The Goods and Services Tax Network has allowed the System to compute liability for GSTR-3B that is Table-3 for liabilities based on GSTR-1 filed by taxpayers are now available on the GST portal.

What is GSTR- 3B?

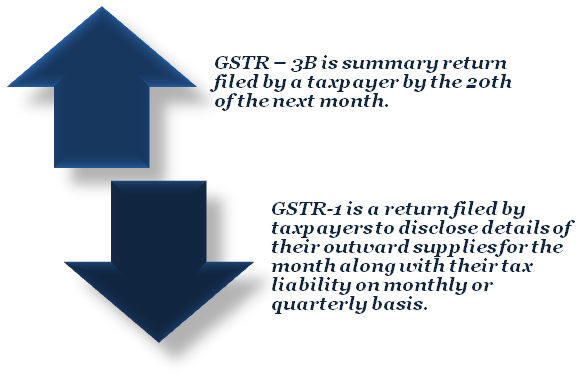

GSTR-3B is summary return filed by a taxpayer by the 20th of the next month. It is a monthly return. In this Form, taxpayers are required to summarize and report the total values of purchases and sales, without invoice details.

GSTR-3B relates with supplies made during the month in which Goods and services tax is to be paid, ITC claimed, purchases on which reverse charge is applicable and also makes a provision for the payment of taxes for the relevant month.

What is GSTR-1?

GSTR-1 is a return filed by taxpayers to disclose details of their outward supplies along with their tax liability on monthly or quarterly basis. In GSTR-1, invoice details are required to be uploaded so that the Government can keep a track of every transaction. This helps the recipient of supplies to accept and take the eligible input tax credit.

Read our article:Multiple Registration Under GST

Interpretation of the Notification

According to the notification, the Goods and Services Tax Network has allowed the System to compute liability for GSTR-3B that is Table-3 for liabilities based on GSTR-1 filed by taxpayers are now available on the GST portal.

Comparing GSTR-3B with GSTR-1 is a necessary process to be undertaken by every taxpayer to ensure no variations or gaps. That could lead to demand a notice from the tax authorities or any unwanted issues that can arise and hinder the accurate filing of the annual GST return.

What is the difference between GSTR-3B & GSTR-1 Forms?

It is a summarized return Form while GSTR-1 is a reporting of all output invoices and taxes on them. It was originally visualized that GSTR-3B and information and taxes as performs GSTR-1, 2, 3 will be prepared to be accepted via system based reconciliation.

It has been understood that the two Forms are not supposed to be a one-on-one match. A difference may exist due to many reasons, those are as follows:-

- Order received last minute and not included;

- Sales incorrectly counted twice;

- Inter-state supply unintentionally shown as intra-state supply or vice-versa;

- Sales returns not included or exports wrongly included.

Invoices which are not confined via summarized GSTR-3B are then offered in the next month’s GSTR-3B, and due tax[1] and interest on it must be paid next month itself.

Conclusion

Taxpayers have to report the full invoicing of a month in its GSTR-1 form, including missed or incorrectly details reported in the same month’s GSTR-3B. It’s a common mechanism. In case of system reconciliation any additional tax liability adds up on its own with the filing of the three forms, it should be paid accordingly. Without this mechanism any reconciliation done between GSTR-3B and GSTR-1 is likely to make gaps which can be due to the reasons as mentioned above.

Read our article:CBIC: Extension of deadline for GST Return Filing FY 2019-20