A few years back, the Banking and Finance sector came across a pleasant surprise when the Government declared the Financial Resolution & Deposit Insurance bill’s withdrawal. This declaration continues to disrupt sectors owing to the persistent loophole in the framework governing the stress in FSPs, i.e., financial services providers. Till the arrival of Insolvency and Bankruptcy (Insolvency & Liquidation Proceedings of FSPs & application to Adjudicating Authority) Rules, 2019, the Insolvency & Bankruptcy Code, 2016 (“IBC”) did not cover financial Service Providers. Currently, the FSP rules only cover non-banking finance companies, i.e., NBFC, whose asset size is over INR 500 crores. The infamous IL&FS default & evolving stress in the banking sector necessitating the prompt inculcation of a holistic regulatory framework for all financial Service Providers. In this write-up, we will talk about Insolvency Resolution for NBFCs: All you Need to know.

Overview & Coverage of the FSPs Rules

As per FSP Rules, the IBC’s provision related to insolvency resolution process of the corporate mutatis mutandis apply to the FSP’s insolvency resolution process subject to some vital rectification, which are:

- The FSP’s CIRP (Corporate Insolvency Resolution Process) shall come into effect only by an apt regulator such as RBI.

- On admission, an administrator equivalent to resolution professional under IBC is appointed;

- An interim moratorium shall come to effect from the application’s filing date till its admission or denial by the NCLT;

- The moratorium’s provisions shall not cover any third-party assets or properties in possession of the Financial Service Provider, including any securities, funds, & other assets needed to be held in trust for the third parties’ benefits; and

- Upon resolution plan’s approval, the Administrator shall ask for NOC from the appropriate regulator to ascertain the ‘fit & proper test.

Read our article:NBFC Registration: Step by Step Procedure

What are the Implications of FSP Rules?

Given that financial Service Providers have a significant part to play in India’s financial stability, the protection of the rights of FSPs deposit holders, if any & the protection of the linked economy that they cater is also paramount. It has been declared that these rules are “an interim measure,” & thus, while the other entities such as insurance providers, banks, stock exchanges, clearing corporations, etc., are a different concern altogether.

Amidst the ongoing situation, it might be a suitable time to review the Resolution Corporation’s principal & identify a feasible solution to the inevitable stress & not let issues dictate the solution in upcoming days. Each financial services provider in isolation may not inevitably be “too big to fail,” but they certainly have the build to seek holistic unified regulation.

Benefit for FSPs Regarding the Accessibility to Insolvency Resolution Process

- Avail rights as that of other corporations that come under IBC

- Prompt Settlements of evolving fiscal issues

- No confrontation with initial legal requisites such as plea submission before NCLT

- Access to interim moratorium from the date of application filing

Key Takeaways Related to FSP Rules & 18 November Notification

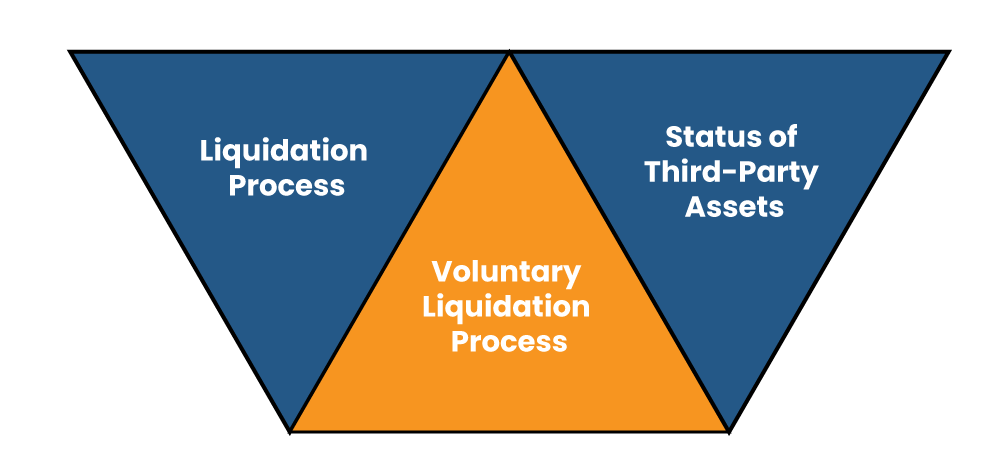

The following points will let you understand FSP rules’ scope subjected to the different conditions such as liquidation process and status of third-party assets.

Liquidation Process

In the liquidation process, the license of the registered FSPs shall not be canceled or suspended without rendering a chance of being heard to the liquidator. The Adjudicating Authority shall enable the appropriate regulator to share the concern before issuing the liquidation order. It’s worth noting that the FSP rule lacks any guidance on the license suspension if the Administrator strives to liquidate the FSP.

Voluntary Liquidation Process

The FSP must avail prior consent of the appropriate regulator to initiate voluntary liquidation proceedings u/s 59 of the Code. Moreover, the adjudicating authority is mandated to provide an opportunity to the relevant regulator of being heard before issuance of dissolution order for FSP.

Status of Third-Party Assets

Following the initiation of the corporate insolvency resolution process, the Administrator shall take control & custody of third-party assets or properties, in trust, for the benefit of the same and shall deal with them as per the direction of the Central Government[1] under Section 227. The notification released on 18 November does not provide any mechanism for the handling of such assets and merely implies that this would be promulgated subsequently

Expert’s Opinion on the Amendments to IBC Act

According to the rating agency Moody, the amendment to IBC enabling the resolution of FSPs is credit positive for banks. India’s banks are a prominent lender to NBFIs operating across this country. The provisions in the IBC aim systematic resolution of the stressed companies.

Until now, liquidation is the only viable source of resolution for the NBFIs. The agency is assured that such measures will help minimize losses for creditors as a comparison to the liquidation.

- The corporate insolvency resolution process i.e., CIRP for FSPs, would be initiated “only on an application by the appropriate regulator”.

- One of the substantial reasons given for keeping out FSPs from the ambit of the Insolvency and Bankruptcy Code, 2016 (IBC) was the opinion that such entities deal with public money and insolvency provided to them could trigger economic instability.

- The distressed economy, the liquidity crunch incurred by the FSPs such as DHFL, & compromised restructuring mechanisms for certain FSPs have led the inculcation of mechanism for restructuring FSPs under Insolvency and Bankruptcy Code, 2016 (IBC)

Conclusion

The financial sector has been encountering a liquidity crisis for a long time. The exclusion of NBFCs from the insolvency resolution process under the Code has remained a severe concern for years. While some well-known players failed to cope with financial stress, several investors & creditors of stressed NBFCs strived to resolve the issue by using options such as Reserve Bank’s 7 June 2019 Circular. However, the absence of holistic mechanisms such as Code & multiplicity of legal proceedings disrupted the resolution of fiscal stress. Therefore, an extension of resolutions under the Code to the FSPs was widely expected. The issuance of the FSP rules and association with 18 November Notification has made a unified resolution process available to financial entities and their creditors with some procedural differences. Undoubtedly, the extended ambit of the Code has closed a gap in the corporate Insolvency resolution regime.

Read our article:Types of NBFCs in India – An Overview