FinTech, aka financial technology, is that segment that deals with conventional finance business through the method of P2P model, crowdfunding, asset management, and mobile payments loans. Technically, these firms do not fit with the legal definition of a bank, as mentioned under the Companies Act 2013. Widespread internet penetration and the wave of digitization have led to the surge in Fintech sector funding from venture capitalists. The advent of the Unified Payment Interface (UPI)* platform has changed the way we looked at conventional finance and payment services. Complete Digitization of Banking services could be the next big in the Fintech Sector because it adheres to unprecedented growth. But could it be easy for Fintech Startups to stroll on that path with ease? Let’s find out.

Unified Payments Interface* (UPI) is a digitized payment system that facilitates inter-bank transactions. The National Payments Corporation of India developed this system, and the Reserve Bank of India is the one that regulates it.

Why Several Fintech Startups are looking for an NBFC License?

There are many companies in India that are rapidly solidifying their presence in the Fintech business. All these firms in India are now approaching Reserve Bank to avail their NBFC license. According to many experts, the reason behind this is to maintain the loan books rather than sharing the profit with the partner.

The grant of NBFC license to such companies will affect the loan disbursement process and cost of capital. Nevertheless, it will reduce the cost of capital and speed up the loan disbursal process. According to some industry experts, this will help to curb fraudulent activities using technology and scaling up operations.

Read our article:Documents Required for NBFC Registration

Underlining the Potential of Fintech firms to become a Full-Fledged NBFC

Fintech is the modern approach to financial services. Since these firms leverage the latest technology, they have more potential to deliver quality services to the users. Below are some pros of fintech firms that make them perfectly suitable to work as a full-fledged NBFC in India

Potential to Rejuvenate Traditional Banking System

FinTech has been resonating strongly in the Indian financial space since its inception. They have also become an integral part of the Government’s mission regarding financial inclusion. Owing to its unparalleled potential to rejuvenate the traditional banking system, the FinTech space is now garnering popularity in the areas of lending, deposits, asset management & credit system.

Ability to Render Diverse Services

At present, these entities are taking full advantage of the latest-gen technologies to mitigate challenges & build products such as enterprise automation for accounting, last-mile reach and delivery, fraud detection, alternative credit models, treasury and reconciliation for private lenders and, regulatory compliance.

Access to Alternative Data Sources and Latest Tech

Traditionally, lenders excelled on the ‘one size fits all approach, evaluating all types of clients against standard credit policy. Such an approach is excluding a large population of potential customers. With FinTechs adopting AI combined with ML, it becomes easier to render personalized services to the clients.

Under the influence of alternative data sources, Fintech has the ability to take correct and swift decision, particularly in the case where the creditworthiness of the customers is in question.

Current Challenges for Fintech Startups to Work as a full-fledged NBFC

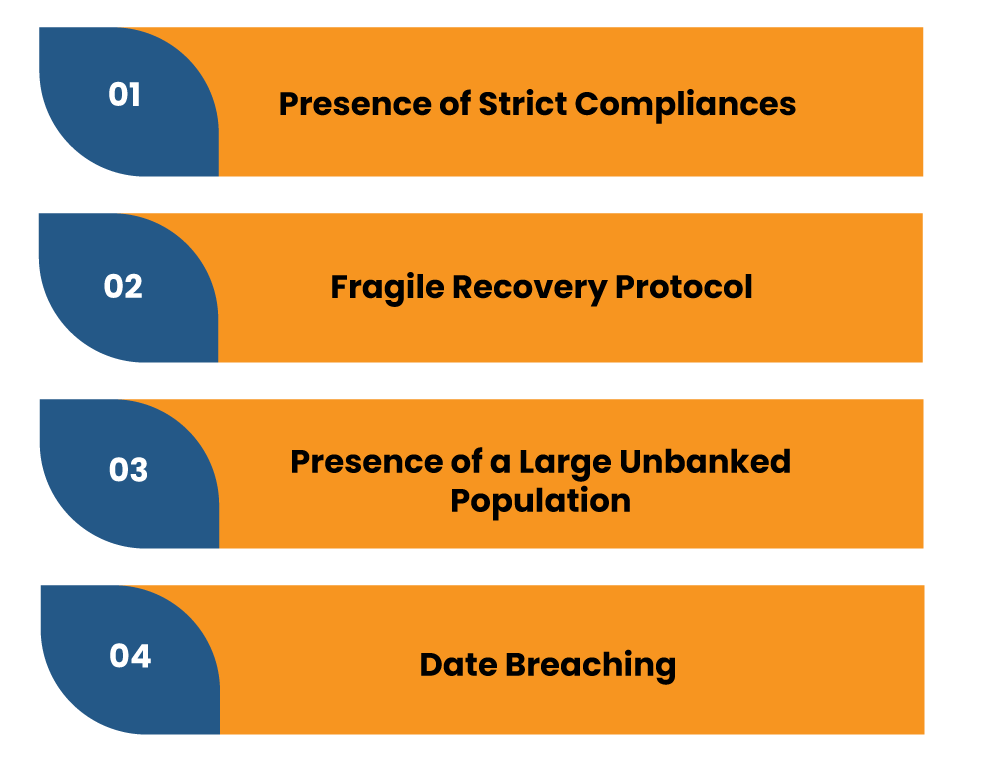

The list below consolidates the potential loopholes that are considered as the biggest obstacle for the growth of new Fintech entrants.

Presence of Strict Compliances

Many laws and regulations in India contribute to the slow-down of Fintech startups in the financial markets. Not only these laws are stringent, but they have also discouraging Fintech players from making their way into the Indian market.

Compliance laws exist as a restrictive regulatory framework to mitigate fraudulent activities. But, sadly, new Fintech entrants are finding them as the biggest obstacle in the path of growth. Practically, there is an extensive list of compliances that Fintech startups need to meet before starting their operation.

Fragile Recovery Protocol

Most Fintech startups might find it hard to build a robust management for credit recovery. Maintaining a continual connection with credit seekers for outstanding payment seeks raw professionalism and a good code of conduct, which is something quite daunting to maintain.

Presence of a Large Unbanked Population

Even today the large portion of Indian population lack access to proper banking services that makes them depends on cash transaction instead of online purchases. A government initiative like Pradhan Mantri Jan Dhan Yojana has tried to fix that loophole to some extent, but that too remained largely ineffective owing to low internet penetration and literacy levels. Catering to such a section of the population will be a daunting task for the Banks and new Fintech entrants.

Date Breaching

Most Fintech companies have an abundance of customer data to deal with. Constantly monitoring and securing such data against a possible cyber threat is a paramount challenge for these firms. Any loophole in this regard could result in massive financial losses during web-based transactions. Therefore, ensuring end-to-end encryption to customer’s data is a fundamental concern for the new Fintech entrants.

Inculcation of Robust KYC and Consumer Grievance Mechanism

Setting up a Know Your Customer (KYC) and consumer grievance mechanism would add to the hardship of these firms. Also, it seems that these firms would have no control over the customer’s bank account, fees, and charges that the bank administers. Since these firms will operate as a technology player, they might not have access to all banking services.

Conclusion

There is no denying that Fintech startups are playing an essential role in revolutionizing India’s financial services. At present, there are several Fintech startups that have partnered with Banks and leveraging their Application Programming Interface (APIs).

While performing such actions, these firms are under obligation to stay in line with existing regulations. In light of the ease of doing business, the Indian government[1] may sooner or later decide to speed up the digitization of banking services. And that’s the only thing that keeps the hope of many distressed Fintech entrants alive.

Read our article:NBFC Registration: Step by Step Procedure