Dropshipping is an e-Commerce business in which the seller does not hold any inventory. Whenever the customer placed an order on such a portal, the seller diverts the request to the third party for further processing.

Dropshipping has become immensely popular in India due to its productive and cost-effective business structure. The responsibility of the drop shipper is only limited to accepting an order, the rest of the formalities such as order packaging and delivery is fulfilled by the third party. Those who are about to step into this business model must get accustomed to tax implications.

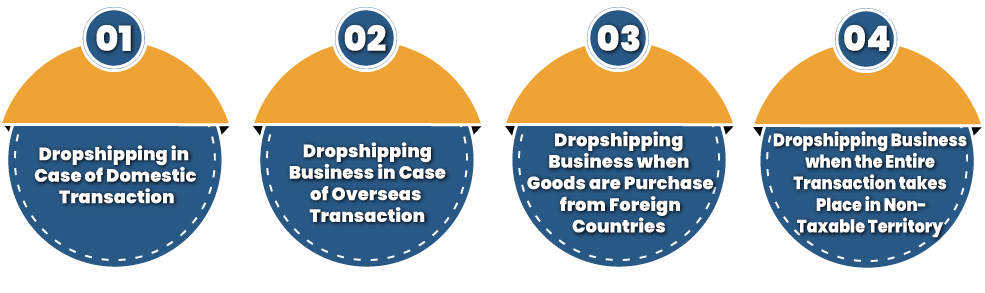

Applicability of GST on Dropshipping in Case of Domestic Transaction

Let’s understand the concept of Goods and services tax implication on dropshipping business through an example. Suppose there a person name Rohit who solely manages the dropshipping business. For packaging and delivery, he enters into a contract with a third-party entity known as ABC enterprise.

Now a person X places an order on Rohit’s website and pays the cost of the goods in a usual manner. As soon as Rohit receives the order, he forwards the request to the ABC enterprise for further processing and issues an invoice to the customers.

While dispatching the product to the customer, ABC enterprise won’t issue an invoice for the same since they are playing a third-party role and don’t have direct interaction with the customer. Therefore, ABC enterprise will issue an invoice to Rohit instead of the customer. Rohit can further avail of the input tax credit of such an invoice.

Both ABC enterprise and Rohit are required to get registered under GST if the turnover of their business exceeds the max threshold limit of Rs. 20/10 lakhs. The registration is also applicable in case the sales are made outside the union territory/states in which the seller has a place of business.

Applicability of GST on Dropshipping Business in Case of Overseas Transaction

When commodities are sold outside the Indian Territory, the drop shipper has to deduct GST from the person in dropshipping business (merchant). In the case of export sales, the merchant has an option to either pay IGST at the time of sale and seek a refund afterward or file a letter of undertaking to get exempt from GST for selling the goods.

For issuing an invoice to the merchant, the drop shipper can avail the benefit of CBIC’s notification issued on 23rd October 2017 and pay SGST & CGST @ 0.05% each or 0.1% IGST, as the case may be. This benefit is exposed to certain conditions as mentioned in the said notification.

GST on Dropshipping Business when Goods are Purchase from Foreign Countries

If the drop-shipper is operating from a place other than the Indian Territory then the merchant has to pay IGST based on RCM (reverse charge mechanism) at the time of import of goods. The merchant will issue the GST invoice along with IGST or CGST/SGST, as the case may be. The merchant can avail input tax credit against the IGST paid for the importation of goods.

GST on Dropshipping Business when the Entire Transaction takes Place in Non-Taxable Territory

In such cases, GST will not be levied. According to para 7 of the Schedule III of the CGST Act[1], any supply/transaction that takes place in the non-taxable location with no connection to the home country shall not be treated under the GST regime. If the merchant belongs to India and completes the entire business transaction outside the nation then in such case the GST will not be applied.

Services Used in Such Transaction

The owner of the dropshipping business might leverage services related to the packaging and transportation of goods in such a transaction. The services of the freight forwarder or courier are utilized for the transportation of goods.

In many instances, the drop shipper has to avail of services of the third party for the inspection of goods for quality. Now, this leads to a query whether such services come under the GST regime or deemed as the import of services?

According to Section 2(11) of the IGST act the term “import of service” is described as the supply of any service, where-

- The supplier of service is located outside India.

- The recipient of service is located in India.

- The place of supply of service is in India.

Henceforth, transactions subjected to these conditions will be treated as the import of services.

According to Section 13(5) of the IGST Act when the services supplied are related to goods which are needed to be made available by the merchant to the suppliers of services then place of supply will be the location where services are performed. Henceforth, in the case of quality inspection services, the place of supply will be the location where such inspection is performed.

Essential Points to Ponder

- Taxpayers are not required to mention sales that are not treated as supply under the GST regime in GSTR-1 and GSTR-3B.

- GSTR-3B doesn’t seek to report of purchase of supply which is not considered as the import of service under GST regime

- Taxpayers belong to the taxable location are liable to pay GST based on RCM if the services are availed from foreign a country that is not directly related to the goods.

- Any business transaction of dropshipping business occurs in the non-taxable region i.e. outside India is not subjected to tax deduction under GST.

- Dropshipper holding a warehouse for goods outside India need not be pay GST

Conclusion

Dropshipping is a cost-effective business model that allows individuals to build their online store without having an inventory. Currently, the margin of profit under this business model is sustainably higher and it’s likely to grow over time. The implication of the GST on such business models is subjected to various conditions as mentioned above. If you need further clarification on this then connect with CorpBiz’s expert without any second thought.

Read our article: GST Exemption on Satellite launches for Encouraging the Domestic Launch