Company is a voluntary association of persons who come together to carry on some business and share profits after company registration. There are different types of companies specified under the Companies Act, 2013[1], and Government Companies is one of them. The Government Companies are owned and managed by the Central and State Government or both. The Government Companies under Section 394 are directed to place their Annual Reports before the Parliament or State Government. In the article, we will discuss the overview of the Government Companies Annual Reports.

What is a Government Company?

A Government Company is defined under the Companies Act, 2013, under Section 2(45) of the Act. The Company in which not less than 51% of the paid-up share capital is held by:

- The Central Government, or

- The State Government, or

- Partly by the Central Government partly by one or more State Government(s), or

- Includes the Company which is a Subsidiary Company of such Government Company.

The Subsidiary Company of a government company should also be considered as a Government Company. The main objective of the Government Company is to gain momentum in the growth of the nation.

What are the Features of Government Companies?

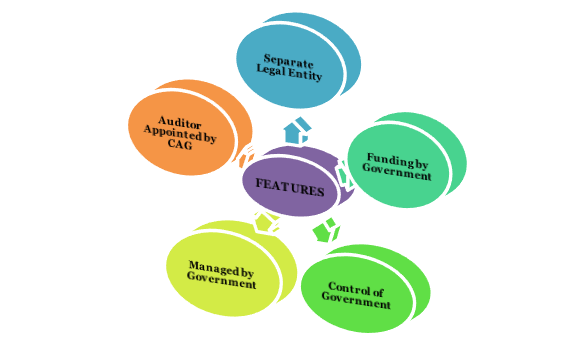

The different features of the Government Company are as follows:

- It is a separate legal entity.

- The incorporation of Government Companies is under Companies Act, 2013.

- The management and control of Government Companies are under the Companies Act, 2013.

- The funding of Government Companies is received from the government shareholdings and certain other private shareholdings.

- The auditing of the Government Companies is done by the agency appointed by the Central Government. The agency is the Comptroller and Auditor General of India (CAG).

- The Board of Directors manages the Government Companies. The Central Government appoints the Board of Directors.

What are the provisions Governing the Government Companies Annual Report?

Under the Companies Act, 2013, the following provisions provide for the Government Companies Annual Report:

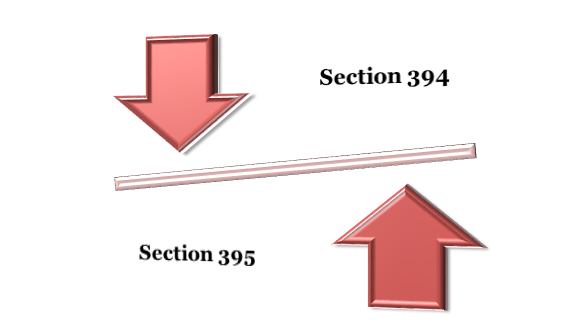

Section 394

Section 394 of the Companies Act, 2013, states the provision for presenting of Government Companies Annual Report by the Government Companies. The Central Government will direct the CAG to direct and administer the accounts of the Government Companies. The CAG then appoints an Auditor to manage the performance and functioning of the Government Companies. The CAG appoints the Auditor to manage the financial functioning of the Company.

The CAG can conduct supplementary test audits by the persons authorised by the CAG as per Section 143 of the Companies Act, 2013. The Auditor of the Government Companies should submit a copy of Government Companies Annual Reports to the CAG for any comments or supplements. The comments by CAG should be made within 60 days of the date of receipt of the Tax Audit Report as per Section 143 of the companies Act, 2013.

Audit Report, when presented by Auditor in the Annual General Meeting, the comments and supplements made by CAG, should be mentioned in its original form in the Audit Report.

As per Section 394 of the Companies Act, 2013, the following conditions should be considered while presenting Government Companies Annual Report:

- The Central Government should submit the Government Companies Annual Report before both the Houses of the Parliament.

- The Government Companies Annual Report should explain the working and affairs of the Government Companies.

- The Government Companies Annual Report should also include the general description of the industry in which the Government Company is involved.

- The Government Companies Annual Report should be presented within 3 months of the Annual General Meeting.

- The copy of the comments by the CAG on the Audit Report should also be added in the Annual Report.

In addition to the Central Government, if the State Government is also a member of the Government Company, the Government Companies Annual Report should also be submitted to both the Houses of the State Legislatures. The copy of comments by the CAG on the Audit Report of the Government Company should also be added in the Government Companies Annual Report.

Section 395

Under Section 395 of the Companies Act, 2013, provides for the Government Companies Annual Reports where one or more State Government(s) is a member of Government Company. The following conditions are provided under Section 395 of the Companies Act, 2013:

- Every State Government of the Government Company should prepare Government Companies Annual report on the functioning of the Company.

- The Government Companies Annual Report should be prepared within 3 months of the date Annual General Meeting held of the Government Company.

- The preparation of the Annual report should be done as per Section 394 of the Companies Act, 2013.

- The copy of the comments on the Audit Report by the CAG should be submitted with the Audit Report.

Conclusion

Government Company is owned and managed by the Central Government. Section 394 and 395 of the Companies Act, 2013, provides for the provision for Government Companies Annual Report. The Auditor should present the Government Companies Annual Report within the prescribed time. We at Corpbiz have expert professionals who can assist and help you in your work. Our experts will assure the successful and timely completion of your work.

Read our article:Procedure of Filing Annual Return: A Complete Guide