Numerous registered or unregistered NGOs (Non-Government Organisations) have been formed over the years and they indeed play a crucial role in the upliftment of the society. However, it is always recommended to get an NGO registered to utilize the benefits provided by the government and to attain legal status. In this Blog we are going to cover all the aspects of Role and Power of Commissioner under NGO Registration.

The Income Tax Act recommends specific powers to each level of income tax commissioners for accurate implementation of the various tax organizations in India. The central government has the rights to decide and appoint the officers for the posts of tax authorities who have passed the eligibility criteria.

What is the Power of Commissioner in registration of New NGO?

The Power of Commissioner in registration of New NGO is as follows-

Read our article:Everything you need to know about Statutory Controls of NGO

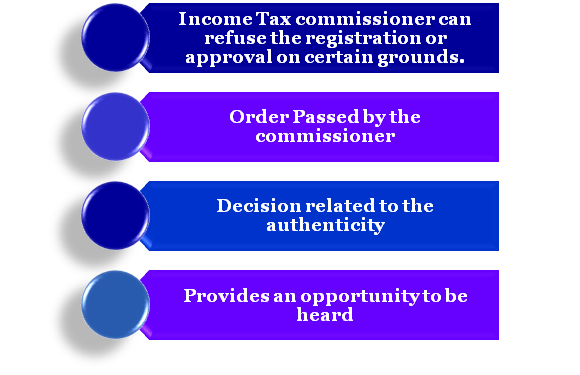

Income Tax Commissioner can refuse the registration or approval on certain grounds.

Following are the grounds in which the commissioner has the power to refuse or approve the registration:-

- If less than 85% of the property of the trust is dedicated towards social work, then Income Tax commissioner can refuse its tax exemption.

- If the property held under trust is not used for religious or charitable purposes entirely.

- If the amount generated from the NGO is used for the personal usage of the Founder, Trustee or his relatives, or any person who contributed more than Rs. 50,000 for the organisation for the respective financial year.

- If the Annual income return is not filed by the organisation and so on.

- Litigation between the Income Tax commissioner and an NGO looking forward to be registered has always existed.

Order Passed by the commissioner

Income Tax commissioner can order any organization to submit their relevant documents on the receipt of an application.

Decision related to the authenticity

Income Tax commissioner decides the authenticity of any organisation based on their workings.

Provides an opportunity to be heard

Income Tax commissioner can provide an opportunity to be heard to the NGOs which fail to prove their authenticity.

What is the Role & Power of Commissioner under the Registration of NGO?

The Power of Commissioner under NGO Registration are specified below-

Renewal of Existing Registration and Approvals

It is mandatory for the organisations which are already registered under section 12A/12AA of Income Tax Act, 1961[1] or have acquired the approval under section 10(23C) or 80G, to file an application under the newly inserted section 12AB or amended provisions of section of 10(23C) or 80G in order to receive a unique identification number. The application has to be filed within three months 3 months from the date on which the new provisions shall come into force that is on or before 31st August, 2020 for renewal of existing organisations and approvals.

The application filed for the renewal of the existing registration or approval has to be submitted before the income tax commissioner in whose area the NGO is located. In four metropolitan cities, the application is required to be sent to the Director of Income Tax.

Exemption

Any delay in filing the application will not be ignored by the authority, and the onus of acquiring tax exemption lies entirely on the organisation.

The Commissioner of income tax has to pass an order granting registration or approval within three months of application. An approval can be refused on certain grounds by the Income Tax Commissioner. The validity of the registration will last for five years, and has to be renewed every five years.

Renewal of Registration after every 5 years

Every NGO that has been granted registration under the Section 12AB is required to file an application for renewal after every 5 years and the renewal application has to be filed at least 6 months before the expiry period.

However, renewal of registration can also be refused by the Income Tax commissioner.

Registration of New Non-Profit Organisations

Registration under the newly inserted section 12AB or approval under section 10(23C) or 80G shall be granted to the NGO without any enquiries for 3 years.

Conclusion

There has always been a conflict between an Income tax Commissioner and an NGO. Any Income tax commissioner plays the most crucial role in the registration and approval of NGOs. The power of commissioner is to refuse the registration, to cancel the existing registration and to refuse the approval for tax exemption. If you want to know more about the NGO Registration contact our experts at Corpbiz

Read our article:An Outlook on NGO DARPAN Registration