The sole motive of every business is to reap profit against every penny invested. The company is established with a goal of returns, which is the ultimate goal of every entrepreneur. A partnership firm is established with the primary object of profit. In this write-up, we will discuss the Remuneration to Partners and financial returns.

The role of a partner in a company is not confined to investment only. Few serve the business for an extended time, and others lend their goodwill for the business. The different investment seeks different rewards. And the finest efforts are supported by maximum returns. But, the partner is required to balance the payment subjectively for all. The term “remuneration to partners” exactly implicates this concept in a registered organization.

What are the Dimensions for Finalization of Remuneration Clause?

In general, such terms are inculcated in the remuneration clause during the registration of the partnership firm. However, before finalization of terms, you were required to comprehend all dimensions of financial returns to partners. It would let you make precise decisions apart from tax planning.

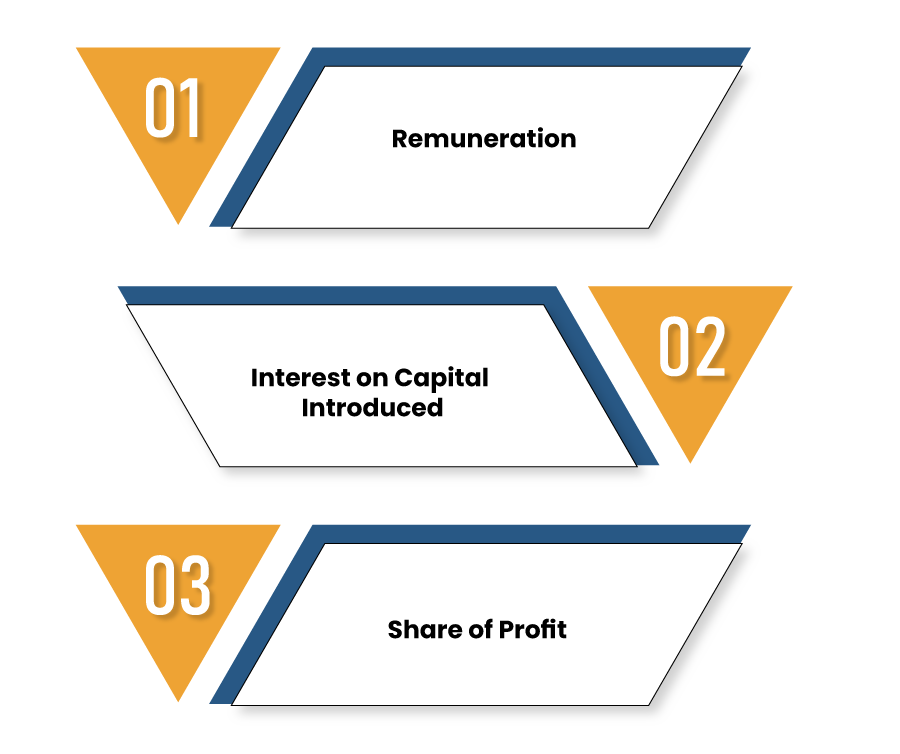

In a Partnership Firm, financial returns to partners are bifurcated in the given three heads:-

What are the Terms of Remuneration for Partners?

The term remuneration to partners implies any bonus, salary, commission, or remuneration paid to the partner. The partners were proactively contributing to the operation of the firm stand eligible to receive remuneration. Just like an employee, these individuals are rewarded for their contribution every month.

Determine if you Stand Eligible for Remuneration

The eligibility for remuneration is primarily subject to the remuneration clause in Partnership Deed. Whether you are actively involved or not, active or sleeping partners, you will be awarded in the form of remuneration provided the partnership deed has the same clause.

Eventually, it is a joint agreement of the partner to inculcate in a partnership deed. The nature of rewards implies providing remuneration to partners, and so does the IT law. It further reflects the max limit for remuneration in the same firm.

Amount Deductible under IT Act

The remuneration is permitted as a deduction from the firm’s profit when paid to an active partner. Here, deduction implies to deduction of expense from the firm’s profit. Moreover, the partnership deed must have the provision for paying remuneration to working partners.

Income Tax Act provides the max allowable amount, as mentioned below in the table. Any amount crossing this limit is not an allowable for deduction.

| Book Profit (Rs) | Maximum Deductible Amount |

| Loss | INR 150,000 |

| Up to 3 Lakh |

90% of Book Profit or INR 150,000; whichever is more |

| More than 3 Lakh | 60% of Book Profit |

It’s worth noting that limit is not imposed on the individual partner, but all on partners. It implies that the max amount estimated above is the sum payable to all active partners.

Taxability in the Hands of Partners

Remuneration which is permitted in the hands of partnership firm will be non-exempted in the hands of receiving partner as “Income from Business or Profession”. If such remuneration is not permitted as expense in the hands of the aforesaid firm then it will be exempted in the hands of partners.

Read our article:Description on Registration of Partnership Firm in India

What Interest is levied on Capital Introduced?

Interest is paid to active partners who have invested the capital, whether through cash or any other mode. Non-cash capital (tangible or intangible) is estimated in monetary terms at the event of its introduction. The interest has to be paid on the amount as per the capital clause of the Partnership Deed.

Provision Regarding Rate of Interest

The interest rate is provided under the relevant clause of the partnership deed. Though it is not mandated to mention interest rate in the agreement, it is advisable to do so. Citing the rate gets rid of the ambiguity and potential disputes that might arise in the future. The partners stand eligible to alter them anytime. It’s worth remembering that the partners who have invested the capital are eligible to receive the interest.

Amount Deductible under IT Act

According to IT Act, the maximum interest @12%/annum is permitted. Any amount paid surpassing the effective rate is not allowed as a deduction from the company’s income. For deducting applicable taxes as per IT Act, the partnership deed must have an authorization to pay interest on capital.

Make a note that an interest received by the firm’s partners is non-exempted as business incomes in their hand.

Profit Division under Share of Profit

The term share of profit reflects the percentage of profit divided among the partners.

What is the Profit-sharing Ratio?

The profit-sharing ratio is decided by the active partners of the firm. The absence of such a ratio in the partnership deed will allow the active partners to share equal profit. While agreeing to the ratio, make sure to consider its downside as well.

The partners are required to set a distributable amount via mutual decision. It is not compulsory to divide all the profit. Partners may agree to reserve some of the profit for reinvestment in the business[1].

Implication of taxes on Share of Profit

The share of profit worth Rs 1 lakhs furnished to each partner would be non-taxable in the hands of partner on account of provisions of section 10 (2A) of the Income Tax Act. The remuneration’s amount of Rs 10,000/month received by each partner would be non-exempted in the hands of respective partners.

Conclusion

While preparing the partnership deed, the partners must take all these clauses into account. While you may permit all kinds of financial-based reward via Partnership Deed, the taxability is estimated as per the IT Act. Even to pay the interest or remuneration, you must take their taxability into consideration.

The return paid more than the prescribed limit is not allowed & double taxed. In such a firm, it is taxable @ 30% with other applicable cesses, etc. Moreover, it is also subjected to taxes in the hands of partners at the given rate. Interest on capital and remuneration to partners is allowed to be deducted as business expenses up to a set limit.

Read our article:Partnership Firm Registration and Annual Compliances