Understanding the head of Income from Other Sources is residuary in nature. It includes incomes which are not taxable in other heads of income. Income from Other Sources is one of the heads of income chargeable to tax under the Income tax Act. 1961. Any income that is not covered in the other four heads of income is taxable under income from other sources, because of this, it is known as residuary head of income. All the incomes excluded from salary, capital gains, house property or business & profession (PGBP) are included in IFOS, except those which are exempt under the Income Tax Act.

What are the Heads of Income under Income tax?

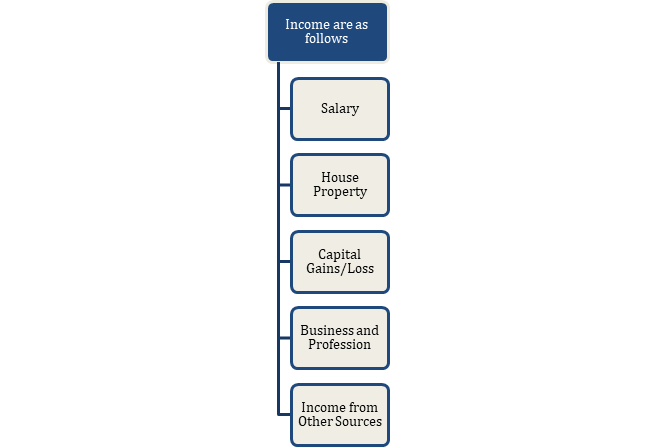

The Income Tax Department of India classifies income into five categories for streamlining the process of income tax reporting.

What Income Tax Act says about “Income from other sources”?

According to the Income Tax Act[1], the income of every kind which should not be excluded from the total income shall be chargeable to income tax under the head ‘Income from other sources’, if it cannot be chargeable to income tax under any of the other heads of income. As a result, income from other sources is a residuary head of income i.e. income which cannot be chargeable under any other head is chargeable to tax under this head. All income other than income from salary, house property, business, and profession or capital gains, etc. is covered under ‘Income from other sources’. Given below is the list of “Income from other sources’:

Section 56- Incomes taxable only in Income from Other Sources

- Dividend Income;

- Income earned from winning lotteries, crossword puzzles, races (including horse race), gambling or betting of any kind;

- Money or movable/immovable property received without consideration or inadequate consideration during previous year;

- Interest on compensation or enhanced compensation received;

- Advance money received or money received in negotiation for transfer of a capital asset (only if the money is forfeited and it doesn’t result in the transfer of such asset).

Incomes taxable under IFOS, only if not taxable under Profits and Gains of Business or Profession (PGBP)

- Any sum contributed towards provident funds, ESI, etc. by employee to the employer, only if not deposited in the relevant fund;

- Interest earned on Securities;

- Income received from the letting of a plant, machinery or furniture, with or without building.

Incomes taxable under IFOS, only if not taxable under PGBP or Salaries

- Key man Insurance Policy;

- Salary of MP/MLA

Income Computation and Disclosure Standards: Section 145 states that Income from Other Sources must be computed on the regular accounting methods followed by the assessee. It can be either cash or mercantile system of accounting. The Central Government has notified Income Computation and Disclosure Standards to be followed while computing the income.

Section 57- Expenditures allowed as deductions

- Expenses incurred for realisation of dividend or interest income;

- Deductions to the extent amount remitted within due date are authorised in respect to contribution towards funds for the welfare of employees;

- Family Pension- deduction is allowed to the extent of 33-1/3% of pension or Rs. 15000 whichever is less;

- Deductions for current repairs, insurance and depreciation, will be allowed for income earned by way of lease rental;

- A deduction equal to 50% will be allowed for interest received on compensation or enhanced compensation.

Read our article: A Complete Guide on How to Save Income Tax

Section 58- Sum not allowed as deductions while computing taxable income

- Personal expenditure;

- Interest or salary payable outside India without TDS deduction;

- Wealth tax;

- Expenditure concerning winnings from lotteries, crossword puzzles, races, and gambling, etc.; and

- Expenses specified in Section 40A.

What are the items which are generally classified under “Income from other sources”?

The following incomes are chargeable to tax:-

- Dividend received from an Indian Company has been made exempt in the hands of the receiver. Accordingly, dividend received from a foreign company or any cooperative bank received from a foreign company will be taxable as income from other sources.

- Any pension received by the legal heirs or representatives of an employee.

- Any winnings for an amount above Rs. 10,000 from lotteries, crosswords, puzzles, races including horse races, card games or other games of any sort or gambling or betting of any form or nature.

- Income from any plant, machinery or furniture let out on hire where it is not the business of the assessee to do so.

- Income from securities by way of interest

- Any kind of sum received by the assessee from his employees as a contribution to any staff welfare scheme

- Income from subletting the premises

- Interest on the number of bank deposits

However when an assessee makes the payment of such contribution within the time limit under the scheme of welfare, then the payment will be allowed as a deduction and only the balance amount will be taxable.

Income classified under Income from Other Sources if not taxable under the head “Profits and gains of business or profession”?

- Any kind of contribution to a fund for the welfare of employees received by the employer

- Any Income received by way of interest on securities.

- An Income earned by letting out or hiring of any plant, machinery or furniture item.

- Income from letting out of a plant, machinery or furniture along with building; both the lettings are inseparable.

- Any amount of money received including bonus under a Keyman Insurance Policy.

Conclusion

Income from other sources includes and means all those residual income that cannot be placed in any other heads of income. ‘Income from Other Sources’ can be defined as an income that is not included in any of the above-listed categories. However, there are certain other incomes that are always taxed under Income from other sources. These generally include interest income from savings bank accounts, post office savings accounts, fixed deposits, recurring deposits, family pension, etc.

Read our article: What Is A Tax Residency Certificate, And How To Get It?