Tax accounting is an arrangement that focuses on tax appearances on financial statements. It is governed by the Internal Income Codifications of any NGO which commands the specific rules that the NGO must follow at times of formulating their tax returns.

Donations made by a charitable institution to any other NGO listed under section 12AA, that forms apart of a corpus of recipient institution shall not be treated as application of income under section 11.

What does Corpus Fund signifies in terms of Inter-NGO Donations?

Corpus Fund is a type of fund which is kept for the necessary expenditures desired for the management and existence of the NGO. Therefore, the corpus fund is generally not permitted to get utilized for the accomplishment of the purposes.

However, the interest/ dividend accrued for such funds can be employed for the accumulation of overall revenue. NGOs can use other donations as corpus donation, only if there is no prior specific instruction received from the donors to employ it as corpus donation.

Additionally, it has also been held in numerous cases that donation made by one Charitable Organisation to another shall be measured as ‘application of income’ if the object of the organization have objects parallel to the purpose of donor establishment.

Non-conformity of exemption on Corpus by Inter-NGO donations

- It has been planned to insert a new Clarification under section 11 of the act to provide any amount, out of income mentioned in clause (a) or clause (b) of sub-section (1) of section 11. The contributions with detailed direction that forms a part of the corpus of the institution shall not be preserved as application of income. It has suggested for inserting a requirement in clause (23C) of section 10 to make related restrictions on the entities exempt under sub-clauses (iv), (v), (vi), or (via).

- Those are to be regulated as per said clause for the amount credited or paid out of the income. Such amendments have taken place from 1st April 2018 and accordingly applied to all the concerns by the assessment year 2018- 19 and the following years.

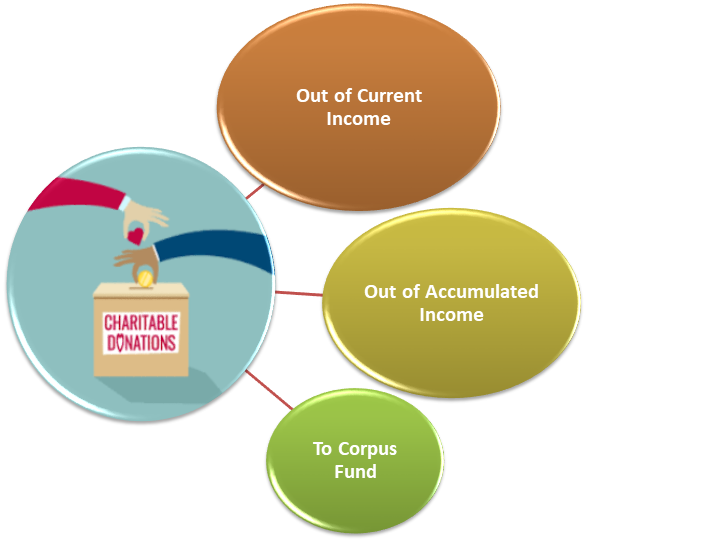

What are the Donations to other Charitable Institutions?

The three types of Donations to other Charitable Institutions are as follows:-

Donations Derived out of Current Income

If any inter-NGO’s or institution’s donations made out of the current year’s income, then it is regarded as an application of funds under the terms of the act. There is no explicit bar on payment or credit to such other institutions out of the previous year’s income subjected to the terms of section 11(1).

Donations Derived out of Accumulated Income

- According to the new explanation embedded long back by the Finance Act, 2002, section 11(2) has prohibited organizations from applying its accumulated or set-apart income by way of payment or loan to other institutions. If an NGO/institution donates accumulated funds U/s 11(2), then it would be deemed a violation of the section. Moreover, the amount donated shall get considered to be the income of such person of the preceding year.

- As per provision to sub-section (3A) under section 11, inter-charity donation derived out of accumulated funds will be permitted in case of the dissolution of a Charitable Organisation.

Donations Derived for Corpus Fund:-

- Any donation made by a charitable trust to any other trust or organization registered Under Section 12AA (form part of the corpus of recipient trust/institution) shall not be employed as application of income u/s 11 for the donor trust/institution. It has viewed as per the explanation 2 added to section 11(1) by finance act 2017.

What does Authorities say on the Utilisation of Income Receipt?

- Any donation made by a charitable Trust to another charity with parallel or similar objects gets reflected as an application of income for charitable or religious purposes.

- Central Board of Direct Taxes–Instruction No.1132 (1978) has clarified that if the donee of the organization does not utilize in the year of receiving, then the exemption to contributor will not be affected.

- Moreover, the Assessing Officer should be satisfied that the donation is a bonafide, which will be used by the donee for charitable purposes only for the Organisation. In short and crisp, any unreserved benefit to the donor is not accessible.

- Additionally, even the High Courts have held that inter-charity donations in the direction of the corpus are valid applications. But then again this contention may need re-consideration. After the Financial pronouncement dated- 01.04.2002, inter-charity donation out of accumulated funds is not promising by nature except in the case of closure of the donor administration.

- As a result of this, any organizations receiving funds towards the end of the year can still make inter-charity donations under the Explanations to section 11.

What is the Journey behind Inter-NGO Finances Donations 2002-03?

Donations from a Charitable Institutions to Another

In the beginning, it has held in numerous cases that donation made by one Charitable Organisation to another shall be measured as application of income for the organization on condition that the receiving organization also has object similar to the object of donor organization.

Donations from a Charitable Institution to another Later 1/4/2002

- After the engagement of The Finance Act 2002, it has introduced an Explanation to sub-section (2) of under section 11. It notably prohibits donations to other Charitable Organisations derived out of the accumulated funds of the institution. In compliance with the far-reaching practical implications, this amendment puts restrictions on donations to other NGOs only acquired out of accumulated funds.

- In simple words, the funds once get accumulated under section 11(2); they can only get applied for charitable purposes directly by the concerned organization. Subsequently, any such inter-organizational transfer would not arrive as sufficient to be potential.

Any Donations derived out of Current income is Qualified for Application

- On the other hand, the inter-organizational donation isn’t getting prohibited from current years of income received. But then again, the newly amended provision will indeed create obstacles for organizations that get used as conduct for passage rising funds to other such institutions.

- In agreement with the new explanation implanted by the Finance Act 2002 [section 11(2)], it has debarred organizations from applying its accumulated or set-apart income received. It could be by way of payment or credit to other such charitable institutions.

Central Board of Direct Taxes on Inter-NGO Donations

- In the light of the “circular no. 8, date 27.08.2002′ given by the Central Board of Direct Taxes, funds once accumulated are no longer accessible for credit or payment to any other Charitable Organisation. Nevertheless, the Central Board of Direct Taxes has also issued a clarification, which says that such transfer may still be conceivable derived out of the current year’s income under section 11.

- Inconsistent with the amendments of the Finance Act, 2002, donations to other charitable institutions are still possible but only derived out of the current year’s income. As soon as the funds get accumulated, at that time, it will not be permissible to make Inter-NGO donation and treat them in place of application.

Donations from a Charitable Institution to another Later Amendment in Finance Act-2003

- After the amendment in the Finance Act year of 2003, it has inserted another proviso to ‘sub-section (3A) of section 11’. It provides that Inter- NGO donation out of accumulated funds will be allowable only in case of the ‘dissolution’ of any Charitable Organisation. The motive behind the amendment was to reduce the hardship of Charitable Organisations on the edges of its dissolution.

Taxability on Donations from a Charitable Institution to another over Considered Application

- From the time when accumulated income is not available for Inter- NGO donations, the funds possibly will neither be applied nor could be donated to other charities. For the case where if a Charitable Organisation obtains funds – which is obligatory to be circulated to other charitable Institutions – and is unable to make Inter-NGO donations in the year of receipt, then it has to accrue the same. On one occasion where the income gets accumulated under section 11(2), at that juncture, it is not allowable to make Inter-NGO donations.

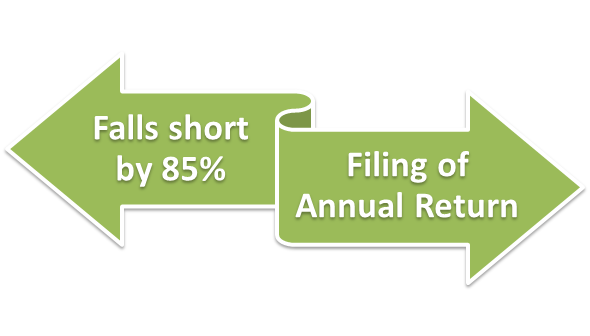

- Depending upon the above pointed out situations, a Charitable Organisation may exercise the option presented under the explanation to section 11. For that reason, it refers to two circumstances:-

- Where the income applied falls short by 85% but still can be considered to have been involved in the prior year.

- Secondly, the assessee may use its option by applying in writing before the expiry of the time permitted ‘under section 139(1)’ for filing of Annual Return.

If the Inter-NGO donations get its valid application of income, there is no cause under Explanation 2 to section 11(1) could not be applied as well as the income gets genuinely-placed/expended/distributed in the successive year. Nonetheless, all the reasons have to be genuine. With this, the organization must make sure that they carry valid reasons for not being able to apply the income as Inter-NGO donations.

Read our article:Application & Accumulation of Income by Trust: Case Laws

What are the Major Case laws Enshrined upon the Inter-NGO/Charity Donations?

Case: – D.C.I.T. Vs. M/s Divya Yog Mandir Trust (I.T.A.T. Delhi) Exemption U/s 11 admissible on Inter-NGO donation for application towards charitable objects

Case Synopsis

- In the view of the Central Board of Direct Taxes- Instruction No. 1132, date 5-1-1978, the Inter-NGO donation by one charitable trust to another for operation towards charitable objects stays proper application of income is in the hands of donee trust. In addition to it, it will not affect the exemption under section 11 as requested by donor trust in any manner. The assessee was a trust registered under section 12A appealed for the exemption under section 11.

- After that, the A.O. rejected the exception on the Inter-NGO donations made to ‘Patanjali Yogpeeth’ by another charitable trust to set up of ‘yoga gram’ and other yoga connected activities. It further did not amount to the application of income charitable purposes of the institutions.

Held

- In light of the circular, as mentioned above, it held the order approved by the ‘Coordinate Bench of Tribunal for AY 2009-10’ in assessee’s case. It says that the inter-trust donation by one charitable trust to another for employment by the donee trust in the direction of charitable objects was a correct application of income for charitable purposes.

- Besides, it would also not affect the exemption requested by the assessee under section 11. It will not alter in any manner, nor could any inter-trust donation get termed as non-conformity from its objects. It is because nowhere in the case of Department that donee trust had not applied such calculations for charitable purpose differing funds.

Case: – St. Joseph’s Convent Chandannagar Educational Society [2016 Kolkata – Trib]

Case Synopsis

- According to section 13(3) (b), it covers a person whose total contribution up to the end of Fiscal year more than 50,000/-. In this very context, both trusts have exchanged more than Rs. 50,000/- as well as stood covered by 13(3)(b).

- In furtherance to it, as per S.13(1)(c), if any part of income or property of the trust is handed down or applied for the profit of person covered by 13(3), any claim for exemption u/s 11 is not accessible. In consonance with the Finance Act 2014, as per its 12AA (4), the registration may get canceled. Moreover, as per Section 115TD presented by Finance Act 2016, tax on the Minimum Marginal Rate is payable on the total market value of assets less charges.

Held

- The Inter-NGO charity out of income accumulated u/s 11(2) only gets prohibits under the Explanation below Section 11(2), not out of current income

- Any payment or credit of money to trust listed u/s 12AA [or Institution u/s 10(23C) (iv), (v), (vi), (via)] is allowable in case of dissolution of the trust. It is only allowable in the year in which trust or institution gets dissolved, as viewed as per 2nd proviso to S.11 (3A).

- Any Inter-NGO donation given by one trust to another trust derived out of the current year’s income is legalized under section 11 of the act by way of an application of income. Furthermore, the same cannot get curtailed by another provision of the Act (i.e., section 13(1) (c) (ii) read with section 13(3) of the act) as it would reverse the objectives of such provision.

- The case, as mentioned above, passed the subsequent decree upon a simple donation by one public charitable trust to another public charitable trust, in which no individual could grasp any substantial interest.

Additional relevant case laws are as follows:-

- C.I.T. v. Trustees of the Jadi

- I.R.C. v. Helen Salter Charitable Trust Ltd

- C.I.T. v. Sarla Devi Sarabhai Trust

- C.B.D.T. Instruction No. 132, dated 05.01.78.

- C.I.T. v. Matriseva Trust

- C.I.T. v. M. CT. Muthiah Chettiar Family Trust & Others

- C.I.T. v. Aurobindo Memorial Fund Society

Conclusion

The Indian government is becoming more conscious of assembling the correct tax from roots so that our economy gets more durable. It aims to fulfill this goal as per the new amendments proposed until this date. Having said this, if any capital gets utilized for donating to another charitable trust following the objects of the trust deed, then yes, it should be understood as the application towards income.

These are just an evaluation, and we always inspire our readers to examine the issue in-depth based on the mentioned case laws and amended rules/decided judicial decisions accordingly. With this, the group of Corpbiz has experienced professionals to help you with the process of Inter-Charity Donations and tax exemptions parameters. Our expert will ensure the successful and favorable completion of your work.

Read our article:NGO Registration – Step by Step Procedure