GTA under GST means any person who provides service concerning the transport of goods by road and issues consignment note, by whatever name called.

What are the rates for GTA under GST?

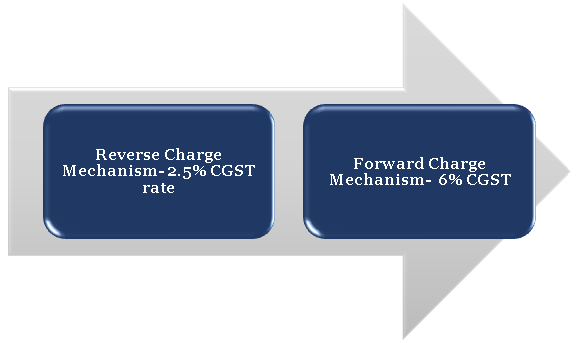

Goods Transport Agency has the option to charge Goods and services tax at the rate of 2.5% or 6% CGST (equal SGST and 5% and 12% IGST). The GST rates are reliable on taking input tax credit. The Classification based on Heading 9965 – Services of GTA concerning the transportation of goods

- GST Rate 2.5%

Provided that GTA does not take credit for input tax charged on goods and services used in supplying services.

- GST Rate 6%

Providing that the goods transport agency opt to pay tax @ 6%, and hence, they should be liable to pay fee @ 6% on all the services of GTA.

What do you mean by Consignment Note?

Consignment note is a document allotted by a goods transport agency (GTA) against the receipt of goods for the transport of goods by road in a goods carriage, which is serially numbered. It contains the name of the consignor and consignee, registration number of the carriage of the goods in which the goods are transported, details of the products carried, details of the place of origin and destination, the person accountable for paying service tax to the goods transport agency (GTA).

Issuance of any consignment note is the sine-qua-non for a supplier of service to be considered as a Goods Transport Agency. If the transporter does not issue such a consignment note, the service provider will not come within the domain of GTA. If a consignment note is delivered, it designates that the spleen on the goods has been transferred to the transporter, and the carrier becomes accountable for the products until its safe delivery to the consignee.

Explain Reverse charge mechanism (RCM) for GTA under GST

Reverse charge mechanism means the accountability to pay tax by the addressee of the supply of goods or services or both instead of the supplier of products or services or both.

Read our article:CBIC allows Functionality to file Revocation Application for cancelled GST Registration

RCM for GTA services

Supply of Services by a GTA who did not paid tax at the rate of 6%, in respect of transportation of goods by road to –

- Any factory listed under or governed by the Factories Act, 1948;

- Any society listed under the Societies Registration Act, 1860 or under any other law for the time being in force in any part of India;

- Any co-operative society well-known under any law;

- Any person listed under the Central Goods and Services Tax Act or the Integrated Goods and Services Tax Act or the State Goods and Services Tax Act or the Union Territory Goods and Services Tax Act

- Anybody corporate established under any law;

- Any partnership company, registered or not under any law association of persons

- Any casual taxable person.

Thus, the recipient of services has to discharge GST at a concessional rate of 2.5% CGST.

What is GTA under GST for Forward Charge Mechanism and Reverse Charge Mechanism?

What are exemptions available to GTA under GST?

Exemptions of services provided by a GTA are as follows:-

- Agricultural products;

- Goods, where deliberation charged for the transportation of products on a shipment transported in a single carriage, does not exceed INR 1500;

- Goods, where deliberation charged for transportation of all such goods for a single consignee, does not exceed INR 750;

- Milk, salt and food grain including flour and pulses;

- Organic manure or fertizers;

- Newspaper or publications listed with the Registrar of Journalists;

- Relief materials meant for sufferers of natural or human-made disasters, calamities, accidents or mishap

- Defence or military equipment[1]

Facilities by way of giving on hire to GTA under GST, a means of conveyance of goods. Therefore, if the GTA hires a method of transportation of goods, no GST is payable on such transactions.

Are intermediate and additional services to be treated as part of the GTA under GST?

GTA delivers service to any person concerning the transportation of goods by road in a goods carriage, which is a composite service. Intermediary and ancillary services may include various functions such as loading/unloading, packing/unpacking, transhipment, and temporary warehousing, which are provided in the course of transport of goods by road. These services are not offered as independent services but as a subsidiary to the principal service, namely, transportation of goods by road. The statement issued by the GTA for providing the facility contains the value of intermediary and additional services.

Because of this, if any intermediary and ancillary service is provided concerning the transportation of goods by road, and charges, if any, for such services are included in the invoice issued by the GTA, such assistance would form part of the GTA service. It would not be treated as a separate supply. Any service is being provided along with any GTA service that is part of the compound service of GTA should be taxed along with GTA service and not as discrete supplies.

Though, if such secondary services are provided as separate services and charged separately, whether, in the same invoice or separate invoices, they should be treated as different supplies.

What is the place of source for GTA under GST?

Suppose services provided to a registered person, place of supply will be the location of the personal residence. If services provided to any unregistered person, a place of supply will be the location at which such goods are handed over for their transportation. However, where the site of the supplier of services or the situation of the recipient of services is outside India, place of supply of services of transportation of goods by GTA shall be the place of destination of such products.

What are archives and accounts to be maintained by GTA under GST?

Every transporter should maintain records of the consigner, consignee, and any other relevant particulars of the goods in a prescribed way. A person involved in the business of transporting goods shall maintain records of products carried, delivered, and assets stored in transit by him along with the GSTIN of the registered consigner and consignee for each of his branches.

Conclusion

If services provided to any unregistered person, a place of supply will be the location at which such goods are handed over for their transportation. However, where the site of the supplier of services or the situation of the recipient of services is outside India, place of supply of services of transportation of goods by GTA shall be the place of destination of such products.

Our CorpBiz group will be at your disposal if you seek expert advice on any aspect related with GST Registration with complete compliance. We will help you safeguard full compliance concerning all the supplies based on your anticipated activities, ensuring the productive and well-timed completion of your expectation.

Read our article:Procedure for Appeals under GST