCBS-National Centre for Biological Sciences.

- According to the parameters assigned for GST applicability via ‘Notification No 24/2017 Central Tax (Rate) dated 21-09-2017’, the applicant has sought after advance ruling on the subject issue whether an applicant should charge GST @12% for service delivered to National Centre for Biological Sciences or not.

- It is a crucial point to be noted, that this institute is not recognized to carry out a function entrusted by the Government. Therefore, the authority has pointed and remarked upon it saying that the NCR is not protected under the definition of a “Government Entity,” and cannot be articulated upon it.

Read our article: A Complete Outlook on Job Work under GST Regime

Remarks from Bench Bar

- After due deliberations, discussions and fair trials, it was held by M.P. Ravi Prasad and Mashud Ur Rehman Faruqui that GST applicability for the work contract service delivered by the applicant to the National Centre for Biological Science (NCBS) is liable to be taxed at the rate of 9% under Central Goods and Service Tax (CGST), and 9% under Karnataka Goods and Service Tax (KGST).

- The authority for this ruling consisted of members M.P. Ravi Prasad and Mashud Ur Rehman Faruqui. It has been pronounced that “NCBS is neither recognized by the government nor is set up by State Government or an Act of Parliament. As well, M.P. Ravi Prasad opines that Government does not have more than 90% control over it, because the council which manages this institute has only four members appointed by the Government.

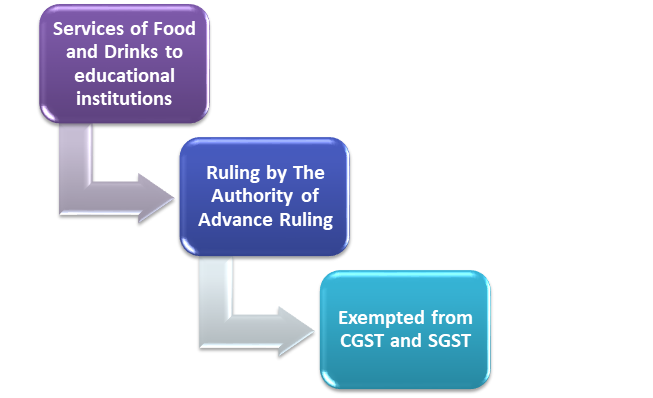

GST Applicability on Supply services of Food and Drinks to Educational Institutions: Held Exempted

Authority Held

- It was held that the supply facilities of Food and Drinks to educational institutions are exempted from State Goods and Service Tax (SGST) and Central Goods and Service Tax (CGST). It was ruled by the Authority of Advance Ruling (AAR), Karnataka.

Facts and Contentions

- According to the GST applicability pronouncements “SI.No.66 of the Notification No.12/2017 Central Tax (Rate) dated 28th June 2017”, M/s Mahalakshmi Mahila Sangha which is the applicant in the case was involved in providing catering services to educational institutions supported by State/ Central Union territories which are under exempted services.

- All over again, with the virtue of GST applicability under Serial No. 66 of the Notification No. 12/2017-Central Tax (Rate), the applicant sought improved/advanced ruling on the issue of whether activities of delivering catering services to educational institutions under exempted service.

- It was also contended that TDS under GST is applicable only for taxable supply contracts according to the Circular 65/39/2018. Therefore, the applicant is meant to be exempted as the service provider. It was also mentioned that TDS is not applicable to its services (HSN Code 9992).

Remarks from Bench Bar

- M.P. Ravi Prasad and Mashud Ur Rehman Faruqui were the Authorities consisting of members who ruled that, the supply of services made by the applicant in the form of supply of food and drinks to the educational institutions is covered under entry no.66 of Notification (12/2017) Ng. FD 48 CSL 2017 and entry no. 66 of Notification No. 12/2017- Central Tax (Rate). After due deliberations, these services are hence exempted from CGST and SGST.

- It was also noted by the AAR, that under section 51 of the CGST Act and section 51 of KGST Act, “the amount received for such exempted service as sheltered under para 1 above is not accountable for tax deduction at source”

Conclusion

The greater test may essentially be around GST applicability for the institutions. Our Corpbiz group will be at your disposal if you want expert advice on any aspect of Charitable Trust issues. We will help you to ensure complete compliances concerning all the issues related to GST applicability-based as per your desired activities, ensuring the fruitful and well-timed completion of your work.

Read our article:Elucidation on GST Refund Issues – Recent Updates