CCPS is also known as Compulsory Convertible Preference Shares which is a well-recognized investment instrument preferred by Private Equity investor. CCPS is referring to as an anti-dilution or hybrid instrument. NBFC can issue CCPS without availing permission from Reserve Bank if the conversion remains well below the twenty-six percent. Henceforth, it is safe to say that RBI’s permission is not required in the event when there is no noticeable increment in shareholding.

However, during the conversion of preference shares to equity, NBFC must obtain permission for Reserve Bank. NBFC can issue Compulsory Convertible Preference for a max timeline of twenty years. There will be no tax obligation on Compulsory Convertible Preference Shares, whether it is issued at face value or par.

What do you mean by Compulsorily Convertible Preference Shares?

Compulsorily Convertible Preference Shares, aka CCPS instruments that mandatorily changed into equity shares of the issuing organization on the predetermined condition at the time of releasing of the instruments.

Compulsory Convertible Preference Shares typically posses lower interest rate as compare to NCDs. CCPS are also deemed as capital instruments & investment done Compulsorily Convertible Preference Shares under the FDI route,

As per RBI, the CCPS ought to be treated at par with equity shares. Indian organization can agree to financial commitments depends on the exposure to a joint venture via CCPS. The current provision related to FDI (foreign direct investment) contributing to the equity capital of the venture to acquire a joint venture.

What is the Concept of Anti Dilution in CCPS Issued by NBFC?

The company’s promoters avail several benefits from CCPS by maintaining equity shares intake during the release of equity share to new investors. The promoter can easily convert the Compulsory Convertible Preference Shares availed in the event of lower valuation of shares when new investor introduces the funds at a higher valuation. Subsequently, the promoter can escalate its stake in the absence of the fund described above.

How Private Equity Investors get benefitted from Compulsorily Convertible Preference Shares?

CCPS offers several benefits for private equity investors. During the conversion time, the investor can link the performance of the company. This essentially indicates that the share shall get converted only in the situation when the NBFC accomplish the target growth. In case the target is not laid out, the company has every right to crank up its stake.

According to norms of the capital market regulator, any acquisition of fifteen percent or more (in case listed organization) opens up the possibility of offers. Likewise, a PE firm can drive direct equity of @14.9% and remain in the form of securities, which might transform into equity within eighteen months. In this ways, the companies have a chance to exist the one year lock-in period for private equity investment.

How Start-ups can avail benefits from CCPS?

The CCPS, aka Compulsory Convertible Preference Shares, also render aid to the owner of startup firms in curbing their stake at the stage of funding of new investors in the absence of infusion new funds. As CCPS are also referring to as anti-dilution securities, the company’s owners can handle their equity by introducing additional funds. This also helps the owner to handle their equity share to manage the organization by holding a good amount of stake in the company.

Discounted Cash Flow under CCPS

The Compulsory Convertible Preference Shares helps in averting the valuation gap that exists between investor and founder. According to the theoretical viewpoint, several methods are used to bring at par the equity share value. Furthermore, the most preferred method for calculation of the valuation gap is the relative valuation. Another method that is used for the purpose is known as Discounted Cash Flow (DCF). The said method seeks multiple assumptions, including forecasting data of five years for valuation. Henceforth, an easy method to avert a valuation discussion is if there is any distinction.

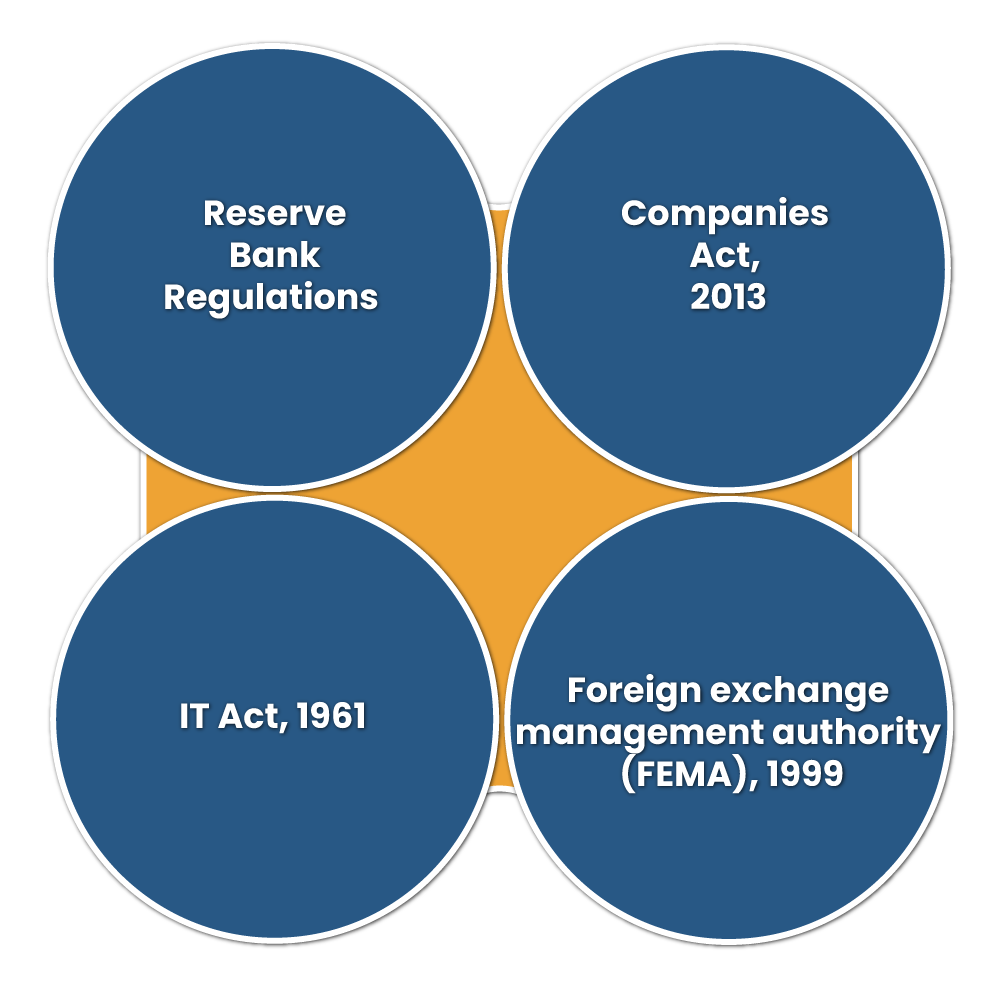

Regulatory Framework Related to CCPS

The issuance of CCPS securities is not a straightforward business decision for NBFCs. It plays a pivotal role in curbing the promoter’s equity stake. A slightest of disparity can impact the holding structure of the founders. Moreover, the Compulsory Convertible Preference share issued by NBFC entails compliances of 4 major laws, which are as follows:-

Companies Act, 2013

The following bylaws regulate the issuance of Compulsory Convertible Preference Shares:

- Section 42, Companies Act, 2013

- Section 62, Companies Act, 2013

- Section 55, Companies Act, 2013

- Companies (Prospectus and Allotment of Securities) Rules, 2014

- (Share Capital and Debentures) Rules, 2014.

FEMA Regulatory Framework

Compulsory Convertible Preference Shares are also being recognized as equity instruments; subsequently, even overseas investors can subscribe under the FDI policy under the automatic route in the view of pricing guidelines as well as the sartorial cap. As per the above policy, the conversion stipulates shall be determined upfront during the issuance of said instruments. The price during conversion, under any circumstances, should not be lower than the fair value estimated during the issuance of such instruments.

Keep in the mind that Indian companies are not eligible to issue Non Convertible Preference shares (NCPS) under the foreign direct investment policy. The External Commercial Borrowing Regulations regulate it. Moreover, Indian companies have an option to issue CCPS subjecting to some limitations minimum lock-in period and also assured to returns to overseas investors. Henceforth, one has to remain cautious while opting for the convertibility aspect of the Preference Shares. Post compliances issues of Compulsory Convertible Preference Shares are as follow:

- Submitting advance reporting form – First Year Commission

- FCGPR – Foreign Currency-Gross Provisional Return

The compliance measures remain more or less the same during the issuance of equity shares. The filing of the FCGPR isn’t mandatory during the conversion, i.e. CCPS into equity shares. However, it is advisable to intimate the Reserve bank about the information of conversion of CCPS into equity shares, so that Reserve Bank would update its database related to the foreign equity policy.

Taxation Regulatory Framework

The CCPS valuation is done pursuant to section 56 (2)(viib) of the Income Tax Act, 1961.

As per the said section, the unlisted entity receives the consideration regarding the issuance of shares from any individual being a resident that surpasses the face value of such shares, the cumulative compensation availed for such shares which surpasses the fair market value of shares will be converted to income tax under the head income generated from other sources. But, pricing, as mentioned above limitation, is not applied to the shares issued to the non-resident individual.

Stamp duty Aspect of CCPS

The payment related to the stamp duty is governed by the stamp duty act of the respective states. It should be noted that no stamp duty applies to the Equity Share Certificate.

Regulations Imposed by Reserve Bank of India

The offered document regarding the private placement ought to be issued within six months from the date of issuance of board resolution regarding the same. The offer document must enclose the name of the office along with their designation that reserves the right to issue the offer document. The offer document and board resolution must enclose all the detail about the purpose behind the procurement of the said resources.

- The offer document must be printed as “For Private Circulation Only.”

- The general information like the registered office address, date of opening or closure of the issue etc. must get enclose in the offer document.

- The NBFC make sure to issue debenture for the inclusion of the funds in its balance sheet and not facilitate request regarding the resources of group entities or associates or parent companies.

- The private placement by all the Non-Banking financial companies will be limited to forty-nine investors, picked by the NBFC.

- The cost of subscription for a single investor shall be twenty lakh rupees and in multiple of ten lakh rupees afterwards.

- There should be a minimum period gap of at six months between the subsequent private placements.

- An NBFC cannot extend credit while taking the security of its debentures into account.

- All other guidelines in pursuant to private investments remain unchangeable.

- The provision of the said direction shall supersede in case of contradiction.

Conclusion

The NBFCs should make sure that at any instance, the debenture issued, including NCDs, are secured. Henceforth, during the issuance period, the security cover is inadequate or not formed the issue proceeds will be routed to secure escrow account until the formation of security. The several statuary compliances accountable for the creation of CCPS are mentioned in this blog. However, in the current scenarios, Compulsory Convertible Preference Shares are playing a crucial role as far as the strategic decision-making of the company and investor is concerned.

Read our article:How to get easily a Name Change Affidavit in India?