The Income Tax Appellate Authority or ITAT has ruled in favour of Yum Restaurants situated in Asia, which operates for brands such as KFC, Pizza Hut, and Taco Bell in India, stating that the amenities provided by the vice president are not taxable of its Indian Counterpart.

Decision of ITAT

The case is related to the agreement and contract between the Yum Restaurants situated in Asia, the assessee and Indian counterpart, where Vinod Mehboobani was deputed to India as the vice president for Asia. The assessing officer held that the VP was providing technical services on behalf of the assessee company. Henceforth the salary settlement was ‘Fee for Technical Services’ (FTS) actually.

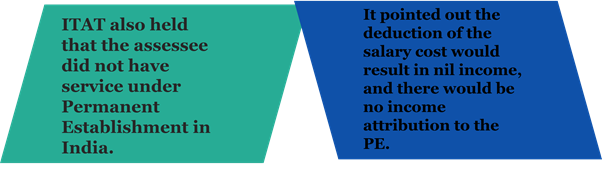

Though, the Income Tax Appellate Tribunal (ITAT), Delhi, held that the Vice President took part in the everyday operative functions of the Indian Branch by attending board meetings, signing the financial statements, and under the direct governance of Yum Restaurants India. Also, he did not ‘make available’ any technology, knowledge, or skill in its Indian Counterpart.

Facts and Contention

During the period under consideration, the salary was paid by the assessee in Singapore and was reimbursed by the Indian Branch on a cost-to-cost root. Consequently, the ITAT held that the Vice President was an employee of the Indian Branch and not for the assessee company.

Also, the Vice President has paid tax on his salary that he received in India and taxing it as Fee for Technical Service and will lead to double taxation, and the bench noted this. Singapore and India have a double taxation avoidance agreement (DTAA) between both countries. Yum Restaurants, situated in India, the assessee, is a company registered in Singapore and is involved in the occupation of franchising KFC, Pizza Hut, and Taco Bell brands in India.

The evaluating officer is supposed to check the existence of a service or DAPE (Dependent Agent Permanent Establishment) of the assessee in India and requiring acknowledgment of business revenue to the Permanent Establishment on account of the marketing activities carried out by the Indian Branch.

For the operation of outlets of KFC, the assessee has entered into an agreement known as Technology License Agreement (TLA[1]) for the license related to “Technology” as well as “System” with Yum Restaurants (India) Private Limited also known as YRIPL.

Yum Restaurants (India) Private Limited had appointed various franchisees for operating restaurants in India under the brand name of KFC and Pizza Hut. Yum Restaurants (India) Private Limited operated the company-owned KFC outlets in India. The Evaluating Officer was of the viewpoint that the person employed by the assessee, working under any Indian entity, was upheld to India; the salary of the person was compensated by the Indian entity and therefore taxable in the hands of the assessee in India.

Conclusion

The revenue department opposed that there is a Technical License Agreement between the assessee and the YRIPL, and there is a delegation of an employee of the assessee company in India. He additionally stated that the person employed in India was seconded to India, and the question was whether there was a PE (Permanent Establishment). The court of law in ITAT headed by Shushma Chowla, the Vice-President, held that the evidence is required to be seen in the entirety as the burden of proof that the foreign assessee has a PE in India and accordingly it has to be taxed on the business created by such PE is initially on the Revenue. In the nonappearance of the same, it cannot be said that the assessee had service PE in India.

Read our article: Is Capital Gain Tax incapable of levying upon Registration of Sale Deed? Know-How!