Nowadays a lot of corporations have gotten so big that it’s hard to focus on what they’re currently doing. The hazards related to doing business have multiplied along with corporate expansion. The government has improved the internal audit system for numerous companies under the 2013 Companies Act in order to lower the risks connected with the firm. Internal audits are crucial to the day-to-day operations of a business.

In order to give independent assurance on the efficiency of internal controls and risk management systems and enable the organization to achieve its objectives, internal audits evaluate business processes and internal controls. On August 30, 2013, the Companies Act, 2013, which calls for a significant revision of the corporate governance standards for all companies in the nation, was put into effect.

The Act modifies and defines the legislation governing corporations. For any business or a class of companies (both listed and unlisted), as may be stated therein, the conditions imposed under the Companies Act, 2013, and the rules published there under, would be applicable.

What is Internal Audit?

Internal audit is an independent management function that continuously and critically evaluates how an entity functions with the goal of making suggestions for improvements. It also adds value to and strengthens the entity’s overall governance system, including its internal control system and strategic risk management.

What is the Objective for Conducting an Internal Audit?

The internal audit begins with an examination to see if the company is in compliance with all applicable laws, and then the internal auditor prepares a report outlining compliances and any substantial deviations. The internal auditor must make sure that he is mindful of the Companies Act of 2013’s obligations for internal audit. In order to perform an internal audit or to generate a report thereto, the Companies Act of 2013 has no specific format or method requirements. As a result, businesses have the freedom to perform internal audits in accordance with their needs and size.

However, the report that has been generated must list the compliances, any deviations that were discovered, and the steps taken to correct the problems. The procedure should be handled honestly and transparently when it comes to the risk, internal checks, and internal control system and it should be given the appropriate weight as it examines the company’s state of affairs.

Also Read: Section 207 of Companies Act, 2013: Conduct of Inspection and Inquiry

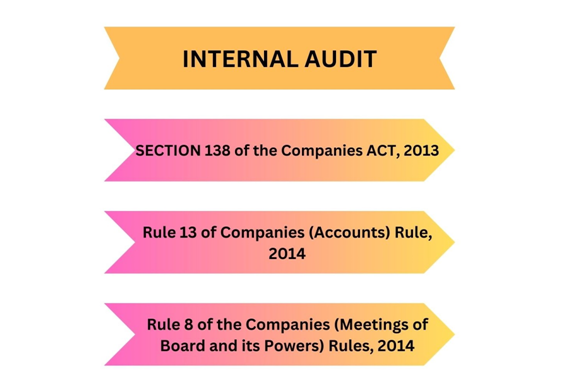

Section 138 of Companies Act, 2013

Sub-section (1) of Section 138, Companies Act mandates that businesses that must conduct internal audits appoint an internal auditor:

- Either a Chartered Accountant (whether practicing or not), a Cost Accountant (whether practicing or not), or both are required for internal auditor qualification.

- Any other professional that the Board deems appropriate.

The mode and intervals at which the internal audit shall be undertaken and reported to the Board may be prescribed by rules made by the Central Government.

Rule – 13 of the Companies (Account) Rules 2014

The following class or classes of corporations must hire an internal auditor or company of internal auditors, under Rule 13 of the Companies (Accounts) Rules, 2014:

- every listed company;

- every unlisted public company having-

- Paid-up capital of at least 50 crore rupees during the last fiscal year; or

- revenue of at least 200 crore rupees during the previous fiscal year; or

- outstanding loans or borrowings of at least 100 crore rupees from banks or public financial institutions at any point during the previous fiscal year;

- outstanding deposits totaling at least 25 crore rupees at any point in the previous financial year; and

- every private company having-

- Any private firm that had a turnover of at least 200 crore rupees the previous fiscal year, or

- Outstanding loans or borrowings from banking or public financial institutions that totaled at least 100 crore rupees at any one moment.

Thresholds for the Internal Audits Under Section 138 of Companies Act, 2013

- The application of internal audit shall be followed by all registered types of listed firms.

- All unlisted public company with an annual revenue of at least 200 crore rupees shall adhere to the internal audit’s applicable requirements.

- Every unlisted public firm that has issued shares for 50 crore rupees or higher shall adhere to the internal audit’s application.

- An internal audit shall be conducted by any unlisted public firm with an outstanding deposit worth 25 crore rupees or more at any one time.

- Every unlisted public firm that has ever obtained one hundred crore rupees or more from numerous banks or public financial institutions shall adhere to the internal audit’s application.

- Every private firm that has a yearly revenue of at least 200 crore rupees shall adhere to the internal audit’s applicable requirements.

- Every private firm that has ever received one hundred crore rupees or more from several banks or public financial institutions shall adhere to the internal auditing requirements.

Responsibilities of an Internal Auditor

- You must maintain your independence at all times and refrain from participating in the exercise of executive function.

- Examine the risks and notify management about them.

- Examine the entity’s activities, maintain a sufficient internal control system, and offer protection against asset theft.

- Assess the organization’s policies and make the appropriate adjustments if necessary.

- Continue to keep up to date on all significant happenings and events that can have an impact on the company.

- Shall not decide on operational concerns that may be subject to internal audit later.

Also Read: Section 129 of Companies Act, 2013: Financial Statement

Penalty for Non-Compliance

No particular criminal provisions are established under Section 138 of Companies Act, 2013. As a result, if Section 138 of Companies Act, 2013 is broken, the criminal provisions listed in Section 450 would apply.

As a result, the firm and any defaulting officers of the company would each be subject to a punishment of up to Rs. 10,000. If the breach persists, a daily punishment of Rs 1,000 will also be levied. The Companies Act of 2013’s Section 441 allows for the compounding of violations of Section 138 of Companies Act, 2013.

Conclusion

In conclusion internal auditing is the process of analyzing and verifying internal issues, such as accounting, finance departments, and other business procedures. Internal audits are used to assess the efficiency and effectiveness of a company’s numerous operations and services. A timely adherence to the law and regulations may be ensured by an internal audit for an organization.

The audit offers a certain level of security and aids in managing risk those results from fraud, power abuse, or any other circumstances. An internal auditor gives the management their unbiased evaluation of the procedures and financial records. By hiring an internal auditor, management may enhance their financial and operational performance.

Frequently Asked Questions

The purpose of internal auditing is to offer value and enhance an organization’s operations. It is an impartial, unbiased assurance and consulting activity.

The purpose of the internal audit is to discover weaknesses or confirm strengths. An organization could conduct an internal financial audit, for instance, to ensure that its internal controls over accounts due are in line with company policy.

An organization’s internal controls, comprising its accounting and corporate governance processes, are accessed via internal audits. These audits assist to maintain timely and precise financial reporting and data collecting while ensuring compliance with laws and regulations.

Internal audit is responsible for independently confirming the efficiency of a company’s risk management, governance, and internal control systems.

Companies hire internal auditors who work on the behalf their management teams.

Although the legislation does not specify a deadline for internal audits, it is generally seen as best practice to carry them out every three months.

An internal auditor is required for all businesses with stock market listings in India.

Under Section 138 of the Companies Act of 2013, internal audit is stated.

Every private business with a yearly revenue of at least 200 crore rupees should adhere to the internal audit requirements.

Under Section 138 of Companies Act, 2013 no specific criminal provisions are specified. Each of the company’s defaulting officials might face a fine of up to Rs. 10,000. If the violation continues, a daily fine of Rs 1,000 will also be applied. The criminal penalties mentioned in Section 450 would be applicable if Section 138 of Companies Act, 2013 were breached.

Every unlisted public firm with an annual revenue of 200 crore rupees or more shall adhere to the internal audit’s applicable requirements.

Read Our Article: Section 118 Of Companies Act, 2013: Minutes Of Proceedings Of General Meeting