The term ‘Agent’ has been defined under section 2(5) of CGST Act, 2017 as a person including a factor, commission agent, broker, auctioneer or any other mercantile agent who carries on business of supply and receipt of services or goods on behalf of another. A pure agent is the registered taxable person who liaises between other suppliers on behalf of his client.

The concept of this while providing services to a client, he also undertakes to receive the ancillary services from service providers and incurred expenditure on behalf of the client. The actual expenditure incurred by the pure agent is later claimed as reimbursement. In other words, over and above a value of services rendered to his client, other expenditure incurred by the pure agent (behalf of the client) can be reimbursed.

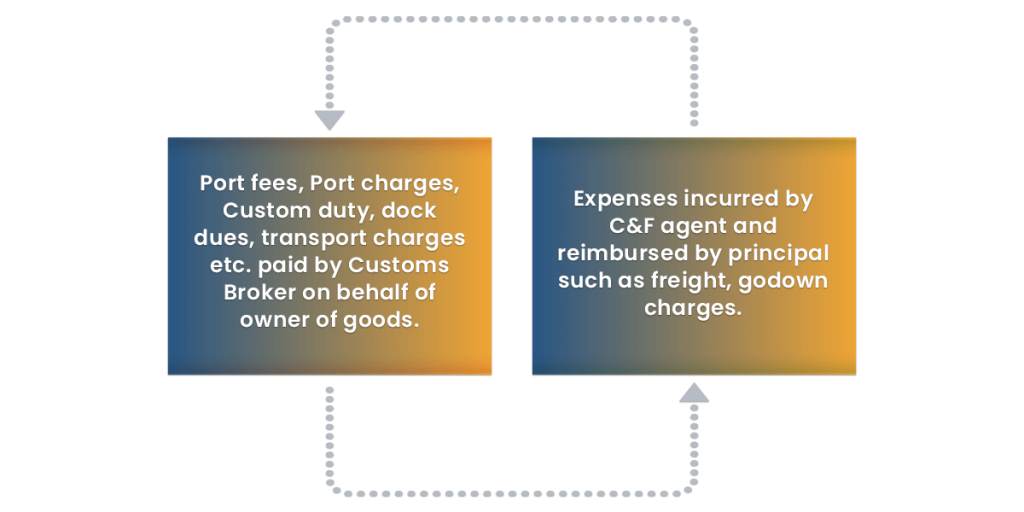

Illustration of Pure Agent

For example- A is an importer and B is a Customs Broker. A approaches B for the customs clearance work in respect of an import consignment. The clearance of an import consignment and delivery of the consignment to A would require taking service of a transporter. Hence A authorises B, to incur expenditure on his behalf for procuring services of the transporter and agrees to reimburse B for transportation cost at actual.

In given illustration, B is providing Customs Brokers service to A, which would be on the principal to principal basis. An ancillary service of transportation is procured by B on behalf of A as the pure agent and expenses incurred by B on transportation shall not form part of value of Customs Broker service provided by the B to A. This, in sum and substance, is a relevance of the pure agent in GST. Following are the examples of pure agents for your better understanding:-

The Relevance of Pure Agent in GST

The concept is borrowed from erstwhile Service Tax Determination of Value Rules, 2006 and carried forward under the GST. Under GST Valuation Rules 2017, a pure agent is defined as a taxable person who:-

- Enters into the contractual agreement with a recipient of supply to act as his pure agent to incur expenditure or costs in a course of supply of goods and services or both;

- Neither, intend to hold nor holds any title to goods or services or both, so procured or provided as the pure agent of the recipient of supply;

- Receives only an actual amount incurred to procure goods or services in addition to an amount received for supply he provides on his account.

How to Calculate a Pure Agent value in GST?

The Pure Agent in GST typically incurs the expenditure on behalf of his client, and later the actual will be claimed as reimbursement. Thus, it needs to be clear whether the value mentioned in a pure agent invoice under GST, must be included or excluded in determining the taxable value of supplies made by the pure agent to his client.

In determining a value of taxable supply, any expenditure incurred by a supplier as the pure agent of the recipient must be excluded from the value of supply. Thus, a pure agent concept in GST becomes more relevant from a point of determining the taxable value.

Conditions applicable to Pure Agent escaping the Taxability’s

Expenditure incurred as the pure agent becomes relevant when it comes to determining the value of a supply for levy of GST. The valuation rules provide that an expenditure incurred as the pure agent, will be excluded from a value of supply, and thus also from aggregate turnover. However, exclusion of expenditure incurred as the pure agent is possible only and only if all the conditions required to be considered as the pure agent and further conditions mentioned in the rules must be satisfied by the supplier in every case.

A supplier must have to satisfy following conditions for exclusion from value as under:-

- Any supplier acts as a pure agent of recipient of supply when he makes payment to third party on authorization by recipient;

- The payment made by a pure agent on behalf of recipient of supply has been separately indicated in an invoice issued by the pure agent to recipient of service

- The supplies procured by a pure agent from the third party as the pure agent of recipient of supply are in addition to services he supplies on his own account.

In case conditions are not satisfied, then expenditure incurred must be included in the value of supply under GST.

Conclusion

A concept of a pure agent is an important one for businesses as it has direct implications on a value of taxable service. It has a direct bearing on an amount of the GST charged on a particular supply. It also has a bearing on an aggregate turnover of the supplier and therefore on calculating the threshold limit for GST registration.

Whenever an intention is to act as the pure agent, care should be taken to ensure that the conditions specified for pure agents and conditions given in the valuation rules are met so that only a real value of the service provided is subjected to the goods and service tax.

Read our article:GSTN Rolled out Solutions to Prominent GST Errors