Education is one of the most powerful weapons which can be used to change the world and also an effective way to break the cycle of poverty in India. Government through its Right to Education Act, 2009 have been trying to put up Educational Institution as NGO in its way to enroll and maintain children in school particularly from the marginalized sector of India.

Registration of Educational Institution as NGO

Formation of an Educational institution is quite complex and promoters always prefer a suitable form of Educational Institution to be formed. The registration process as well as compliances for different form of entity in which educational institution as NGO can be formed, they are-

Registration of Educational Institution as a Charitable Trust

Educational Institutions can be registered as Trust under Indian Trust Act, 1882. Trusts are formed by trust deed containing vital information such as information related to trustee, rights & duties, operations of trust and most important of all is objective of the Trust.

The trust deed should be submitted to the local registrar with all the requirements and at the time of the settler and two witnesses with proof of identity should be present. The registrar will keep a photocopy of the deed and return the original one. After registration, the trust should apply for PAN card as it is an important document for income tax registration from the department of income tax.

Registration of Educational Institutions as a Society

An educational institution can be Registered Society according to the Societies Registration Act 1860. A society can be formed by group of 7 or more persons for charitable, scientific purposes & literary as defined in Section 20 of the said act.

The associated persons are required to subscribe their name in Memorandum of Association (MoA) and file it with registrar.

Exemption Provided to Educational Institution as NGO

Analysis of certain exemptions given to Educational Institution as NGO under Section 10(23C) in comparison with exemption available under Section 11 of the Income Tax Act, which are as follows-

What is the background Section 11?

Section 11 of Income Tax Act[1] is a popular section to claim exemption from tax between the charitable trusts and institutions. The majority of the charitable trusts are registered as per section 12AA of the said Act and it can claim exemption as per Section 11. While the exemptions available under section 11 are common and accessible for all the charitable organizations and institutions, Section 10(23C) of the said Act is an explicit exemption obtainable to specific Governmental as well non-governmental educational institutions.

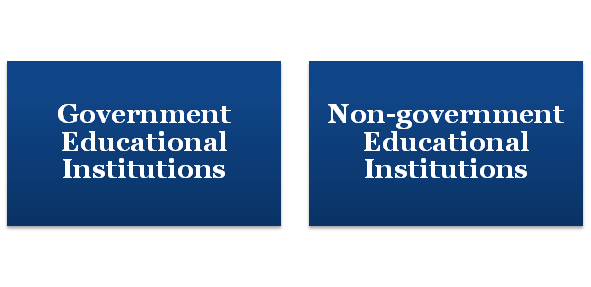

Situations Prevalent for Claiming Exemption for Educational Institution as NGO

Following are the prevalent conditions for exemptions-

Government Educational Institutions

Income received by any educational institution obtainable exclusively for educational purposes. It should not be instituted for purposes of profit. Educational Institution is wholly or substantially financed by the Government is fully exempted from tax through Section 10(23C) (iiiab). Therefore, a Government educational institution is fully exempted from tax without any separate approvals as long as it does not have any profit motive.

Read our article:An Outlook: Registering an NGO in India

Non-government Educational Institutions

The exemption for non-government educational institutions depends on the collective annual receipts of the educational institution. They are as follows-

Educational Institutions with annual turnover up to 1 crore

Section 10(23C) (iiiad) specifies that the income earned by any educational institution or university existing exclusively for educational purpose will be exempted from income tax if the annual receipts of such university or educational institution does not surpass INR 1 crore.

Therefore, an educational institution having receipts up to INR 1 crore can claim full immunity under the above mentioned clause without any separate approval as well as registration.

Educational Institutions with annual turnover exceeding 1 crore

Exemption in the case of an educational institution or university having turnover exceeding INR 1 crore is directed by Section 10(23C) (vi) which says that income earned by any educational institution accessible exclusively for educational motive. Things mentioned in sub-clause (iiiab) and sub-clause (iiiad) is exempted if they are approved by the approved authority. Thus, where the total turnover of the educational institution exceeds INR 1 crore, the organization needs a separate approval to claim exemption as per Section 10(23C).

The Application for approval is necessary to be made in Form 56D with the essential documents before the Commissioner of Income Tax. Just like the approval under Section 12AA, the approval under Section 10(23C) is also available for an indefinite period unless it is withdrawn by the authorities.

Further Conditions

The third proviso to Section 10(23C) gives the following conditions:-

Spend minimum 85%

The educational institution should spend its income entirely and exclusively for the objective for which it was established. Additionally, the educational institution should apply for at least 85% of the income every year. Consequently, registration under Section 10(23C) does not result in full exemption of Tax. The institution has to spend at least 85% of total income to claim full exemption of tax.

In case the income that is applied falls short of 85% then the educational institution have to accumulate excess income for application in following year which does not exceed five years.

On the other hand, the accumulated amount is said to be spent by the educational institution on its own as it cannot spent it by way of donations to any other trust registered according to 12AA of the said Act or another institution claiming exemption under Section 10(23C) of the Act.

Investments

The second condition is that the educational institution should invest its money only in the forms specified according to section 11(5) of the Income Tax Act. This provision is similar to the other provisions applicable under Section 12AA.

Other Relevant Conditions

Some other conditions are as follows-

Income Tax Return

By the standards of 139(4C) all educational institution mention or allude to in sub-clause (iiiad) or (vi) of Section 10(23C) whose entire income, without any consequences regarding the provisions of section 10, surpasses the maximum amount which is not taxable under income-tax, should endow a return of income. Hence, if the total receipts of the organization exceeds INR 2,50,000/-, it has to file the return of income. The Form of Income Tax Return (ITR) is ITR-7, the same is applicable for a Section 12AA registered Trust.

Audit

Proviso no. 10 to Section 10(23C) states that when the total income of an institution, without any consequences regarding the provisions of this section, exceeds the maximum amount which is not taxable any preceding year, such establishment should get its accounts audited and furnish along with the income return for the applicable assessment year, the report of such audit is provided in Form No. 10BB. Hence, if the total receipts of the establishment exceeds INR 2,50,000/-, it should file the return of income.

Corpus Donations to other Trusts

Proviso no. 12 to the Section 10(23C) further states that any amount paid or credited out of the income of any educational institution or university to any institution registered under section 12AA or to any trust, being a corpus donation should not be taken as application of income to the objects for which such educational institution or university is established. Hence, the educational institutions or university registered under section 10(23C) (VI) are excluded from giving corpus donations to other Trusts registered under section 12AA.

Other Provisions

Applicability of other provisions such as Tax Deducted at Source (TDS) on expenses is completely applicable to an educational institution or university. Therefore, an educational institution or university is required to deduct tax from payments, wherever required to claim the amount as application of income.

Conclusion

From the above detailed discussion, we can conclude that the exemption offered to Educational institutions or universities as an NGO are specified in provisions of Section 10(23C) and Section 11 are very similar. Both have similar requirements and conditions for claiming exemption by doing NGO Registration. Though, Section 10(23C) has fewer necessities when it comes to accretion of income i.e. there is no requirement for filing a separate Form and also there is no requirement to specify the purposes of accumulation.

Read our article:An overview of Temple Registration under NGO